![Artificial Superintelligence Alliance [FET] plunges 18% in a day: What's next?](https://moneyvests.com/wp-content/uploads/2026/06/Artificial-Superintelligence-Alliance-FET-plunges-18-in-a-day-Whats-696x392.webp "Artificial-Superintelligence-Alliance-FET-plunges-18-in-a-day-Whats.webp")

The Artificial Superintelligence Alliance [FET] token price rallied 50.94% from the 23rd of May to the 1st of June. This move spanned from $0.1914 to $0.2889, just below the $0.30 psychological round-number resistance.

AMBCrypto reported that this resistance level could be challenging to overcome. The recent rejection showed that sellers remained in control of this supply zone.

Though Binance traders had been bullish going into this supply zone, they have been headed. The question remains—was this a temporary reset, or should you anticipate a deeper bearish trend?

FET remains locked in a higher timeframe downtrend

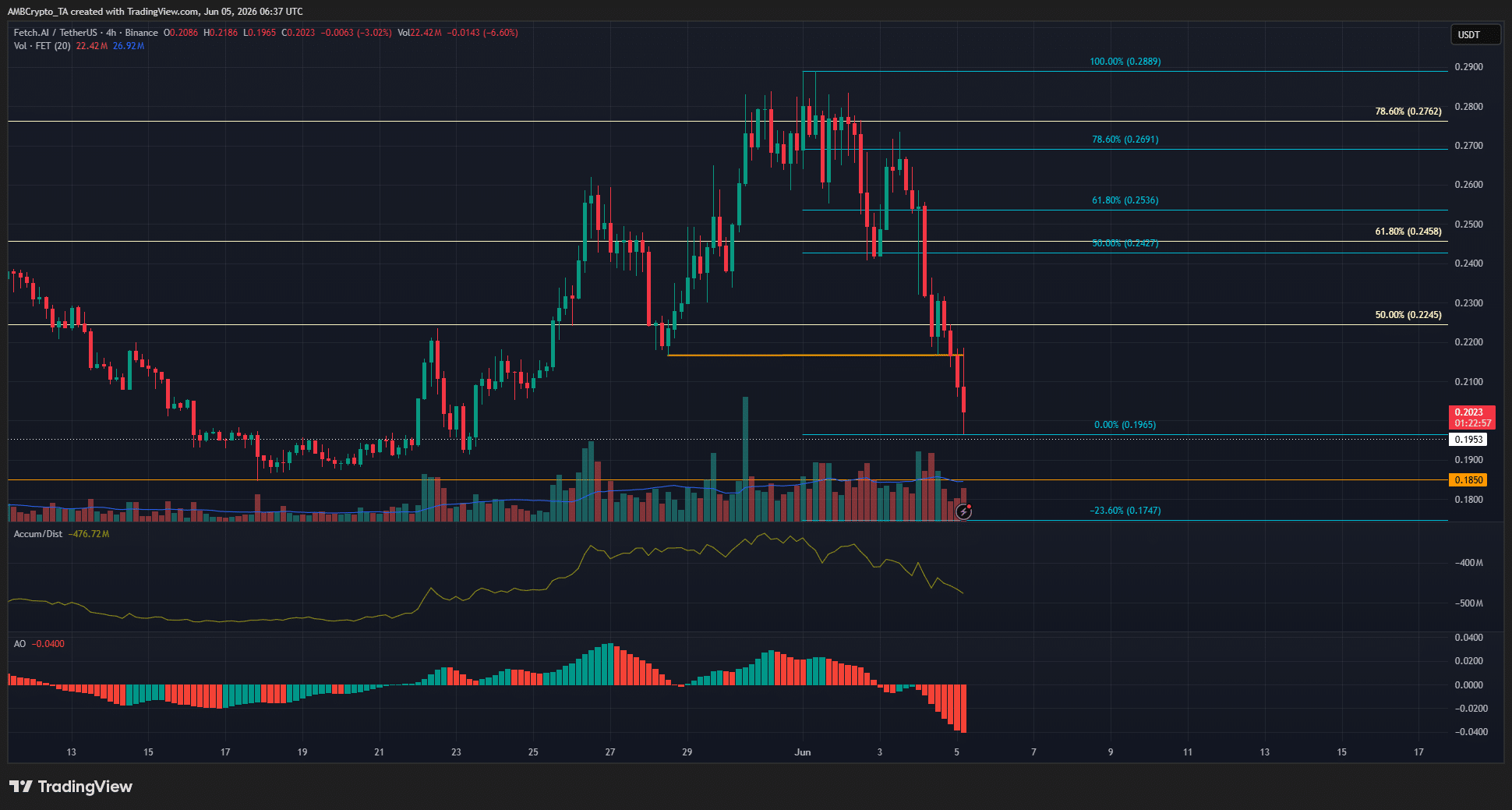

The higher timeframe price chart quite cleanly answered the question about FET’s ongoing trend. Despite the rally in recent months, the swing structure remained bearish.

The selloff in early 2026 saw Artificial Superintelligence Alliance token prices post a new swing low at $0.134. Like Bitcoin’s [BTC] relief rally to $82k, FET also witnessed a relief rally to the 78.6% retracement level.

The subsequent rejection has forced the price back to the $0.195-$0.20 support zone that has been respected since April.

FET is down by nearly 18% in 24 hours. Yet, though the momentum appeared firmly bearish in the short term, swing traders should watch out for a relief bounce.

Traders’ call to action: Sell the bounce

The internal structure has shifted bearishly on the 4-hour chart when the altcoin crashed below the higher low at $0.2166 (orange). The technical indicators also agreed with overwhelming bearish strength in the short term.

On this timeframe, the A/D was rapidly declining, and the Awesome Oscillator fell to depths not seen since the October 2025 crash. And the impulse leg was not yet over.

Eventually, the sell-off would be oversold and necessitate a relief rally. This bounce is likely to reach the $0.25-$0.26 area, though the exact levels are not clear yet.

Traders can wait for a bounce toward $0.25 before looking to sell FET. Trying to buy during the bounce could be risky since a Bitcoin drop below $60k can set off another immense wave of panic across the altcoin markets.

Final Summary

- FET bulls drove a rally nearly as high as $0.3 but were rebuffed from this technical and psychological resistance.

- A short-term bounce toward $0.25-$0.26 could offer a selling opportunity.