The Best Metatrader 5 Brokers: A Comprehensive Guide

As we all know, the MetaTrader 5 is one of the most popular trading platforms in the world and it is used by millions of traders. In this blog post, I will be sharing with you the best MetaTrader 5 brokers in 2022.

Top MetaTrader 5 brokers in 2022?

So, without further ado, here are my top MetaTrader 5 brokers in 2022:

XM Group

XM Group is a leading online broker that offers trading in more than 100 financial instruments. They offer their clients tight spreads from as low as 0 pips, fast execution speeds, and a leverage of up to 500:1.

They are also regulated by multiple financial authorities such as the FCA (UK), CySEC (Cyprus), ASIC (Australia), and BaFIN (Germany). Overall, XM Group is an excellent choice for both beginner and experienced traders.

IC Markets

IC Markets is another excellent choice for those looking to trade on the MetaTrader 5 platform. They are one of the largest forex brokers in the world with an average daily trading volume of more than $5 billion.

They offer their clients extremely low spreads from 0 pips, fast execution speeds, and a leverage of up to 500:1.

Global Prime is also regulated by multiple financial authorities such as ASIC (Australia), CySEC (Cyprus), FCA (UK), BaFIN (Germany), and MAS (Singapore).

Saxo Bank

Saxo Bank is a leading online broker that offers trading in more than 30,000 instruments across multiple asset classes including forex, stocks, CFDs, options, ETFs, futures, and bonds.

They offer their clients competitive spreads from as low as 0.6 pips on major currency pairs like EUR/USD and GBP/USD, fast execution speeds, and a leverage of up to 200:1.

Saxo Bank is also regulated by multiple financial authorities such as FSA (Denmark), FINMA (Switzerland), ASIC (Australia), BaFIN (Germany), and CySEC (Cyprus).

Overall, Saxo Bank is a great choice for those who want to trade in a wide range of markets.

CMC Markets-

CMC Markets is another leading online broker that offers trading in more than 10 000 instruments across multiple asset classes including forex, indices, shares, commodities, options, and cryptocurrencies.

They offer their clients tight spreads from as low as 0 pips on major currency pairs like EUR/USD GBP/USD USD/JPY; fast execution speeds; and negative balance protection.

CMC Markets is also regulated by multiple financial authorities such as ASIC(Australia ) FCA(United Kingdom ) IIROC(Canada ) FINMA(Switzerland )and SFC(Hong Kong ). Overall CMC Markets is ideal for those who want to trade on a wide range of markets with tight spreads and fast executions.

Pepperstone–

Pepperstoneis another great choice when it comes to finding good MetaTrader5 brokers in Traders Union. They are an award-winning online broker offering their services to retail and institutional investors alike.

Pepperstone offers its clients access to over 70 tradable assets via the MT5 platform including forex indices shares commodities cryptocurrencies options EFTs bonds; tight spreads from as low0 pips on major currency pairs like EUR/USDBGP/USD.

IG–

IG is one of the oldest online brokers in existence today having been founded back in 1974.

They offer their clients over 17 000 tradable instruments across multiple asset classes including forex indices shares commodities options cryptocurrency ETFs bonds; competitive spreads from as low as 1 point on major currency pairs like EUR/USD; GBP/USD; fast executions; leverage up to 200:1; negative balance protection; and much more.

IG is regulated by some of the most prestigious financial regulatory bodies such as FCA (United Kingdom); ASIC (Australia); BaFIN (Germany); Financial Conduct Authority Ireland); and MAS Singapore).

Overall IG is perfect for those who want an established broker with decades of experience offering them access to over17000 tradable assets.

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate contact us. If you see something that doesn’t look right, contact us!

Bezos Yacht is estimated to have a value of approximately $500 million

His Yacht has three masts that measure 229 feet each, making it impossible for it to pass under the bridge, which has the same height as a 13-story structure and a clearance of 131 feet.

The construction of his ship is anticipated to cost approximately $500 million.

Despite his low profile, the Amazon CEO does seem to enjoy yacht travel.

He and his wife Alexis Sanchez were spotted aboard the yachts of a number of high-profile friends, including David Geffen’s rising sun and Diane von Furstenberg’s schooner, Eos. In Cabo San Lucas, they were seen boarding yet another yacht.

Jeff Bezos Yacht

Jeff Bezos’ Y721 Yacht

Amazon CEO Jeff Bezos has just ordered two new superyachts, one of which will be the shadow version.

At 246 feet, the new vessel will seat 45 more guests and crew members.

It will also feature a helipad, conference room, and ample storage for Bezos’ water toys. It will be able to cruise the world in style. But it will also require at least $25 million a year to operate.

The new sailing yacht is being built by Oceanco, a Dutch shipbuilder. Like the Black Pearl sailing yacht, the Jeff Bezos yacht features a black hull with a white superstructure.

The yacht’s aft deck includes a swimming pool and can accommodate 18 guests.

The boat’s 40-person crew will also take care of catering duties.

The yacht’s design is based on the Black Pearl sailing yacht, which is considered the world’s largest environmentally friendly sailboat. Bezos will be able to cross the Atlantic without relying on fossil fuel.

Jeff Bezos’ yacht is too tall to pass under a historic bridge

Amazon founder Jeff Bezos is too rich to worry about his yacht’s height as it approaches a city bridge. The yacht’s masts are so tall that it could potentially pose a risk to helicopters.

Luckily, the former Amazon CEO commissioned a super yacht with its own helipad.

However, the construction of Y721 has prompted local authorities to dismantle part of the bridge, but that is not likely to happen.

As the biggest luxury vessel in the world, Jeff Bezos’ project Y721 is about to break ground in Alblasserdam, the Dutch city of Rotterdam. This project will require a bridge in the city of Rotterdam called the Koningshaven Bridge.

This historic structure can only accommodate ships 131 feet tall, so the construction of Bezos’ new ship will have to temporarily dismantle the bridge and relocate it elsewhere.

Jeff Bezos owns a yacht

Amazon founder and CEO Jeff Bezos is rumored to own a superyacht, and it’s set to debut in daylight next month. The yacht, named Y721, is 417 feet long, which is equivalent to four and a half blue whales swimming single file.

Upon completion, the yacht will be as high as the Great Pyramid of Giza.

Dutch yacht builder Oceanco is designing and building the vessel, which will have three decks, three enormous masts, and a helicopter pad.

The Amazon CEO has also been rumored to be building a yacht for himself. This has not been confirmed by Oceanco, the company that is building the yacht.

However, the yacht is expected to be the world’s largest sailing yacht, taking the title from the Sea Cloud, which was commissioned in 1931. The yacht will be accompanied by its own support yacht. The total cost is estimated at $485 million, according to Bloomberg.

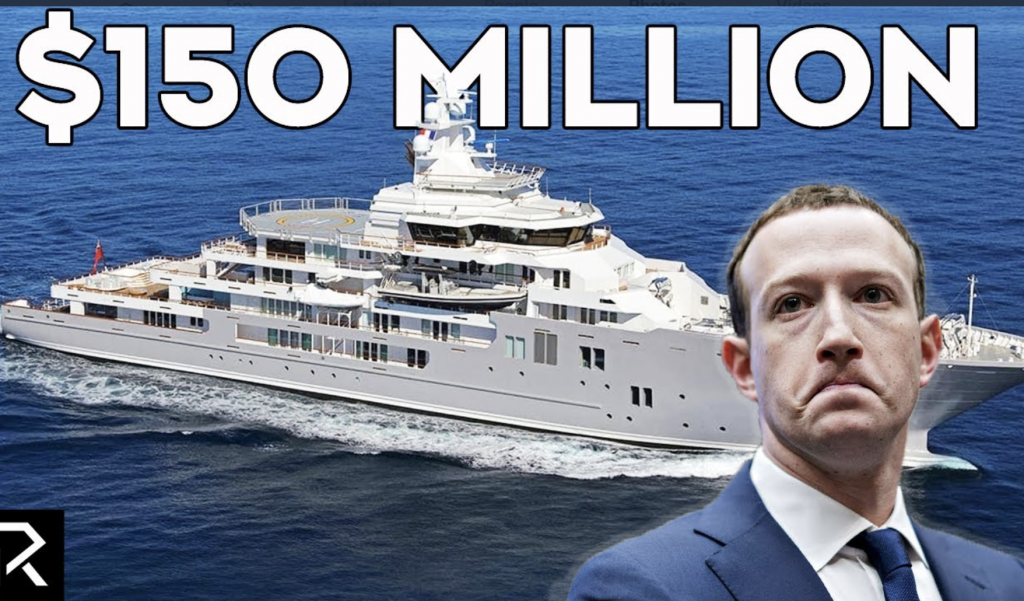

Mark Zuckerberg Yacht

Amazon CEO Jeff Bezos has ordered a $1.2 billion yacht. The two billionaires have not paid any federal taxes on the boat, and their wealth is almost double that of the average person.

They own a variety of asset classes, including real estate, art, and business ventures. They are also very involved in charity work, supporting Save The Children and Global Nomads, which focus on early childhood education.

They also support the National Academy of Science, the Aspen Challenge, and Mind In the Making.

Unlike Jeff Bezos, Mark Zuckerberg and Jeff Bezos do not own their own private jet. They use charter services for their yacht. A private jet will cost them at least $200,000 a day, so the yachts are expensive.

The billionaire CEO of Amazon spent about $25 million a year on charters. Jeff Bezos is the richest man in the world, second only to Bill Gates.

Bill Gates Yacht

The soaring carbon footprint of Jeff Bezos and Bill Gates’ birthday parties has become a topic of debate on social media.

While Gates is well known for giving millions to organizations that fight climate change, it is surprising that Bezos and Gates have yachts.

Despite the high carbon footprint of their yachts, both are committed to addressing climate change.

In fact, both Gates and Bezos are climate change activists. They have also been criticized for spending so much money on their yachts that it makes them look indifferent to our climate.

Bill Gates Yacht

Bill Gates’ 76-meter (230 ft) superyacht, called Lana, is for sale. The yacht was built by Benetti, a company founded in 2003. The Benetti Group operates out of 68 countries around the world.

Jeff Bezos’ yacht, Eclipse, is currently for rent at 3 million euro per week. Although Gates and Bezos are incredibly wealthy, they don’t seem to be in need of a vacation.

Did you enjoy reading this article? If so, check out more today!

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate to contact us. If you see something that doesn’t look right, contact us!

The Only Providers Offering a True Own-Occupation Definition of Disability to Physicians

Disability insurance is financial protection for your present and future earnings in case you become wounded, ill, or disabled and unable to work.

You can negatively affect your financial security without the right disability insurance.

Not only is the right disability insurance important but one should also have an understanding of the definitions of disability.

There are many definitions of disability; the strongest is the true own-occupation definition.

A majority of insurance companies claim to provide “true own-occupation” disability insurance, but big 6 disability insurance companies are the only ones that offer it.

A true own-occupation definition of disability is the simplest to qualify for. Physicians receive benefits despite being unable to perform some, all, or a portion of their present medical specialty.

Other definitions of disability include transitional own occupation, modified own occupation, and any occupation.

With transitional own-occupation, physicians receive benefits if they cannot work in another occupation and begin earning money in a new one.

The catch, however, is that your total income should be equal to the benefits plus your new income and not exceed your original income.

The modified own occupation definition states that a person who is disabled can be eligible for benefits if they cannot perform the duties of their own occupation.

Benefits become discontinued if the person chooses to work and earn a living in another occupation.

Any occupation provides policy benefits if you have a critical illness or are severely disabled and cannot work in any job. You will not collect benefits if you can work even in a low-paying job.

Insurance is expensive, therefore comparing insurance options and their terms and definitions is important before applying for one in order to manage your money properly.

In this article, we are going to look at the big 6 disability insurance companies and the benefits they offer for a true own-occupation insurance policy. The insurance companies include:

MassMutual

Ameritas

Guardian

Principal

The Standard

Ohio National

The Big 6 Disability Insurance Providers

The “Big 6” providers can offer you the exact services that you are looking for. These insurance providers are:

1. MassMutual Disability Insurance

MassMutual has been in operation since 1851 and is one of the top insurance companies in the country. They provide an income insurance plan called Radius Choice which is comprehensive and customizable.

The Radius Choice policy has various built-in benefits such as the presumptive total and the recurring disability benefits.

2. Ameritas Disability Insurance

Ameritas, established in 1887, is also one of the top insurers in the country. They provide retirement planning services and insurance products.

The Ameritas plan contains a true own-occupation definition of disability, a selection of optional riders and you can have access to several other built-in benefits.

3. Guardian Life Insurance Company of America

Since 1860, Guardian has been a dependable option for both life and insurance coverage. Guardian provides a true own-occupation definition of disability, just like all the other Big 6 companies.

The company offers:

Individual disability income insurance.

Group coverage

Short-term disability

Long-term disability

4. Principal Disability Insurance

Principal is a prominent insurance company that has been in operation for almost 140 years. The company provides a true own-occupation definition of disability called the regular occupation rider. With this plan, you will get guaranteed renewable policies up to age 65. The following are its built-in features:

A recurring disability benefit

A death benefit

A waiver of premium benefit

Physicians can customize a Principal insurance policy with optional riders.

5. The Standard Disability Insurance

The Standard, which was founded in 1906 as the Oregon Life Insurance company, is one of the largest insurance companies in the United States.

They have a history of being dependable and trustworthy providers of life insurance and disability insurance. The standard disability insurance contains a platinum advantage that provides a true own occupation disability definition and elimination durations ranging from 30 to 365 days.

6. Ohio National

This company has been in operation since 1909 and provides long-term and short-term disability insurance products. They contain their disability insurance services in a feature called ContinuON Income Solutions II, which is a great plan and alternative for physicians.

Ohio National plans come with useful built-in features such as the presumptive total disability benefit. It also provides essential optional riders like all the other “Big” providers.

The following are its optional riders:

The catastrophic disability rider

The COLA rider

The residual disability rider

In Conclusion

As a high-income earner, you’ll get the best insurance coverage with a disability insurance policy that provides a true own-occupation definition of disability.

The services offered by the different top-quality insurance companies discussed in this article vary a lot.

Therefore, it is important to compare the different terms and policies offered by each company to find the best insurance coverage that will meet your requirements.

I have a severe phobia of bridges and dirty balance sheets.

Hobbies: blogging, meditation, and loving Bull Market (my dog).

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate contact us. If you see something that doesn’t look right, contact us!

You might think you have a pretty good grasp on what financial planning is. In reality, though, on a day-to-day basis, financial planning is going to vary depending on where you are in your financial journey.

By this we mean that, for people just starting out with saving money or even building credit, financial planning might start with just getting a bank account and a credit card. But for those who are long past that stage in life, it gets a lot more complex.

For example, once real money starts coming in, a person might know they need to invest some of it, but they don’t know where to start.

Once people have a family, they might know they need life insurance, but they don’t know how much.

All of this falls under the category of financial planning. People are often comfortable handling some parts of it, and don’t have much of an idea how to handle other parts of it.

Regardless, there are certain things that should be included in all discussions of financial planning.

Get Started Investing

Hopefully this goes without saying, but we’ll say it anyway: You need to save and invest as large a portion of your income as possible. That’s not financial planning–that’s just a fact.

The financial planning part gets into the details of what that saving and investing should look like. It’s a lot more than putting money in the bank (though that should be a small piece of it).

For many people, the biggest question is going to have to do with what kind of investments they should make. Broadly speaking, this is asset allocation, and it–also broadly speaking–refers to stocks, bonds, and cash.

The way you allocate your investments across these asset types is usually based on how old you are, your ability to stomach the ups and downs of the stock market, and financial goals you have set for you and your family.

You already know what cash is, so let’s talk about the other two: stocks and bonds. These come in all flavors, and depending on the things mentioned in the previous paragraph, you’re going to invest in them somewhere on the spectrum from very conservative to very aggressive.

Conventional wisdom says that you’ll want to invest on the aggressive side when you’re younger and building up your wealth, and on the conservative side when you’re older.

And what do those words mean as they relate to investing? Aggressive stocks are the shares of companies that are growing like crazy and may not even be turning a profit. Think Amazon.com 20 or so years ago.

Conservative stocks are shares of companies that are large, profitable, and quite likely pay a dividend to their investors.

As for bonds, they’re best largely ignored when you’re young and building wealth.

Aggressive bonds are generally junk bonds, which pay big yields but have a higher risk of default, while conservative bonds might be the debt of one of the aforementioned companies that offer conservative stock investments, or, at the most conservative end, short-term US treasury bills and notes.

You don’t want to go out there and buy individual stocks and bonds, though. You want that handled by professionals.

Actually, that’s not entirely accurate–you generally don’t want people picking stocks and funds for you, including professionals. That’s called active management, and it will do worse than the overall stock market indexes the vast majority of the time.

Instead, you want passive management, also referred to as index investing. Index funds will track indexes (such as the S&P 500 and countless others) as best as possible, minus a small management fee. Keeping these fees low is one of the keys to successful investing.

Once you’ve chosen your investments, you’ll want to keep track of how they’re doing. You can use software like WealthTrace, which provides comprehensive financial and retirement planning software and also allows users to track their wealth.

Websites such as PersonalCapital allow users to track their investments and transactions while also providing investment management services for a fee.

It’s up to you how far down that path you want to go, but two things to consider: (1) Watching your investments too closely is a recipe for making yourself crazy, and (2) if you invest solely in index funds that match your goals and risk tolerance, you should not need to worry much about a rogue investment going wrong.

Funds will invest in some companies that do well and some companies that do poorly, but the chance of one of those companies’ stocks doing lasting damage to your investment portfolio is vanishingly slim.

Account Types

In addition to asset classes, you also have to consider what kind of investment accounts you should be funding. Here, we’re referring mostly to how the accounts are taxed and when they can be used.

A 401(k) and a traditional IRA are going to be tax-deferred, meaning you won’t pay taxes on their growth until you take money out of them in retirement.

It’s normally best to fund these right off the top, especially with a 401(k), where the employer might match a portion of your contributions. That’s free money, and it should not be ignored.

But it also makes sense to get a taxable account going as well. If you can squirrel away a bit of money–even a small bit, just to get in the habit–into a taxable account each paycheck, you absolutely should do so. As your earnings increase, you can increase your contributions to it.

Where financial planning comes into play here relates to what kind of accounts to fund and in what order. And that’s largely going to depend on what you hope to achieve by saving and investing.

What Do You Want Out Of This?

In most cases, you’ll want to fund that 401(k) up to the matching amount, regardless of what your goals are. But beyond that, where you sock away your funds is going to have to do with when you’ll need the money, and what you’ll need it for.

Most people want to invest for retirement. That’s an easy one. Beyond that, though, the timing of when you’ll need the money should influence how you’re investing it.

For retirement, assuming it’s a long way off, you can afford to be aggressive–and that aggressiveness will pay off in higher returns. For something like a down payment on a home you anticipate buying soon, you don’t want to risk a market crash right when you need the money, so you’ll want to be conservative with it. This is all part of financial planning.

Don’t Forget About Insurance

Insuring your prized possessions is important and part of financial planning, but even more important is insuring yourself. That is, making sure health and life insurance are handled in some way, and at least considering long-term care insurance.

We’ll start with the last one. Nobody wants to think about it, but getting old will happen, and can be very expensive.

If you’re young, start saving for it now. For most people, ‘self-insuring,’ meaning making sure you have the resources yourself versus buying an insurance policy, will make sense.

The problem is nobody knows how much they’ll need, or if they’ll need it at all. The best we can do is make an educated guess based on heredity and health.

Health insurance and life insurance, however, are a bit more straightforward. You’ll want to be prepared to pay for supplemental Medicare insurance when the time comes; we hope we’re not the ones breaking it to you that basic Medicare won’t cover everything.

Putting money into a Health Savings Account (HSA), if you’re eligible for one, is a solid way to handle this issue.

Life insurance, too, is fairly cut and dried. Would your dependents be able to make ends meet (and then some) if something were to happen to you (or the family’s main breadwinner)? Life insurance can make sure they’ll be OK. Preparing for this is also financial planning.

Managing Complexity

As you get older and make money and maybe start a family, life will get more complicated. This rule definitely applies to personal financial issues too. Financial planning starts out pretty simply, but then gets more complex as you try to prioritize your goals, minimize your taxes, and prepare for retirement.

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate to contact us. If you see something that doesn’t look right, contact us!

Did you know that more than half of all American adults admit to living paycheck to paycheck?

This makes it very difficult for them to come up with the money for unexpected expenses. If you’re someone who falls into this category, you might want to take advantage of something called instant pay.

Instant pay services could help you get your hands on money that you’ve already earned when you’re in a bind.

Want to know what instant pay is and how it works? Our instant pay guide is going to break it all down for you.

Continue reading to learn more about instant pay and to get some instant pay tips that you can put to good use.

What Is Instant Pay

Instant pay is pretty much exactly what it sounds like. It’s a way for people to get paid what they’re owed by their employers prior to their next scheduled paydays.

Rather than taking out a payday loan, people can get access to the money that they need through an instant pay company.

It’s a fantastic option for those who find themselves in a position where they need to obtain money fast for one reason or another.

How Does Instant Pay Work

Outside of the fact that instant pay can provide you with the cash that you need fast, it’s also so easy to secure it in most cases.

All you need to do is sign up for an account with an instant pay company that specializes in providing people with instant pay.

From there, you’ll be able to work out the details as far as how much money you can get from them in a hurry. It’ll be so easy to do that you’ll wish you had thought to do it sooner.

Who Can Provide Instant Pay Services

You shouldn’t trust just any instant pay company to set you up with cash when you need it.

Instead, you should rely on an instant pay company that you know you can trust.

Payactiv has earned an excellent reputation and can provide you with the instant pay services that you need.

You should strongly consider working with them the next time you need to get cash fast prior to the end of your pay period.

Use Instant Pay Today to See How It Can Help You

Now that you know the basics of instant pay, you should set out to utilize instant pay services.

You might be surprised to see how easy it is to get cash from an instant pay company.

You won’t have to worry about trying to take out loans in between paychecks anymore when you find yourself in a tough spot financially.

You’ll be able to turn to an instant pay company for assistance so that you can sleep a little bit better at night.

Would you like to get some more personal finance tips involving instant pay and your other options?

Check them out by reading the other articles posted on our blog.

Conclusion

We hope you enjoyed this article… What are your thoughts on What Is Instant Pay

Please feel free to share with us in the comments section below.

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate to contact us. If you see something that doesn’t look right, contact us!

What Exactly is a Budgeting App? Purpose of a budget?

Budgeting App Apps or budgeting Applications that had a better overall rating in comparison to the amount of reviews they had also rated higher on our list, as did apps that were available for no cost at all.

In addition, we placed a priority on mobile applications that included advanced security features such as biometric authentication, multifactor authentication, and encryption.

Apps that allow for the connection of an infinite number of accounts went closer to the top of our ranking, as did apps that also have a website version and permit sharing with members of the user’s family or friend group.

What exactly is a budget?

A budget is an estimate of an organization’s revenue and expenses for a predetermined period of time in the future. Budgets are typically produced and reassessed on a regular basis.

An individual, a group of people, an organization, the government, or virtually anything else that earns and spends money can create a budget for themselves. Budgets can also be created for organizations.

It is vital to create a budget so that you can keep track of your monthly costs, be ready for the unexpected things that happen in life, and have the financial flexibility to buy expensive items without getting into debt.

You don’t need to be brilliant at arithmetic, it doesn’t have to be a chore, and it doesn’t mean you can’t buy the items you want even if you are keeping track of how much money you earn and spend.

Simply put, it indicates that you will be more in charge of your finances because you will be aware of where your money is going.

What exactly is the point of having a budget?

A budget is not about depriving yourself; rather, it is about gaining control of your finances and your spending habits. Creating a budget shouldn’t feel like a kind of punishment to the person doing it.

Keep in mind that this is a plan for all of your money, including the money you spend on things that are just for pleasure. A budget doesn’t have to be rigid. In point of fact, it should be revised whenever your circumstances shift, such as when you obtain a pay raise or when you purchase your first home.

The goal is to personalize your budget as much as you can while yet providing some wiggle room for changes. There will be unexpected occurrences (as well as errors).

Why is it vital to create a budget?

Everyone, not only those who are having trouble financially, can benefit from creating and sticking to a budget. It instills the value of living within one’s means and putting one’s money to work in the most productive manner possible.

Consider a budget to be a stepping stone on the path to achieving your financial goals.

Where do you even begin with a budget?

Are you prepared to give budgeting a try? Begin with the fundamentals. This includes keeping a record of all of your expenditures, as well as your income, account balances, and obligations.

After that, you should determine your priorities and search for a budget system that is tailored to your requirements.

How to Prepare a Budget

Knowing how much money you actually bring in each month in addition to how you actually spend it is essential to the process of successfully creating and keeping a monthly budget.

Therefore, your income and your expenses make up the two most important aspects of any conventional budget.

To start, determine your entire monthly income by adding together all of your active and passive income, as well as your salary, wages, tips, interest, and any child support or alimony payments.

Next, make a list of your necessary monthly expenditures. This could include expenses such as rent, insurance, utilities, fees charged by the bank, and the minimum payment required on a credit card.

Next, make a list of all of the things that you routinely spend money on but that aren’t absolutely necessary.

Include things like recurring monthly subscriptions, streaming services, the average cost of your meals and entertainment, and everything else that falls into this category.

Check your previous bank statements and credit card statements to confirm that you have not overlooked anything. To calculate your overall monthly costs, add up all of your essential expenditures and subtract all of your discretionary costs.

Is the sum of your income and your spending larger than one another?

If that’s the case, you’re off to a good start. However, if your account balance is not where you would like it to be, it is necessary to make a budget. Having a clear understanding of your objectives will assist you in selecting the most suitable budgeting tool for your specific requirements.

Why Is It Necessary to Have a Budget?

According to a number of surveys, more than half of American adults live paycheck to paycheck, making budgeting an essential tool for assisting individuals in escaping the cycle of financial instability and establishing long-term financial security.

Over the course of the past three decades, the cost of housing and medical care has skyrocketed in the United States, which has reduced the amount of money available for savings and retirement planning.

If you do not have a financial plan or budget in place, you may feel stressed and overwhelmed, which can lead to increased spending, living beyond one’s means, and the continuation of vicious cycles.

But having a strong budget in place as part of your overall money mindfulness can make a significant impact.

This is true not only because it can help you reach your financial objectives, but also because it can reduce stress and worry and improve your entire quality of life.

What Characteristics Do Successful Budgets Share?

Establishing a budget is a process that starts with determining your monetary objectives, as well as keeping track of your typical spending and saving behaviors.

When you have a thorough understanding of how much money is going out and coming in, you are better equipped to deal with the expected as well as the unforeseen monetary obstacles that life throws at you.

The frame of mind with which you approach the management of your finances is vital. The creation of a budget is the essential first step toward regaining control over one’s financial situation.

In the event that you have never maintained a personal budget before, it is possible that it will take several cycles for your habits to catch up. In addition, if you have poor financial practices and want to improve them, the correct app can assist you.

What Exactly Is an App for Budgeting?

A budgeting app is a type of mobile application that is aimed to assist users in optimizing the spending and savings decisions they make on a monthly basis.

A budgeting tool can provide you more visibility into your financial choices and habits by centralizing all of your financial commitments and goals in one location.

A budgeting app, similar to the apps that your bank or credit union may offer for use on your mobile device, may give additional features such as the ability to create financial goals and track cash flow across several financial accounts.

Apps that help you manage your finances can be synced with your bank and credit card accounts to provide you a complete picture of your financial situation.

Some budgeting apps will adhere to a particular method of budgeting, such as zero-based or envelope budgeting, while others will take a more broad approach to budgeting and permit modification in accordance with the user’s personal requirements.

You can manage recurring bill payments, savings objectives, and monthly cash flow with the help of a fully featured budgeting tool, which can also assist you in tracking spending.

How Accurate Are Mobile Budgeting Apps?

The use of a budgeting software is a terrific way to make sure that you are actually sticking to your budget and not just preparing one. They are able to shed light on your spending patterns, illuminating where your money is going and pointing out areas in which you have room for improvement.

Just like any other program, the extent to which it “functions” is mainly determined by how its features are put to use.

One of the challenges associated with budgeting in general — whether it’s done via an app, a spreadsheet, or other, more manual ways — is making the commitment not only to establishing a budget, but also to making your financial decisions in line with what the budget dictates.

The ability of a budgeting app to provide interaction and automation, which may help keep users motivated to stay on top of their personal money, is something that a lot of people have found to be helpful.

How to Decide Which Budgeting App Is Right for You

When compared to other decisions pertaining to personal money, using an app for budgeting may appear to be a rather insignificant matter. However, selecting the appropriate budgeting tool can make a significant impact on the way your personal finances are managed.

When searching for a new software to help you manage your finances, make sure to put your requirements and objectives first.

The appropriate tool to assist you budget can give you with useful insights and data about your spending as well as your savings.

However, before that occurs, determining your financial goals can assist you in narrowing down your search for the most suitable budgeting tool for your needs.

Aside from your objectives, the following are some aspects of a budgeting tool that you should think about before making a commitment to using it:

Fees:

The prices of many budgeting programs can be found online. There are a lot of free budgeting applications, and even more that provide free versions, but some of them do demand a monthly price.

Don’t ignore the paid apps just because you’re drawn to the idea of downloading anything for nothing. If a budgeting software will help you considerably improve your financial outlook, it may very well be worth the expense to get the app.

Features. Because each app has its own set of features and benefits, it might make sense to try out a few various apps before settling on the one that is the most suitable for your requirements.

If you’ve ever used a mobile banking app, you already have some experience with the features you’ll want to look for in a new one.

The most popular budgeting apps typically include a variety of features, some of which are as follows: the ability to connect all of your financial accounts; the ability to receive notifications of upcoming bill payments; the ability to design a budget; the ability to track credit score; the ability to track spending; and the ability to set financial goals.

Security. The safety of your personal information is of the utmost importance, particularly with regard to financial information and login credentials.

Although the vast majority of budgeting apps offer some measure of protection, some are more advanced than others in this regard. Make it a point to investigate the degree of security and encryption provided by each app.

You might find security features on their websites, such as encryption of 256 bits and multiple-factor authentication, for example.

Intruders can be discouraged from accessing your information by adopting features such as this one, particularly when combined with the use of a secure Wi-Fi network.

Assistance to the customer If you are using a budgeting software and run into a problem, having access to a technical support team that you can get in touch with can be helpful.

When looking for a good app to help you manage your finances, you should make it a point to find out what kinds of customer care are offered by the app itself as well as, if appropriate, the desktop version.

Reading reviews written by others who have used the program that you are thinking about downloading might also be helpful.

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate to contact us. If you see something that doesn’t look right, contact us!

TIOmarkets Review: Why TIOmarkets is the Best Trading Company for You

When it comes to trading, there are a lot of different companies out there vying for your business. So, how do you know which one is right for you?

In this post, I’ll be giving my honest TIOmarkets Review, a company that offers its clients the ability to trade in a variety of financial markets.

TIOmarkets is a trading company that offers its clients the ability to trade in a variety of financial markets. These include forex, CFDs, stocks, commodities and more. They offer their services through a variety of platforms, including their own proprietary platform, MetaTrader 4 and 5.

Why you should choose TIOmarkets trading company?

There are many reasons why you should choose TIOmarkets as your trading company.

First and foremost, they offer a variety of services that can fit any trader’s needs – from those who are just starting out to those who are already experienced. They also provide excellent customer support, which is always a plus.

Another reason to consider TIOmarkets is that they offer some of the most competitive spreads in the industry. This means that you can save money on your trades, which can add up over time.

In addition, they offer a number of bonuses and promotions that can further help you save money or make money through your trading activities.

So overall, choosing TIOmarkets as your trading company provides numerous benefits that can be extremely helpful for any trader. Be sure to check them out today and see how they can help you reach your financial goals!

What are ecn brokers?

ECN brokers are electronic communication networks that facilitate the trading of securities. These brokers provide access to a variety of markets, including stock exchanges, dark pools and OTC markets. ECN brokers typically charge lower fees than traditional brokerages, making them an attractive option for active traders.

ECN, or electronic communications network, brokers are firms that provide traders with access to a network of other banks and liquidity providers.

ECN brokers allow their clients to trade directly with these market participants, rather than going through the broker themselves. This results in better prices for traders, as there is no “middleman” taking a cut.

The term “ECN broker” can refer to either the network itself or the brokerage firm that provides access to it.

In most cases, ECN brokers are large institutions with direct relationships with many market participants, such as banks and liquidity providers. This gives them an advantage in terms of both price discovery and execution speed.

There are several different types of ECN brokers, each with its own strengths and weaknesses.

The three most popular models are market makers, agency model firms and hybrid firms.

Market maker ECNs take the other side of trades themselves, while agency model firms simply route orders to other participants in the network. Hybrid firms combine elements of both approaches.

Choosing the right ECN broker is essential for any trader looking to maximize performance and minimize costs. There are a few key factors to consider when comparing different providers: commission rates, order execution quality/speed and platform features/usability (among others).

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate contact us. If you see something that doesn’t look right, contact us!

How Many Views Do You Need To Make Money On Youtube?

What is YouTube and How Does it Work?

YouTube is a video platform created by Google. It is a video search engine that allows users to upload, share, and view videos.

YouTube is the leading video platform in the world with more than a billion users worldwide.

It has been around since 2005 and has since grown into one of the largest online networks in the world. YouTube has been used for many purposes such as entertainment, education, and marketing.

YouTube is an online service that allows people to upload, share, and view videos.

It is impossible to tell how many views a video has unless you know exactly how many people will watch it.

In general, YouTube videos make you anywhere from $0.75 to $1.00 per thousand views.

You can also earn money from advertisements. Unless you have a huge following, the more views you get, the less money you’ll earn. However, if you create high-quality videos, you can make money on YouTube even without a huge following.

A YouTube channel that has reached this level is likely to attract product placements, endorsements, and sponsorship opportunities.

If you are well known, you can also use your channel to sell merchandise to your fanbase. Affiliate marketing is a good option for review-type channels.

Amazon offers a low one to 10% percent affiliate payment rate, which means you can sell products for a profit. Once you reach this level, you may even be able to sell your own product!

One of the best ways to make money on YouTube is through sponsored videos. These videos work a lot like affiliate marketing.

In exchange for your content, you will receive a fee from a brand. The income that you earn does not depend on how many people buy the product but on the number of viewers who view your message.

You need at least 1,000 subscribers to make money with sponsored videos. However, you may need to spend time creating videos to make money.

How to Increase Your YouTube Views and Reach Willingly?

There are many ways to increase your YouTube views and reach. The most popular way is to create a video that will be liked by the audience.

However, there are other ways that you can use to get more views on your videos such as creating an engaging thumbnail, using high-quality content, and even adding a call-to-action button.

YouTube is an excellent platform for marketing your business or brand. With more than 1 billion active users, it is one of the most popular platforms online today.

There are many ways to increase your YouTube views and reach such as creating engaging content with a compelling thumbnail, adding a call-to-action button in the description box of each video, etc.

How to Get 1 Million YouTube Views in One Month

There are many ways to do this, but the most important thing is that you should have a high-quality video. This is not an easy task for all users and it requires a lot of work

This is not an easy task for all users and it requires a lot of work and effort. It’s possible to get 1-million views if you have a high-quality video, but it’s not going to happen overnight.

Sometimes a lot of views are needed because you want to advertise your product or you’re trying to get into the top 100 on YouTube.

You can use third-party websites such as socialblade.com, youtube-mp3.org, and videoleap.com to find videos that have a high potential for views and edit them with music so they’ll get a lot of views.

How to Budget Your YouTube Channel’s Revenue

YouTube is one of the top video platforms today, and videos on this platform are monetized through views.

The question of how many views can you make money on YouTube has been discussed by many.

However, there are no definitive answers to the question and it depends on your channel’s niche.

The best way to budget your channel’s revenue is by breaking it down into each type of ad that you get. This includes video ad clicks, pre-roll ad breaks, and subscriptions.

So if you’re making $10 per day from YouTube ads, then your daily income will look like $10/$120 with 120 videos earning $10 each or $100/100 videos with 100 earning $10 each or anything in between.

If a video doesn’t make enough money it may be time for a rebranding or better marketing campaign rather than lowering the view count needed to monetize successfully.

Conclusion

We hope you enjoyed this article… What are your thoughts?

Please feel free to share with us in the comments section below.

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate to contact us. If you see something that doesn’t look right, contact us!

Credit card companies don’t operate for free, as you might expect. However, when you consider a $200 sign-up bonus for a credit card without an annual fee, you start to wonder how they continue to turn a profit.

How do credit card companies generate revenue when they appear to be giving away rewards for nothing? You shouldn’t worry, though.

No matter how many cash back rewards you receive, your credit card issuer is doing just fine. Additionally, all of the other credit card issuers that function as parts of the enormous payment card machine are.

The specific role that each type of credit card company plays in the payment ecosystem determines how they generate revenue.

Let’s begin by examining the various categories…

1. Credit card issuers

A credit card is a bank’s line of credit that you can borrow and pay back.

The bank that supports the credit line is the credit card issuer. The issuing bank pays the merchant when you make a purchase. When you use your credit card to make a purchase, the money is returned to the retailer by the card’s issuer.

The issuer is typically the only credit card company that cardholders directly interact with. (The most frequent exception to this rule concerns particular advantages provided by networks.

To file a claim for these, you may need to get in touch with that network.) You can actually handle your account if you have a co-branded retail credit card (also known as a store credit card).

2. Credit card networks

The use of a credit card typically involves a significant amount of conversation. The first step in completing a transaction is for the merchant to make contact with the bank and request approval.

After that, the bank will need to transfer the funds to the account of the retailer in order to pay for the purchase.

There is no one person or entity that is responsible for all of this communication between the merchant and your bank. Instead, everything is processed through a network that processes credit cards.

In the United States, the four most important credit card networks are as follows:

Each of a credit card issuer’s cards is associated with a different network of credit card issuers through a partnership. One and only one payment network is compatible with each individual card.

If you look for the network’s logo on the back of your credit card, you will be able to determine which network your card uses. Your credit is the only option available to you.

3. Credit card processors

Not only do most retailers not interact directly with the company that issued their customers’ cards, but they also do not interact directly with the networks.

Instead, the majority of merchants, especially smaller businesses, contract their credit card processing needs out to a third-party company.

Credit card processors, in their most basic function, play the role of an intermediary between the merchant and the network. This results in a number of distinct benefits for the merchant:

Processors, in contrast to issuers and networks, are not involved in any way with the particular credit card that you have.

You won’t find their logo on your card, and the choice of processor that a merchant makes will have very little bearing on the price that you pay for an item.

How credit card issuers make money from cardholders

When you have a credit card, you might get the impression that you are the primary source of revenue for the company that issued the card.

However, that is not the case at all. The issuer of a credit card is the only type of credit card company that makes money directly off of its customers. Other types of credit card companies only make money indirectly.

Fees are typically the source of revenue for card issuers from their customers, cardholders. The good news is that consumers who are knowledgeable about their options can sidestep the majority of these fees.

Annual fees

You, as the cardholder, are responsible for paying these fees in order to keep your account active.

The vast majority of credit cards that assess an annual fee are rewards cards.

In this instance, annual fees help offset the cost of those rewards by providing some additional revenue. On the other hand, some credit cards designed for people with poor credit also impose annual fees on their customers.

When it comes to these credit cards, the annual fee helps the issuer mitigate some of the risk that comes with extending credit to someone who has had credit problems in the past.

How to avoid annual fees

You can easily avoid annual fees by selecting cards that do not charge an annual fee instead of using cards that do charge an annual fee.

The majority of the best cash back rewards cards, for instance, do not charge annual fees to their cardholders.

You can even locate some respectable travel cards that do not charge an annual fee.

On the other hand, there are cases in which annual fees are money well spent.

For instance, many of the best travel rewards credit cards offer sign-up bonuses and other benefits for cardholders that can have a value of several thousands of dollars.

Interest fees

The majority of an issuer’s profit comes, in most cases, from interest and other fees.

When you continue to carry a balance on your card after the due date, the card issuer will assess you with these fees.

When you use your card to make a purchase, the issuer of the card is the one who actually makes the payment to the merchant. The issuer will be out of pocket for that amount of money until you pay off your balance.

The issuer receives compensation in the form of interest fees for the lending.

The amount of interest that you are charged is expressed as a percentage of the total balance on your credit card. This percentage will change based on the annual percentage rate, also known as the APR, of your credit card.

If your annual percentage rate (APR) is high, then your interest fees will also be high.

The annual percentage rate (APR) charged by credit card companies is usually reflective of your credit risk, which is determined by your credit history.

If you have an outstanding credit history, you should have no trouble obtaining a loan.

How to avoid interest fees

There are primarily two ways to keep from having to pay interest fees. Paying off your balance in full each and every month is the simplest option.

The reason for this is that the majority of credit cards come with a grace period during which you won’t be responsible for paying any interest fees.

This grace period begins once your statement is closed and continues until the due date that is listed on your bill. An alternative strategy for evading interest fees is to take advantage of a promotional interest rate offer.

After opening a new account, new cardholders of many credit cards are eligible for an introductory deal that grants them a lower (or even zero) interest rate for a specified period of time.

These introductory offers of 0% APR can last for anywhere between six and twenty-one months (or, rarely, longer).

Transaction fees

A fee is typically assessed for most types of credit card transactions, with the exception of straightforward purchases. For instance, you will be required to pay a balance transfer fee if you decide to transfer an existing balance.

The same principle applies to cash advances on credit cards. When you make a purchase in another country or currency, many credit cards will charge you additional fees known as “foreign transaction fees.”

How to avoid transaction fees

Transaction fees can be easily sidestepped by merely avoiding the kinds of transactions that incur them.

If you never make a balance transfer, you won’t be subject to the fee that is associated with doing so.

The same can be said for cash advances. If you travel quite a bit, avoiding fees associated with foreign transactions may be more difficult for you. However, many excellent credit cards, particularly travel credit cards, do not impose any fees on transactions made in a foreign country.

Penalty fees

When you sign up for a credit card, you are entering into a legal agreement with the card’s issuing bank.

The majority of issuers will charge you a fee if you violate the terms of that contract in any way.

For instance, if you pay your bill after the due date, the company that issued it to you will most likely charge you a late fee. In a similar vein, you might be required to pay an over-limit fee if you spend more money than your credit limit allows for.

How to avoid penalty fees

You won’t be subject to any penalty fees if you follow the guidelines outlined in your cardholder agreement.

If you are consistent about paying your bills on time each month, you can avoid incurring late payment fees. If you have trouble keeping track of when payments are due, you might want to ask your bank about the possibility of setting up automatic withdrawals.

Fees for going over your credit limit can also be avoided by maintaining a balance that is significantly lower than the limit.

Many card issuers even provide customers with the option to completely disable the ability to make purchases that would cause them to go over their spending limit.

How credit card companies make money from merchants

Even though credit card issuers are the only card companies that profit directly from cardholders, virtually all card companies profit from merchants.

Issuers, networks, and processing companies all get their cut from merchants in the form of various processing fees. Merchants pay all of these fees.

Interchange fees

When you use your credit card, the company that issued your card will charge the merchant a fee so that they can process the transaction.

This type of fee is known as an interchange fee. The percentage of the total amount of the transaction that is applied toward the cost of the interchange fee can range anywhere from 1% to 3% of the total.

However, the precise amount of the interchange fee can vary quite a bit depending on the issuer, merchant category, payment method, and even the card that is used to make the purchase.

Your credit card company will charge you interchange fees to cover the cost of maintaining your credit card account, which includes taking preventative measures against fraud and maintaining account security.

As long as you continue to use your credit card for purchases, the issuer of your card will still see a profit from your account even if you never pay any fees associated with it, including annual or interest fees.

For this reason, issuers will close accounts that have been inactive for an extended period. If you are not currently making use of your

Assessment fees

Both cardholder fees and interchange fees are used to cover the costs incurred by the issuer. So, how exactly do the networks for credit cards make money? The purpose of the assessment fee is to cover these costs.

Questions People Are Asking

How does a credit card company make its money?

Credit card companies generate revenue from cardholders in a variety of ways, including the collection of interest, the charging of annual fees, and the imposition of various other fees, such as those associated with late payments.

How do credit card companies make money if you pay the balance in full?

Even if you pay in full, credit card companies can still make money in a variety of ways. Card issuers can charge an annual fee to cardholders. Additionally, card networks and processors charge transaction fees to merchants. As long as you use your credit card, credit card companies can make a profit.

What are three ways credit cards earn revenue?

Credit card companies have developed multiple ways to make money over the years. The three most prominent are through interest payments, credit card fees, and transaction fees. If you’re smart, there are ways to avoid these fees.

Do banks make money on credit cards?

Credit Card Interest and Merchant Fees Income The primary source of revenue for banks is interest on credit card accounts. When a cardholder fails to repay their entire monthly balance, interest fees are assessed to their account.

Does it hurt your credit to pay off credit card?

In most cases, paying off a credit card improves credit scores; in fact, the opposite is true. It may take a couple of months for paid-off balances to be reflected in your credit score, but reducing credit card debt typically results in a score increase if your other credit accounts are in good standing.

Do credit cards like it when you pay in full?

Always pay your credit card bill on time and in full is the most important rule for credit card use. By adhering to this simple rule, you can avoid incurring interest charges, late fees, and low credit scores. By paying your bill in full, you will avoid interest charges and improve your credit rating.

Why do banks try to sell you credit cards?

Selling credit cards contributes more to sales goals than opening a checking or savings account, creating skewed incentives based on the profitability of a product sold rather than how well it met a customer’s needs.

Accepting cards means you get paid faster.

Typically, payments from credit and debit card transactions are deposited within 48 hours. Compare this to the time it takes to send out invoices, wait for payment, and clear checks. In other words, card payments improve cash flow.

Why do merchants accept credit cards?

Accepting credit cards expedites payment. Typically, payments from credit and debit card transactions are deposited within 48-hours. Compare this to the time it takes to send out invoices, wait for payment, and clear checks. In other words, card payments improve cash flow.

Fact Check

We strive to provide the latest valuable information for our readers with accuracy and fairness. If you would like to add to this post or advertise with us, don’t hesitate to contact us. If you see something that doesn’t look right, contact us!

Top 13 Real Time Billionaires : How to Make Money Like a Billionaire

Are you interested in becoming a billionaire? If so, you’re not alone. Recent reports have shown that there are now more billionaires in the world than ever before, and the number is only growing.

This blog will teach you everything you need to know about real-time billionaires and how to make money like one of them.

First, we’ll explain what real-time billionaires are, and then we’ll provide a list of the top billionaires in the world as of September 2022.

In this article, we will be looking at some key lessons that can help you achieve wealth and success like these famous billionaires.

We’ll be discussing everything from business knowledge to marketing savvy – so make sure to read on if you want to learn what it takes to become rich like these people!

Next, we’ll give you tips on how to make money like a billionaire – from developing a successful business to investing in high-yield assets.

Finally, we’ll discuss what happens to billionaires’ wealth once they die. So if you’re interested in becoming a millionaire or even a billionaire yourself, read on!

The Billionaires annual ranking

The World’s Billionaires is an annual ranking that is created and published by the American business magazine Forbes in March of each year. This list is based on the proven net worth of the wealthiest billionaires in the world.

The list was initially published for the first time in March of 1987. The entire estimated net worth of each person on the list is given in United States dollars. This estimate is derived from the individuals’ substantiated assets and takes into consideration their liabilities as well as any other relevant aspects.

These lists do not include members of royal families or dictatorships whose wealth is derived from their positions of power.

This ranking is an index of the wealthiest individuals whose wealth has been substantiated, and it does not include any rankings of those whose wealth cannot be totally verified.

The year 2018 marked the first time that Jeff Bezos, creator of Amazon, was rated at the top of the list.

He also became the first billionaire to be included in the ranking, passing Bill Gates, founder of Microsoft, who had been at the top of the list for 18 of the previous 24 years.

Elon Musk overtook Jeff Bezos as the richest person in the world in 2022, after Bezos had held the top spot for the previous four years.

What is Real Time Billionaires?

Making money is something that most of us dream of doing one day.

For some, it happens overnight. But for the majority of us, it takes a bit more effort and patience. That’s where billionaires come in. They’re the people who make money in real time – as it happens. And to be a Real Time Billionaire, you don’t need to be a stock market genius or have a net worth in the billions.

In fact, you don’t even need to be rich! What you do need is to be smart and capitalize on the latest trends and technologies.

If you’re up for the challenge, then be sure to read on for some tips on how to make real money like a billionaire.

How to make money like a billionaire?

Money is the key to success, and becoming a billionaire is no easy feat. However, with a little bit of effort and know-how, you can be on your way to becoming a millionaire. Here are four essential strategies that will help you achieve wealth like a real-life billionaire:

How are the Rankings Determined?

It’s no secret that ranking high on search engines is important for businesses of all sizes. With that in mind, it’s worth knowing how the rankings are determined. The basics behind it include traffic volume, engagement rate, and time on site.

Rankings are also based on how important a given website is for a specific keyword or phrase. So, if you’re targeting a particular market and want to be at the top of the list, make sure you’re providing valuable content and keeping things fresh.

There are many ways to make money like a billionaire, so don’t be discouraged – stick with it and you’ll be on your way to the top!

Profile of Top Billionaires in the World [September 2022]

Becoming a millionaire is not as impossible as you may think. In fact, there are a variety of ways to make money like a billionaire, so it’s important to research the options available.

Depending on your interests and skills, you might be able to start your own business, invest in a profitable venture, or make money through commodity trading or investments.

Many millionaires live a luxurious lifestyle – they enjoy traveling, dining out frequently, and spending time with family and friends. So if you’re serious about becoming a millionaire, start by doing your research and finding an option that suits your needs! Happy millionaire-ing!

Today’s billionaire Winners and Losers

It’s no secret that being a billionaire is not a easy task. It takes determination, intelligence, and hard work to make it big in today’s world. That’s why today’s winners include those who are creative and innovative – they see opportunities where others don’t.

It’s also important to be aware of current events and trends. By staying educated, you’ll be able to stay ahead of the curve and make money like a billionaire.

However, it takes more than just luck – it takes consistent effort over time. That means you need to be prepared for long hours, frequent travel, and tough competition. So be sure to put in the hard work, and you might just be one step closer to becoming a billionaire yourself!

THE REAL-TIME BILLIONAIRES LIST

It’s time to make some real-time billionaires! In this episode, we share the tips and tricks that will help you become a billionaire-in-the-making. We start by exploring how to make money like a billionaire by starting your own business. This is easier than you think, and we’ll show you how in this episode.

Make sure to subscribe to our newsletter so that you don’t miss out on any of the next billion dollar opportunities! Next, we discuss ways to find hidden cash flows in your company and invest in them wisely.

Finally, we give you the real-time billionaires list – a list of people who have made their fortunes by exploiting unique business opportunities. If you’re looking to become a billionaire like these people, then you’re in the right place. Thanks for joining us!

Here are the Top 10 Real Time Billionaires

#1. Elon Musk – Net-worth: $254.6 B

Elon Musk is a business entrepreneur and investor. His full name is Elon Reeve Musk FRS. He is the creator of SpaceX, as well as its CEO and Chief Engineer. Additionally, he is an angel investor, CEO, and product architect for Tesla, Inc., as well as the founder of The Boring Company and the co-founder of both Neuralink and OpenAI.

Elon Musk is a clear example of how to be successful in any field, be it business or engineering. His latest venture – Tesla – is proof that hard work and innovation pay off. Other billionaires like Bill Gates and Steve Jobs also followed a similar trajectory to success. They were always open to new ideas, constantly evolving their strategies, and had the dedication necessary for long-term success. It takes luck too – just as it does in any other business venture.

#2. Gautam Adani & family – Net-worth: $149.8 B

Gautam Adani is one of India’s richest men and the owner of Australia’s largest coal mine, the Carmichael project. This has caused a lot of controversy as it would result in massive destruction to the environment. Born into a poor family in Rajasthan, Gautam Adani started out by selling tea from his bicycle.

He built his empire from scratch and without debt or any family connections – something that makes him very different from other business people. His frugal approach has helped him amass an enormous net worth- currently estimated at $19 billion!

#3. Bernard Arnault & family – Net-worth: $143.4 B

Bernard Arnault is a French businessman who was born on March 5, 1949 in the city of Roubaix.

He is best known for his position as the chairman and CEO of the French conglomerate LVMH Mot Hennessy Louis Vuitton SA, which is the largest luxury-goods corporation in the world.

The Arnault family are billionaires who made their fortune in luxury goods. They started out as a small luxury company back in the early days of the 21st century and today, they are one of the richest families on Earth.

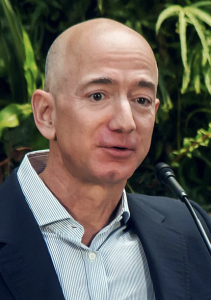

#4. Jeff Bezos – Net-worth: $137.2 B

Jeff Bezos is one of the richest people in the world and founder of Amazon.com – a company that has changed how people shop and consume goods. Born in 1964, Jeff started his career as a bookseller on the internet in 1994.

He’s is a commercial astronaut, entrepreneur, investor, and engineer specializing in computer technology who hails from the United States. He started Amazon, serves as its executive chairman, and was the company’s president and CEO in the past.

By 2000, he had founded Amazon Web Services, which provides cloud computing services to companies all over the world. In 2014, he was worth $135 billion – making him the richest man in history!

From 2017 to 2021, Bezos was the wealthiest person in the world. According to Bloomberg’s Billionaires Index and Forbes, Bezos is currently the second-wealthiest person in the world with a net worth of approximately 136 billion United States dollars as of September 2022.

#5. Bill Gates – Net-worth: $102.5 B

Bill Gates is one of the richest people in the world, as well as one of the most successful. Born in 1951, he started off selling software on university campuses before founding Microsoft – a company that would eventually become worth billions and change how people use computers. Although his wealth and success are largely attributable to his business acumen and dedication, Bill Gates has also been involved in philanthropy over the years.

He’s donated millions of dollars to various causes such as fighting polio and improving maternal health care worldwide. He’s also given back through leadership roles at organizations like The Bill & Melinda Gates Foundation – dedicated to helping solve some of humanity’s biggest challenges!

#6. Warren Buffett – Net-worth: $93.6 B

Warren Edward Buffett is a business entrepreneur, investor, and philanthropist who resides in the United States. He presently holds the positions of chairman and chief executive officer at Berkshire Hathaway. As of the month of September 2022, he is one of the most successful investors in the world.

If you aspire to become like Warren Buffett, then there are a few things you need to remember.

Firstly, regardless of your business status or existing financial position, the methods that work for him will also be effective for you.

Secondly, it’s important to stick with principles and never give up on anything – even in the midst of difficult times. And finally – don’t forget about patience! It can take time (sometimes many years) for businesses to grow exponentially and turn profitable; but if timed correctly, this journey towards billionaire-dom is definitely worth embarking on.

#7. Larry Ellison – Net-worth: $90.9 B

Larry Ellison is a business legend worth billions of dollars. Born in 1945, Larry started off his career as an engineer at IBM. In 1977, he co-founded software company Oracle with Curt Beldin and Frank Secunda.

Over the years, Oracle has become one of the world’s leading software companies and currently employs over 200,000 people worldwide. Apart from being very successful in his own right, Larry also has a wealth of knowledge to share with other business owners just starting out on their journey.

In an interview, we get to hear some great advice from him on topics such as staying focused and never giving up on your dreams; how to make your millions by creating successful businesses; the importance of networking; and more!

#8. Mukesh Ambani – Net-worth: $87.9 B

Mukesh Ambani is one of the richest people on earth and his story illustrates how you too can make money in today’s economy.

He has a history of investing his wealth wisely, for example by putting it into renewable energy and sports teams. This has helped him amass an immense fortune many times over – making him one of the richest people in the world!

If you are looking to achieve similar success, start by following Ambani’s footsteps. Be intelligent with your investments, be opportunistic when market conditions change, and always focus on growing your business at all costs!

#9. Larry Page – Net-worth: $85.5 B

Lawrence Edward Page is a business magnate, computer scientist, and internet entrepreneur who was born in the United States. He is most well-known for his role as a co-founder of Google alongside Sergey Brin.

Page was able to amass a considerable fortune as a result of his creation of Google.

According to the Bloomberg Billionaires Index, as of September 2022, Page is the seventh-richest person on the planet with an estimated net worth of $94.9 billion. This places him seventh on the list of all time.

Additionally, he has put money into the startup companies Kitty Hawk and Opener, which develop flying cars.

#10. Sergey Mikhailovich Brin – Net-worth: $82.1 B

American business magnate, computer scientist, and internet entrepreneur Sergey Mikhailovich Brin was born in Russia and raised in the United States. Together with Larry Page, he established Google.

Alphabet Inc., the parent company of Google, announced on December 3, 2019, that Brin will be stepping down from his post as president of the firm.

It has been claimed by Forbes that Brin is providing financial support for a cutting-edge airship project. Even though he is no longer Alphabet’s president, he continues to be the company’s controlling shareholder and a member of the board. He has one child with Shanahan in addition to the two children he had with his previous wife.

#11. Steve Ballmer – Net-worth: $78.0 B

Steve Ballmer is a billionaire and former CEO of Microsoft. His advice on making money in today’s economy offers valuable insight for people of all ages.

One of the most important things he advises is starting your own business. This isn’t only lucrative, but it also gives you total control over your career and life-path. He also stresses the importance of investing in stocks – something that can provide real long-term returns if done correctly.

Ballmer has authored two books – “Business @ The Speed Of Thought” and “Zero To One”. In them, he shares his insights and experience as one of the richest people in history as well as offers advice to young people about how to make their dreams come true.

#12. Carlos Slim Helu & family – Net-worth: $77.6 B

Carlos Slim Helu is a business entrepreneur, businessman, and philanthropist in Mexico. Forbes business journal consistently named Slim as the wealthiest individual in the planet between the years of 2010 and 2013.

He amassed his wealth through the enormous holdings of his conglomerate, Grupo Carso, in a significant number of Mexican businesses. This was the source of his fortune.

Carlos Slim is noted for being a serial entrepreneur and collecting a conglomerate of firms in Mexico that are involved in industrial production, infrastructure development, and telecommunications.

#13. Michael Bloomberg – Net-worth: $76.8 B

Michael Bloomberg is a billionaire businessman and politician who has had an illustrious career in the corporate world.

He is one of the most successful people in history, having founded several companies that have flourished under his leadership. Speaking about his successes, Mr. Bloomberg shares some great advice on how to become financially independent like him – by following your passion and not allowing anything to stop you from achieving your goals.

He also stresses the importance of being disciplined and staying focused throughout everything – no matter how tough the journey might be at times. These principles have helped him achieve amazing results in life and business, so if you’re determined to make it big too, heed these words!

Frequently Asked Questions