Welcome again to BiggerNews, the place we contact on the information, information, and all the pieces else affecting actual property investing. This time, the Dave duo hits on why mortgage charges shot down earlier this yr and what’s inflicting them to rise once more, plus what it will do to patrons and sellers who’re ready to get into the market. Then, we’ll hear how the BRRRR technique may very well be at risk as new mortgage guidelines make a cash-out refinance far tougher than earlier than. Ever thought, “We’d like extra artificially aware buyers.” In that case, you’re in luck! We’ll contact on how ChatGPT might permit an inflow of sub-par buyers to enter the market.

David Greene:

That is the Larger Pockets Podcast present 736. Fannie Mae got here up with a tenet and stated, “Hey, we’re not going to allow you to refinance something in case you’re pulling money out except it’s been seasoned for 12 months.” It was once six months. That is the place that six month rule that everyone appears to be like into that has to do with the Burr technique and, nicely, I can’t refinance for six months. It’s due to a Fannie Mae guideline. Now they’ve bumped it as much as 12 months. I don’t imagine they’ve stated why they’re doing it. My suspicions can be they’re making an attempt to make it tougher for buyers to purchase offers as a result of they need dwelling costs to return down with out having to lift charges much more. What’s happening everybody? That is David Greene, your host of the Larger Pockets podcast right here immediately with my co-host Dave Meyer, doing a particular version of Larger Information.

As you’ve seen, we’re in a gorgeous scenic place. We’re right here in Denver, Colorado bringing you one of many greater information episodes the place we’re going to be protecting what’s going on on this planet of actual property, what’s going on within the headlines and what it’s essential learn about them. We’re going to be making an attempt one thing new for Larger Information. Dave and I are going to be reviewing the highest headlines in the actual property investing area and speaking, commenting and diving into how they’ll have an effect on the actual property market and our place as buyers. Dave, good to see you.

Dave Meyer:

Sure, man, this can be a lot of enjoyable. First time we’re doing this in individual.

David Greene:

And also you’re much more good-looking in individual than you have been on digicam. I didn’t suppose that it might occur.

Dave Meyer:

Wow. It’s all this fancy gear they’ve surrounding us.

David Greene:

It doesn’t harm. That is how exhausting they set to work to make me look good, however hey, I’ll take it.

Dave Meyer:

I really feel like we’re going to interrupt one thing. It’s numerous costly stuff.

David Greene:

Sure, that’s true. Whenever you’re strolling via, you’ve gotten that very same feeling such as you’re at grandma’s home and also you’re in the lounge the place nobody’s speculated to go.

Dave Meyer:

Sure, precisely. And we appear like actual newscasters. We’ve bought our sheets of paper. We’d like a kind of little ear issues that they put in.

David Greene:

Sure. I’ll be Will Ferrell and you could possibly be Christina Applegate.

Dave Meyer:

Thanks.

David Greene:

All proper, nicely, why don’t we begin with the primary headline, what you bought?

Dave Meyer:

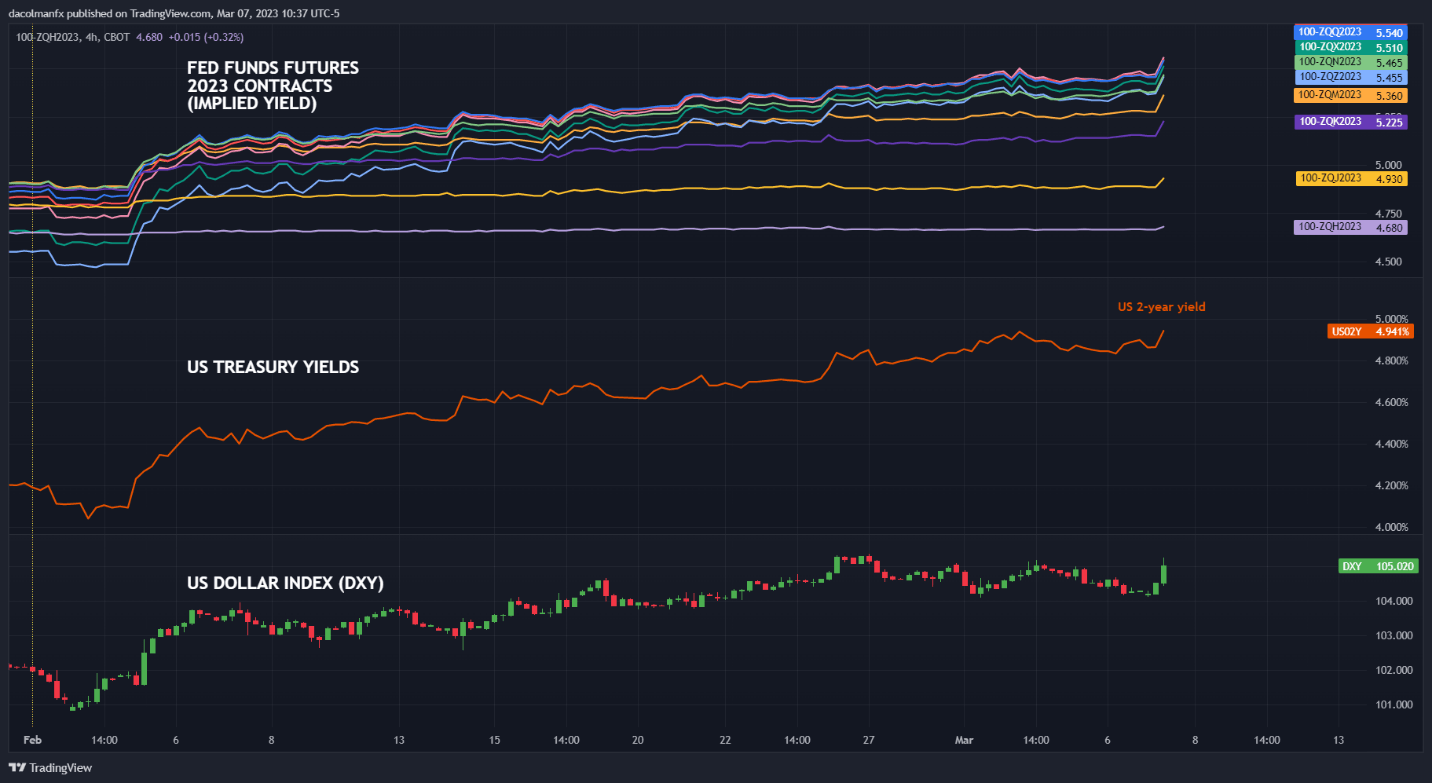

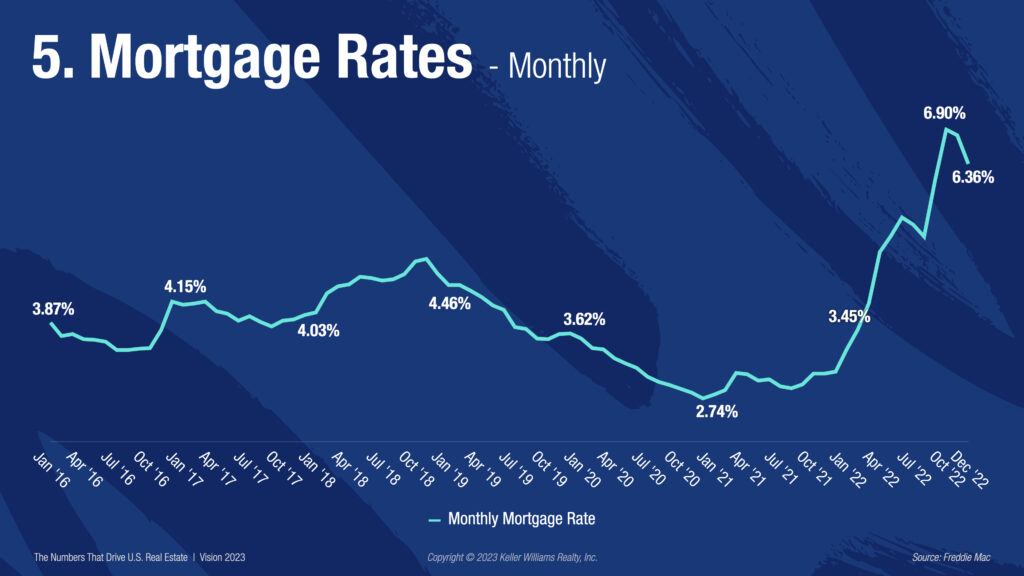

All proper, so our first headline, we have to speak about mortgage charges. I do know that is one thing we speak about rather a lot, however they’ve been actually unstable and only for some historical past right here, clearly everyone knows mortgage charges went up rather a lot final yr. For some time, it appeared like that they had peaked at about 7.4% again in November, they usually had fallen all the way down to virtually 6%. Now they’re again as much as virtually 6.8%, and numerous this appears to be due to latest financial information. There’s simply been numerous issues, two issues actually. One, a extremely robust labor report again in January and inflation information that was fairly ugly and disappointing, and this to me not less than looks as if this can be a inexperienced mild for the Fed to only maintain elevating rates of interest. What do you concentrate on that?

David Greene:

That’s what it appears to be like like proper now. They’re displaying fearlessness in relation to simply being prepared to proceed elevating charges, and we all know the explanation that they’re doing that’s they imagine that is going to cease inflation. That’s debatable whether or not it’s going to cease inflation, delay inflation, it undoubtedly has an impression on the economic system in some ways. We are able to’t predict right here, we don’t know, however I might count on charges to proceed elevating and each time that there’s something lower than optimum within the economic system typically, they usually suppose that costs are going to get too excessive or unemployment is simply too low, we’re going to lift charges to attempt to flip that round, which clearly impacts our place as actual property buyers.

I feel that is one thing that’s very tough is we usually base our selections off of a comparable worth for a house, and when charges bounce round like this, the worth of properties bounce round like this too, it makes it very tough to only not have a shifting goal the place you’ll be able to drill in and say nicely, that is what a home is value. Have you ever seen inside the greater pockets neighborhood frustration or perhaps some hesitancy of individuals to maneuver ahead and pull the set off the place earlier than they could have finished it after they felt extra stability?

Dave Meyer:

I hadn’t actually thought of that time, in regards to the calming side of this, however it does appear to be for some time in January and February, I feel we talked about this not too long ago, that individuals have been beginning to get again into the market just a little bit. And other people have been beginning to really feel like inflation was on a constructive pattern, mortgage charges have been trending downwards, however now that it’s reversed, I do suppose there’s a danger that there could be some demand pulling again out of the market not less than for the following couple of months, however I don’t know but.

I feel it’s simply going to be actually exhausting for people who find themselves new to this to leap in with all of this volatility as a result of it’s up, it’s down. It’s actually exhausting to get a beat on it, and except you’re an skilled investor who has been via one thing like this or simply is aware of your numbers so chilly that you just’re may be assured whether or not your mortgage is six and a half or 7% that your deal goes to work out. I do suppose there’s an opportunity that individuals take a step again and pause not less than until there’s some extra stability.

David Greene:

We have been speaking earlier than we recorded about what you name the pump and glide technique of driving the place my Uber driver was making me sick as a result of they hit the fuel after which they take their foot off the fuel and the automotive slows down.

Dave Meyer:

For those who drive like that, please cease for all of our sakes. Simply don’t drive like that.

David Greene:

Nicely, it made me suppose that’s what the market’s doing. Is you’re seeing, we simply had, on the David Greene staff, a extremely good February as a result of charges had simply come down, so it was like we’re shifting ahead, after which the charges come up and all the pieces slows, after which it’s shifting this forwards and backwards, and buyers are having a really exhausting time getting a grip. So what I might count on for perhaps not less than the close to future in 2023 is you’re going to proceed to see patrons leaping in as a gaggle and patrons withdrawing as a gaggle, and also you’re form of enjoying this recreation the place you’re making an attempt to catch the wave. Possibly you’ll be able to consider kinking a hose, letting it out, kinking a hose, letting it out, and so long as rates of interest maintain doing this, we in all probability simply should get used to the truth that that is how the market’s going to function.

Dave Meyer:

Completely, and I feel stock goes to be form of the identical manner, proper?

David Greene:

Sure.

Dave Meyer:

We’re beginning to see extra individuals begin to listing their property.

David Greene:

As a result of the charges went down. They suppose they’ll promote for extra.

Dave Meyer:

Precisely. So there’s simply going to be, such as you stated, the pumping glide impact, and sadly it simply doesn’t appear to be there’s a very good line of sight on financial stability. Inflation was trying good, took a step again. We’re listening to numerous layoffs within the job market and tech market. Tech makes up 2% of the labor market, and now we’re seeing that the January labor numbers have been truly fairly robust, surprisingly robust, and it simply exhibits that nobody actually is aware of what’s going to occur proper now, and all of us simply should admit that and count on a few of this volatility. It doesn’t imply you’ll be able to’t discover offers, however you shouldn’t count on issues to be clear I feel for the following, not less than three, perhaps six months, after which hopefully by then we’ll not less than know some course, whether or not good or unhealthy, which manner issues are heading as a result of it’s simply so murky proper now.

David Greene:

Now, the excellent news in case you’re trying to purchase on this market is that sellers are feeling that very same factor. They’re placing their home in the marketplace, then they’re listening to the labor report come out, they’re seeing rates of interest go up. They’re additionally going from greed to concern they usually’re biking. So if you’re out there to be shopping for a home, whether or not you simply wish to reside someplace otherwise you’re trying to make investments, you’ve bought your eye on a property, you’re ready on the fitting time. I at all times watch the information and I look forward to the doom and gloom, after which I’m going, proper, extra aggressive presents, and that’s labored for me a number of instances the place a vendor noticed the identical information and we’re like, Jerome Powell simply stated they’re taking this factor to the moon. I must promote now earlier than there’s blood within the streets. After which three months later, charges got here proper again down once more.

Dave Meyer:

That’s superb recommendation. All proper, nicely, perhaps someday we’ll cease speaking about mortgage charges, however that’s not immediately.

David Greene:

It’s given fairly a little bit of fodder to get into, proper?

Dave Meyer:

Sure.

David Greene:

There’s at all times some new dramas. Mortgage charges are the Kardashians of the actual property market now.

Dave Meyer:

Sure, precisely. They’re. Everybody needs to know. However there are different good headlines for us to speak about. The second immediately is about refinancing and actually will impression one in every of your favourite methods. The Burr technique. What occurred was on February 1st, Fannie Mae, which is a huge mortgage lender, authorities backed entity, up to date its eligibility coverage for money out refinance transactions to require that any current first mortgage be paid off via the transaction, be not less than 12 months outdated as of measured from the word date of the present mortgage to the word date of the brand new mortgage. So firstly, are you able to simply clarify what which means to everybody?

David Greene:

Sure, so Fannie Mae. You’ve usually heard the identify Freddie Max, one other one. This isn’t going to be completely correct, however typically, they’re the enterprise that can purchase the loans from whoever your mortgage dealer is if you’re getting standard financing. So as a result of they are saying, “Nicely, if we’re going to purchase a mortgage, it has to fulfill these pointers.” Now all of the mortgage brokers and the lenders go conform to what these pointers are in order that they’ll promote to Fannie Mae.

That is retains what we name liquidity out there. So if I lend you my cash and also you simply stored it for 30 years on that property, I can’t go lend to someone else. So by lending you the cash and then you definately go promote it to someone else and Fannie Mae finally ends up pushing a reimbursement in thumb after they purchase these notes, the federal government is ready to maintain charges decrease than they might usually be. Although charges are greater proper now than they’ve been historically, they’re nonetheless decrease than what they’d be if we didn’t have Fannie Mae.

Dave Meyer:

That’s proper.

David Greene:

Nicely, Fannie Mae got here up with a tenet that stated, “Hey, we’re not going to allow you to refinance something in case you’re pulling money out except it’s been seasoned for 12 months.” Now that was once six months. That is the place that six month rule that everyone appears to be like into that has to do with the Burr technique and nicely, I can’t refinance for six months. It’s due to a Fannie Mae guideline. Now they’ve bumped it as much as 12 months. I don’t imagine they’ve stated why they’re doing it. My suspicions can be they’re making an attempt to make it tougher for buyers to purchase offers as a result of they need dwelling costs to return down with out having to lift charges much more. And so this offers a bonus to individuals which are only a main residence one that’s going to be entering into to purchase, and there’s additionally in all probability going to be a component of danger discount for them, as a result of when charges fluctuate like this, it causes just a little bit of tension in us patrons, however it causes huge nervousness within the lending trade.

So that they’re going to take this mortgage they usually’re going to promote this to a pool of people who find themselves going to purchase it as a mortgage backed safety. These individuals don’t wish to go make investments all their cash into rates of interest at 7% in the event that they suppose they’re going to be at 10% later or if charges are going to be happening, they’re going to wish to purchase extra after they’re at 7%. So the pricing of those loans bounces round each time that the charges bounce round. All of the individuals which are making loans proper now, they usually have about two and a half years earlier than they break even.

So if I give a mortgage to someone, the prices which are included in doing that, I normally don’t get my a reimbursement for about two and a half years. So that they don’t prefer it when money out refinances or fee and time period refinances occur steadily. They wish to gradual that down. So that is one other manner that lenders who’re truly placing cash into the market to sponsor these loans can shield themselves by not letting somebody go in, get a mortgage after which refinance six months later when charges are down by some extent and a half.

Dave Meyer:

That’s a extremely vital word as a result of at first my thought was sure, they’re form of taking purpose at flippers and maybe Burr, however it additionally actually issues that that is their enterprise mannequin and that they should become profitable as nicely, and they also’re in all probability doing it, I might think about some mixture of it. So what do you suppose? Is that this going to impression Burr?

David Greene:

Sure, I feel that is going to impression Burr. People who find themselves already combating Burr as a result of charges have been going up and values weren’t growing as quick as they have been. So one of many widespread errors I feel individuals make with the Burr technique is that they assume they bought to get 100% of their cash out of the deal and that they should do it in a six-month timeframe, that’s like a grand slam if you are able to do that. Whenever you examine it to the normal technique the place you place 20 or 25%, then you definately dumped one other 5 to 10% of the property worth, and on a rehab, you’re taking a look at someplace between 30 and 45% of the property’s worth is invested and caught in it. So in case you do a chicken and you allow 10% of your cash in there, that’s nonetheless a transparent win over leaving 35%.

It doesn’t should be 100%, however this does make it just a little bit trickier there. There’s little question about that, that these lending fluctuations are like an earthquake after which the ripples exit all all through the trade, however we’re having earthquakes each single time the Fed publicizes one thing new. It’s prefer it’s going this fashion, then it’s going that manner. So there’s all these adjustments which are taking place. It does have an effect on in all probability extra Burr than flipping as a result of it’s solely is for money out refinances. That is in case you’re trying to take more cash out of the deal than what you place in. So a flipper, they’re simply going to be promoting the word.

They don’t have to fret a few cash-out refinance, however it additionally makes it much more vital to concentrate to what’s happening within the match. I’ve been saying that is the time in actual property the place training info issues greater than it ever has earlier than. For a very long time, actual property was simply the identical factor for years, for many years, it didn’t actually change an entire lot, and now as we see these adjustments which are being made at a excessive stage are having huge, huge impression on the way in which that we’re doing enterprise and what we count on dwelling values to do.

Dave Meyer:

So what do you suppose individuals ought to do? Is there a strategy to mitigate this or one thing that you are able to do to proceed to do the delivery technique regardless of these new rules?

David Greene:

I feel it makes it tougher to do purchase a home, money out, refinance, get all of your a reimbursement, at six months purchase one other one. That was a supercharged technique that individuals have been, I used to be doing this too, rising your portfolio very, in a short time with the identical capital recycling it. These rules work, however you’re not going to have the ability to execute it on the similar pace. What this actually does is it advantages those that have a bigger portfolio of properties that have been gathered over an extended time period. So in case you purchased actual property constantly for the final 4 or 5 years, you’ll be able to nonetheless money out, refinance the stuff you purchased 4 years in the past, get that capital, put that again into new properties, after which refinance the stuff you purchased three years in the past. It makes it tougher for the one who’s making an attempt to get began.

So the recommendation that I’m frequently giving is one will maintain home hacking as a result of in case you might put three and a half % or 5% down, you don’t must do the Burr technique. There’s not an entire lot of cash you’re having to take out of it. That’s a method you will get your portfolio began choosing up steam. And the opposite one is simply to lower your expectations that actual property ought to by no means be a dash. It’s a marathon on a regular basis. So it doesn’t actually matter what’s taking place proper now since you’re constructing wealth over the following 10, 20, 30, 40 years, and as you choose up that steam, you’ll have the ability to do a cash-out refinance, constructing, use any of the instruments that we speak about with out these rules altering. They’re at all times instruments that have an effect on the brief time period, and if you will get out of the brief time period mannequin and right into a long-term mannequin, you’ll be able to function independently of these items.

Dave Meyer:

Sure, and that’s wonderful recommendation. I feel for the final couple of years, this low stock the place individuals have to purchase rapidly and promote, and there’s simply a lot happening frenzy and also you needed to transfer rapidly, not less than on the acquisition facet. Folks get ramped up they usually really feel like they should do all the pieces actually rapidly and it’s not needed. The opposite factor you are able to do too is if you wish to refinance one thing rapidly, you’ll be able to look into portfolio loans, as David was explaining, standard loans, conforming loans get bought and repurchased to individuals like Fannie Mae and Freddie Mac. Portfolio loans are when the financial institution maintain onto the mortgage, so perhaps they’ll be-

David Greene:

That was a great-

Dave Meyer:

… Emergence of portfolio lenders who’ll be prepared to do money out refis for buyers.

David Greene:

That’s an incredible level. Portfolio loans, you keep away from the entire Fannie Mae state of affairs. The opposite one which I forgot to say is DSCR Loans. We do numerous these on the one brokerage, and if you get that mortgage, it’s not being bought to a standard lender. It’s being bought in a non-public markets mainly. So a few of these DSCR lenders are going to comply with the Fannie Mae pointers as a result of they’re the large canine in cost. What they do, everybody else falls in line, however different ones gained’t. So asking a mortgage dealer or asking a lender, do you’ve gotten a DSCR lender that can do that with out making me wait 12 months? That’s one other workaround additionally. It’s just about simply applies to those that need the easiest fee and the easiest phrases they might get.

Dave Meyer:

Completely. However I really feel like when these rules occur in a capitalist system, somebody fills the void. And there’s going to be a lender, there’s going to be somebody who sees that buyers nonetheless need this sort of product and possibly will create one thing like that. It’ll in all probability take a short time, however.

David Greene:

That’s actually how DSCR loans got here to be.

Dave Meyer:

Oh, actually?

David Greene:

Sure. Somebody like me that has greater than 10 properties, I simply couldn’t get one other mortgage. I can’t get a standard mortgage. So there was sufficient those that wished them, they usually have been like, nicely, we are able to’t use Fannie Mae pointers for this individual. What can we do? We are able to use industrial underwriting requirements the place we simply take a look at the money move of a property we’ll qualify it primarily based on that, and that’s actually what occurred. Is that this new factor stepped into the place there was a necessity out there. So don’t panic. Don’t eat panic in Anikins.

Dave Meyer:

Cleansing round.

David Greene:

Wait, and there can be an answer that can come to fruition.

Dave Meyer:

Superior. All proper. Nicely, that is superb recommendation and one thing we’ll undoubtedly be keeping track of. For our third level, we bought to speak about Chat GPT.

David Greene:

Are individuals speaking about that now?

Dave Meyer:

I don’t know if we’re even a information present. For those who don’t point out it, you must speak about it. Have you ever used it but?

David Greene:

No, however everybody else has.

Dave Meyer:

I’ve.

David Greene:

I’m just a little scared to make use of it. Is that bizarre?

Dave Meyer:

You need to be since you’re going to love it.

David Greene:

That’s what I’m afraid of.

Dave Meyer:

So Chat GPT, in case you haven’t heard of it, known as a generative AI platform. Mainly what it’s you’ll be able to go on and textual content, you’ll be able to ask it questions and a pc program, which has studied 1,000s of textbooks and web sites and books. Will use the data from that finding out to type distinctive and novel solutions for you so you’ll be able to have an actual dialog with it. Truthfully, it’s fairly exceptional to make use of, and stuff like this has existed earlier than. However I feel what’s distinctive in regards to the latest advances is how conversational it feels, it form of feels such as you’re speaking to a different human being and it’s not as generic because it was once. And that is clearly only the start and the tempo of acceleration right here in Chat GPT, and it’s not simply Chat GPT. Bing additionally has a brand new program. Google is engaged on one known as Bard. So I feel it’s seemingly that a majority of these interactive AI programs are simply going to continue to grow and rising and rising from right here.

David Greene:

Do you suppose they’re going to get together with one another, or do you suppose we’re going to have a rivalry?

Dave Meyer:

Sure, see, everybody at all times talks about AI versus humankind because the battle which may occur. The matrix. Possibly it’s going to AIs versus one another, and we’re [inaudible 00:17:24].

David Greene:

[inaudible 00:17:24] related.

Dave Meyer:

Sure, precisely. It’s like Transformers.

David Greene:

It’s like Transformers versus human, misleading cons versus auto bots right here. Who’s going to win?

Dave Meyer:

Sure, however we’re nonetheless going to be the collateral injury.

David Greene:

Sure, that’s true.

Dave Meyer:

It’s form of enjoyable. And as a knowledge science background individual, I actually loved enjoying round with it. It’s fairly enjoyable.

David Greene:

What are a few of the stuff you’ve finished with it thus far?

Dave Meyer:

Oh, I used to be asking it actual property questions, actually. I began asking it information questions which isn’t superb at but, like decoding information. So my job is secure for not less than six extra months, however it does do a extremely good job of it… It’s what’s known as generative AI, so it might have a dialog with you, which is exceptional. And I used to be curious what your emotions about this and the way it’s going to impression the actual property trade.

David Greene:

I’m a little bit of a contrarian in numerous methods typically. I feel individuals ask the unsuitable questions generally. When individuals say, “How do I purchase actual property so I can stop my job in two years and by no means work once more?” Improper query. You’re in all probability going to get into the unsuitable offers if that’s what you’re making an attempt to do. Actual property works higher over an extended time period, shopping for in the fitting areas, letting an asset stabilize naturally over time than it does in case you simply rush in and attempt to purchase a bunch of $40,000 properties in some turnkey market that find yourself inflicting you complications. One of many unsuitable questions individuals ask is, “How do I make this simple? How do I automate this factor so I don’t should do the work?” And the issue with that strategy is as soon as it’s made simple, it may be replicated and amplified at a giant scale as somebody with extra capital assets than you’ll be able to are available in and do it very simply.

Dave Meyer:

Hey, you want a barrier to entry.

David Greene:

These are so essential.

Dave Meyer:

Sure, completely.

David Greene:

Sure. Think about in case you’re making an attempt to get individuals throughout a physique of water and also you’re the man that’s employed as a result of you recognize the place the rocks are, you recognize the place the sharks are, you recognize the place the areas that you could possibly get shipwrecked are going to be, you recognize the world very nicely. You’ll at all times have a job. The minute that you just take away all these and also you simply have a giant deep water, good channel, some big boat can are available in and cargo up far more individuals than you ever might and take them throughout and also you’re out of labor. That is the issue with us at all times searching for a straightforward reply. The minute actual property investing grew to become one thing that may very well be finished at scaled from all of the software program, the programs, the ways in which we have been capable of do it simply. BlackRock is available in they usually purchase all the homes.

So I’m anxious about AI doing the job of copywriting, doing the job of constructing your footage of your property look higher, taking a look at what short-term rental listings are doing nicely, copying it, after which simply blasting it throughout all people as a result of then you definately’re not profitable doing the job of what the very best individuals did. You’re simply leveling the enjoying discipline and now your property is not going to have a bonus over someone else’s since you pay extra consideration to it. That’s my concern for the way this might work with actual property investing is in case you have been a short-term rental operator and also you have been taking note of the market and your competitors was lazy they usually weren’t, you have been following the algorithm that Airbnb or VRBO had, you have been altering your description, you have been getting new footage taken, you have been including facilities as you noticed what was taking place out there, you have been the individual on that little raft navigating these harmful waters to assist individuals.

The minute that AI can are available in and do this for you, the one who’s not paying any consideration to their property will get all the advantages of what the great operator was doing. So one of many ways in which I’m taking a look at, I’m anticipating that’s going to occur. I’m making an attempt to determine what properties can I get into, what asset lessons might I purchase, what strategy might I take that would not simply be replicated? The hacks that we’re at all times searching for, do you bear in mind when Craigslist was model new if you would listing your Toyota Camry on the market, after which individuals realized in the event that they put Honda Accord within the description, that it could set off the search engine of those that have been searching for Honda Accords?

Dave Meyer:

Sure. Or everybody would put $1. So all the pieces, it doesn’t matter what your worth truly was, it could simply present up.

David Greene:

Sure, it was a manner of getting visitors to your web page you wouldn’t usually have gotten. That, I feel is simply going to occur all over the place, that sort of factor. And so I don’t know what the reply’s going to be but, however once I take a look at AI affecting actual property investing, it means the plenty will have the ability to do that. So that you’re going to should be further choosy in regards to the property you’re taking. So once I’m trying to purchase, let’s say a cabin within the mountains as a short-term rental, I must that cabin to have one thing that different individuals can’t replicate as a result of AI goes to have the ability to replicate any benefit I might need had in different areas. So AI can’t replicate a view that different cabins don’t have or a location that’s going to be higher. These fundamentals are the issues we speak about on a regular basis will develop into extra vital when know-how improves to the purpose that everyone loses their benefit. What do you suppose?

Dave Meyer:

Sure, that’s an incredible level. I completely suppose so, and I feel copywriting is certainly one in every of them. Something the place content material creation I feel goes to be actually attention-grabbing. People who find themselves advertising and marketing for properties, for instance, sending out mailers, that’s one thing AI might do actually simply and possibly write a fairly compelling letter to somebody. I feel as an agent, will probably be actually attention-grabbing. I learn some article about how brokers are already utilizing it to jot down their descriptions of listings that they’re placing up, which doesn’t appear that tough. I don’t know, however put numerous large adjectives and massive fancy phrases in there, however I’m positive there’s some artwork to it.

David Greene:

I’m positive that’s what they’re doing, they usually suppose that it makes their job higher. The issue is each itemizing’s going to learn the identical manner, so it’s not going to face out anymore.

Dave Meyer:

Sure, completely. So I feel it’s going to be actually attention-grabbing. I used to be saying I used to be asking it information questions, and it doesn’t actually do this but, however I do suppose that’s an inevitability. Finally you’re going to have the ability to say, what’s the very best money move market or one thing, and it’ll let you know, after which everybody’s going to go to that, like your level. And so I feel there’s going to should be this contrarian view the place there’s going to be should be some form of real thought management the place individuals truly are doing one thing completely different than everybody else, and you may’t simply comply with the herd of what the AI is telling you to do, however you’re truly going to should be doing the evaluation for your self and doing the exhausting work, such as you stated.

David Greene:

It’s an excellent level. If you concentrate on how most individuals make selections, they watch social media, they watch a podcast, they go on a weblog, they hear what everybody else is doing, then they go do it, and for some time, that has been a fairly good, stable technique. The issue is AI’s going to make this occur so rapidly that by the point you hear about what everybody’s doing, it’d already be finished.

Dave Meyer:

It’s identical to Jim Kramer, no offense to Jim Kramer, however these guys who speak about shares on CNBC. By the point it’s on CNBC, it’s already too late. And I feel there’s going to be some component of that in predicting actual property markets, the place to purchase neighborhoods, that form of stuff. Possibly I’m simply saying that as a result of I do this rather a lot with my time and I feel I can do it higher, however I do suppose they’re not less than going to try to start out doing that.

David Greene:

The opposite factor to be involved about or simply take note of with AI is the model of it we’re speaking about now’s radically completely different than what it’s going to be in six months.

Dave Meyer:

After all. Sure, completely.

David Greene:

So us considering that we are able to use AI to strategize what we’re going to do, it’s very doable by the point the individual listening to this hears it, it’s already advanced well past what’s going to occur. So-

Dave Meyer:

It’s already within the matrix, by the way in which.

David Greene:

Sure. If there’s somebody utilizing AI to construct their enterprise an unimaginable manner, how lengthy earlier than AI figures which you could ask it, nicely, assist me do what Grant Cardone [inaudible 00:24:30]. He goes, “Growth, right here’s the sport plan proper right here. Go do the identical factor.” How do I develop my followers from this to this? And it might simply do this for you. So I actually suppose that is going to make actual property extra precious as a result of enterprise I feel is simply going to be leveled out. The enjoying discipline goes to develop into very, very plain for therefore many individuals which are stepping into it, however actual property is one thing that persons are at all times going to look at. One cause why I’m extra excited by investing in actual property once I see all of the technological advances.

Dave Meyer:

That’s a extremely good level. Arduous bodily property is not going to be as-

David Greene:

AI can manipulate cryptocurrencies. They’ll construct it and manipulate NFTs. I can’t management something that’s taking place. It will be unable to, not less than I hope, construct one other property in the identical place the place mine is the place individuals wish to go to.

Dave Meyer:

Completely. All proper. So our subsequent headline is about Fb or their guardian firm Meta, which is able to now not help the flexibility for sellers, individuals who wish to promote actual property as a enterprise anymore. So that you mainly have to make use of your particular person private account. So for instance, in case you have been a automotive vendor up to now, you could possibly listing all your automobiles, despite the fact that that you just’re a enterprise on Fb now, solely a person who needs to promote a automotive or actual property in our trade are going to have the ability to do this. So this brings up numerous questions. I’m first curious, do you suppose that is going to impression people who find themselves wholesaling or making an attempt to promote companies and even searching for tenants?

David Greene:

I feel it can, however I feel this can be a constructive change for us in actual property. I don’t need some big home flipping enterprise or BlackRock to return in and say, “Hey, right here’s 400 homes that you could possibly purchase in the identical discussion board the place someone’s making an attempt to do a on the market by proprietor on a property.” So if we’re the investor, we’re searching for the deal, you wish to be individual to individual. I wish to be speaking to a different human that’s not skilled on this, that isn’t a enterprise that is aware of greater than I do. I wish to purchase a automotive from a daily Joe. I don’t wish to purchase a automotive from the dealership that has expertise and expertise, what provides them a bonus. That’s why you go to Fb market is to keep away from getting taken benefit of by the those that know greater than you. So I like Fb eliminating the professionals out of the mother and pop sort of a gaggle, which is cool as a result of we don’t see a lot of that in actual property. We’re shedding the mother and pop really feel as institutional cash form of comes into our trade.

Dave Meyer:

Completely. Sure. I feel it permits Fb to virtually specialize just a little bit extra. It’s like if you wish to see all of the offers {that a} agent has, go on the MLS, the MLS is [inaudible 00:26:57]. If you wish to discover tenants, you’ll be able to market that on dozens of various aggregator web sites. It’s truly good for Meta to have the ability to do that and permit individuals to promote particular person properties or to only have the ability to amplify their private companies and listings in a manner that they’re not competing with main companies. However I’m simply curious, do you suppose this has any danger? It seems like a few of the suggestions about that is that in case you’re a vendor and you must use your individual identify, that there could be a safety danger there.

David Greene:

Sure, I suppose. However that’s at all times been the case. For those who’re going to make use of Fb market, I imagine it’s linked to your Fb profile anyway, so individuals can discover out who you’re.

Dave Meyer:

And that’s true.

David Greene:

I don’t suppose it’s going to be extra danger that wasn’t there earlier than. I’d wish to see Airbnb do the identical factor. I don’t like once I’m searching for a Airbnb to remain at, after which some large lodge has their stuff on Air. I feel most individuals see that they usually’re like, I’m making an attempt to keep away from the large costly lodge and I’m making an attempt to search for a neighborhood individual to help or extra worth a much bigger area or much less cash, no matter it could be. Whenever you let the individuals which are professionals at doing this are available in, they simply bully all people else out. They’ve assets, they’ve advertising and marketing, they’ve expertise, they’ve expertise. We’re making an attempt to create virtually a barrier to that, like a barrier entry like we have been saying earlier than. So I’m glad to see Fb making this transfer. I might like it if VVRBO and Airbnb would take the same step. I don’t wish to see a Hilton itemizing once I’m searching for a short-term rental keep at in some metropolis I’m going to be visiting.

Dave Meyer:

Sure, completely. That is sensible. Do you suppose that is going to be the resurgence of Craigslist? Hastily it’s going to rise to the highest?

David Greene:

Sure. That’s what our producer Kaylin stated is that this going to be the rise of Superman Craigslist going to return proper again once more. I feel Craigslist has so many bugs, it’d be very tough. That’s why individuals moved into Fb market. They bought bored with.

Dave Meyer:

Nevertheless it’ll at all times be there. It’s like Craigslist, each different know-how can transfer mild years forward and Craigslist will nonetheless be there being the very same web site it’s at all times been.

David Greene:

Sure, it’s Jack within the Field. 2:30 within the morning, Jack within the Field is at all times there for you. Is it the very best expertise you’re going to have? No. Are you going to remorse it within the morning? Sure.

Dave Meyer:

Sure.

David Greene:

However it’s there.

Dave Meyer:

All proper. I’ve truly by no means been to Jack within the Field.

David Greene:

In your entire life?

Dave Meyer:

By no means. In the event that they didn’t actually have it on the East Coast the place I grew up. It’s like a West Coast factor, however.

David Greene:

I had no thought. I simply figured it was all over the place.

Dave Meyer:

I’ve by no means had it.

David Greene:

So do you’ve gotten a 24-hour place that you just guys can go to on the East Coast?

Dave Meyer:

Not-

David Greene:

You’re simply going to be hungry.

Dave Meyer:

… Consider.

David Greene:

The 7-Eleven.

Dave Meyer:

They’d have McDonald’s that was like 20-

David Greene:

24 hour.

Dave Meyer:

I grew up within the suburbs, so not there. All proper.

David Greene:

In all probability a very good factor.

Dave Meyer:

Sure. Subsequent time I come to California, we’ll go. So for our final one, we’ve got yet another headline, which is the Biden administration launched a framework for rental protections. And so that you’ve heard of this, I assume.

David Greene:

Oh, sure.

Dave Meyer:

And my tackle this, simply so everybody is aware of this, there’s numerous intention right here, stuff that they’re planning on doing, however there’s not numerous meat. There’s not rather a lot to sink your tooth into type an opinion on. However do you’ve gotten some ideas on what has been launched thus far?

David Greene:

Nicely, there’s a pair parts to it. One in all them has to do with my understanding, it’s limiting background investigations that may be finished in your tenant. So that they’re already beginning this in sure locations in California the place they’re making it unlawful for landlords to run a felony search on any potential tenant that’s going to be coming in. And so they’re claiming that it’s unfair to individuals who have a felony historical past that they don’t have the identical entry to housing that different individuals do. So it’s slipping into the honest housing ethos for sure jurisdictions, which clearly, it’s identical to each political change, it advantages some individuals and it hurts different individuals, or it advantages some methods and it hurts different methods. There’s at all times a give and a take. So in case you’re someone who’s coming from that place, you’ve had a tough time getting housing, this seems like a constructive change for you.

For those who’re a landlord who has been counting on felony backgrounds and assist make selections for tenants, it’s going to alter in all probability the place you’re going to take a position. I might assume within the cities that do enact these insurance policies, you’re going to see much less investor demand. It doesn’t imply homes aren’t going to promote, however you’re not going to have as many buyers going there. And if this does develop into a factor that turns into a sweeping regulation, that that is one thing the place landlords have much less authority or management or autonomy, I ought to say, over the selections which are made. The placement you purchase in will develop into further vital and perhaps the worth level.

So I don’t know precisely how that works out, however this would possibly have an effect on areas the place hire is $400 a month greater than it could have an effect on an space the place it’s $4,000 a month. So it’s one other factor to be desirous about if this does go, location goes to develop into completely different. After which in all probability another issues like Part eight I feel would achieve some traction. As a result of in case you’re getting paid from the federal government on your tenant, you’re not as anxious about what the person tenant goes to be as much as contemplating their potential to repay.

Dave Meyer:

That’s actually attention-grabbing. That’s one in every of them. I’m to see what they really advocate. And the explanation I used to be saying earlier than, what the Biden administration has introduced thus far is like they’re going to direct the FTC to look into this or the Shopper Monetary Safety Bureau to look into this. So we don’t know these particular strategies, however it does sound like they’re following the lead of California, and that could be one of many examples that they appear into. One of many different ones is the FHFA, which is the Federal Housing Finance Company announce it can launch a brand new public course of to look at proposed actions together with renter protections and limits on egregious hire will increase. This is able to solely be for federally backed housing, however curious what you concentrate on that.

David Greene:

Nicely, this can be a type of hire management. It’s not prefer it’s a brand new factor. We’ve had this for a very long time in sure areas, hire management is larger than others. Once more, I’m in California, so Los Angeles has important hire management. San Francisco has important hire management. Traders nonetheless do very nicely in these areas, however in sure conditions it might develop into problematic over time. So each now and again we’ll discover a San Francisco itemizing the place the owner will not be capable of improve the hire previous a sure level. So that you’ll get someplace the place honest market hire could be $5,500 a month, and there’s a tenant paying $1,200 a month, that can have an effect on the worth of the actual property important. They wish to promote this property, this triplex and two of the items are occupied at $1,200 a month. You may’t get a investor that’s going to go purchase that property.

But additionally, this bleeds into home hacking as a result of it’s not all pure buyers. There’s individuals in San Francisco that simply have common W2 blue collar employees that would not afford to reside there in the event that they weren’t home hacking. And now you’ve gotten two of your items that aren’t out there that may’t be rented out as a result of they’re occupied by under market rents. So I feel long-term, in case you’re taking a look at how this might have an effect on if these things does go, this is able to truly make, as a result of historically actual property has finished higher, the longer that you just personal it, this will flip the chances towards you in a few of these instances. So perhaps short-term leases will develop into extra well-liked.

There’s going to be much less long-term leases which mockingly would scale back the quantity of housing out there, make it worse for renters as there’s much less housing out there, there’s much less provide. So now landlords can cost extra as a result of the demand versus provide is all whacked out. So this sort of stuff, when it occurs, there’s winners and there’s losers in each class. You may’t simply blindly comply with a mildew. This makes the one who’s taking note of this stuff, it provides them a giant benefit over the one who purchased a property 20 years in the past and simply doesn’t take note of the market anymore.

Dave Meyer:

Sure, completely. You’re going to should be fairly nimble and to concentrate to this.

David Greene:

Sure.

Dave Meyer:

I do suppose this one is actually attention-grabbing as a result of what the Biden administration stated was they have been mainly taking a look at public backed properties, which isn’t an enormous quantity. I feel it’s like 28% of the market, however there was additionally a letter despatched to the Biden administration from some members of Congress encouraging a extra broad take a look at hire management. And I do suppose there’s numerous research, I’ve seemed into this, there’s an incredible Freakonomics podcast episode if anybody needs to take heed to it, in regards to the execs and cons of hire management. And it simply looks as if it doesn’t truly work, even for the meant impact, which is like even in case you wished to assist present honest and inexpensive housing for individuals, it truly actually helps the incumbents, just like the people who find themselves already in property.

David Greene:

That’s precisely proper.

Dave Meyer:

However for people who find themselves shifting to that city-

David Greene:

There’s less-

Dave Meyer:

… Shifting into that apartment-

David Greene:

[inaudible 00:35:14] To get into.

Dave Meyer:

It truly goes greater.

David Greene:

Sure.

Dave Meyer:

As a result of landlords must compensate for these, the individuals who keep of their flats for a very long time. So they really cost extra for people who find themselves shifting in. And there are some research in California truly, and I feel in Portland additionally, that goes up. So I perceive that there’s a difficulty with inexpensive housing. I simply hope that no matter comes out of this can be a proof backed answer that helps each side.

David Greene:

Nicely, my subjective opinion, once more, I don’t know that is going to occur. I’m not talking for anybody however myself, is that these adjustments make actual property investing much less passive than what it was once. So the concept of passive earnings purchase a pair properties, reside off the hire, by no means work. That’s getting tougher and tougher and tougher to do as we’re speaking about, you must keep on prime of the adjustments which are being made. If Chat GPT is available in and makes sweeping rules to the short-term rental market, guys like me, we purchase short-term leases. We rent a property supervisor. We’re like, you do it, I don’t wish to hear about it. Subsequent factor you recognize, income’s down by 60% as a result of my correct supervisor can’t get it booked as a result of all people’s utilizing the methods that they used to have a bonus in as an expert.

Nicely, now there are not any professionals as a result of Chat GPT can do it for everybody. Or like we have been speaking about with hire management. In order that makes the individuals which are investing in actual property have to concentrate to what’s happening with their property. It’s turning it extra into you’re a enterprise operator. You’re extra of an entrepreneur as you’ve at all times been an entrepreneur, however it requires extra out of you to handle properties than what it did earlier than, which supplies individuals listening to podcasts and studying the information and getting knowledgeable and benefit over the those that aren’t paying consideration.

Dave Meyer:

Completely. Sure. The operational load is-

David Greene:

It’s an effective way to encourage.

Dave Meyer:

Sure. It’s identical to you must run a enterprise, however hopefully you already knew that. For those who’re going to get into actual property investing, it’s not shopping for a bond. It’s not shopping for stuff.

David Greene:

Sure. And the individuals listening to us proper now, they’re nice. These individuals shouldn’t be anxious. It’s those that don’t learn about podcasts, don’t learn about YouTube, don’t learn books, don’t comply with what’s happening. Those that aren’t listening to this message, which are truly going to be those which are on the drawback.

Dave Meyer:

Sure. Completely. All proper. Nicely, these are all of the headlines I bought for you. I believed you probably did an incredible job placing these collectively.

David Greene:

Thanks. The manufacturing staff.

Dave Meyer:

Nicely, sure. This was all Kalin and Eric, however I thanks. It was actually useful listening to your opinions on all this, and hopefully everybody listening to this bought rather a lot out of it. We’d love to listen to your suggestions on it. For those who like this, please give us a 5 star evaluation, or you’ll be able to hit up both David or me on Instagram or wherever to provide us suggestions. I’m on the Information Deli.

David Greene:

I’m at David Greene 24.

Dave Meyer:

All proper. Nicely, thanks rather a lot, man.

David Greene:

Sure, thanks. And in case you guys like this present, go away us a touch upon YouTube. Inform us what you appreciated about it. Possibly we missed a headline that you just wish to hear about. Put that in there. We are going to take a look at that, and we’ll add that within the subsequent present. We actually do take a look at your suggestions, we take a look at your feedback, and we incorporate that into the exhibits we’re doing to make them pretty much as good as doable. So thanks for becoming a member of me, Dave. I’ll see you on the following one.

Dave Meyer:

All proper. Nice.

Assist us attain new listeners on iTunes by leaving us a ranking and evaluation! It takes simply 30 seconds and directions may be discovered right here. Thanks! We actually admire it!