Higher rates hurt bitcoin and risk assets as when the Fed raises rates, cash and Treasury bonds start paying a decent, guaranteed return, so investors have less reason to hold something that pays no yield and swings 5% in a session.

On the other hand, cooler inflation means the Fed has less reason to raise, so that pull weakens and money flows back the other way.

Elsewhere, brent crude advanced 1% to above $85 a barrel, a third consecutive day of gains, after President Trump threatened further strikes on Iran and the U.S. resumed its blockade of Iranian shipping through the Strait of Hormuz. Crude has now surged 11% in two sessions.

Equities took the same cue as crypto. MSCI’s Asia Pacific gauge climbed 2.3%, its biggest advance in a month, with technology shares leading. South Korea’s Kospi jumped 8.2%, retaking its position as the world’s best-performing major benchmark this year, and SK Hynix rose 13% in Seoul after its American depositary receipts surged 27%.

“Bitcoin remains a rate-sensitive risk asset rather than a macro hedge,” said Jeff Ko, chief analyst at CoinEx, who said the print as reducing ‘“immediate downside pressure without building a durable breakout.”

Core inflation at 2.6% is still above the Fed’s 2% target, so the print buys the central bank room to hold rather than reason to cut. Ko pointed to the September FOMC meeting as the next real macro test, along with the direction of the dollar and whether bitcoin ETF flows can sustain themselves.

Dell Technologies (DELL) is dealing with two very different trends right now. New industry data shows global PC shipments declined in the second quarter as rising memory and storage costs pushed PC prices higher and weakened demand. That news weighed on DELL stock because investors worry higher component costs could slow future PC sales. However, Dell still outperformed the broader market, shipping 9.3 million PCs and holding a 14% global market share.

At the same time, Dell’s core business remains incredibly strong. In its latest quarter, the company easily beat Wall Street’s expectations on both revenue and earnings thanks to booming demand for AI servers.

More News from Barchart

The stock has more than doubled over the past year as investors continue betting on Dell’s AI infrastructure business. Strong support from the Trump administration also helped fuel this rally recently. Trump asked citizens to “go out and Buy Dell computers,” which popped Dell’s shares even higher. But the question now is whether the stock has run too much or if there’s still room to run. Let’s find out.

www.barchart.com

Dell Is Gaining Market Share Despite a Weaker PC Market

The latest industry data isn’t encouraging for the PC industry. Global PC shipments fell about 4% year-over-year (YoY) to 65.7 million units during the second quarter as memory and storage prices climbed 20% to 40%. Higher component costs forced manufacturers to raise prices, leading many customers to delay purchases after buying earlier in the year.

Dell, however, performed better than most competitors. The company shipped approximately 9.3 million PCs during the quarter and maintained a 14% share of the global market. That suggests Dell continues taking market share even while the overall industry slows.

The weakness appears to be industry-wide rather than company-specific. Dell’s commercial customer relationships and enterprise focus have helped it outperform the broader PC market, although prolonged component inflation could still pressure demand over the coming quarters.

AI Business Continues to Drive Record Results

While the PC market faces challenges, Dell’s AI infrastructure business continues to deliver mind-blowing results.

During its fiscal first quarter of 2027, Dell reported revenue of $43.8 billion, up 88% YoY, comfortably beating analyst expectations. GAAP earnings per share surged to $5.24, while adjusted EPS reached $4.86, also ahead of Wall Street estimates. Net income climbed 256% to $3.44 billion, and free cash flow reached roughly $3.2 billion.

The biggest growth driver remains Dell’s Infrastructure Solutions Group. Revenue from servers and storage jumped 181% to $29 billion as enterprises continued investing heavily in AI infrastructure. Meanwhile, Dell’s Client Solutions Group, which includes its PC business, generated $14.6 billion in revenue, up 17% from a year ago.

Management also raised its full-year outlook, now expecting approximately $167 billion in fiscal 2027 revenue while forecasting around $60 billion in AI server sales.

Beyond earnings, Dell continues expanding its AI ecosystem. The company recently introduced new high-density PowerEdge servers through its Dell AI Factory partnership with Nvidia (NVDA) while also increasing shareholder returns through a $0.63 quarterly dividend and continued share repurchases.

DELL Stock Isn’t Cheap Anymore

Dell’s execution so far has been outstanding, but investors are paying a premium for that growth.

DELL stock trades at roughly 30 to 35 times forward earnings, far above traditional PC peers like HP. That higher valuation reflects investor expectations that Dell’s AI server business can continue delivering exceptional growth for years.

If enterprise AI spending slows, customers delay infrastructure upgrades, or higher memory costs begin affecting margins, investors could become less willing to pay such a premium multiple.

What Do Wall Street Analysts Think of DELL Stock?

Wall Street remains optimistic about Dell’s long-term AI opportunity, although price targets suggest the upside may be more limited after the stock’s huge rally.

Bank of America recently raised its price target to $246 and maintained a “Buy” rating. Evercore increased its target to $240 with an “Outperform” rating, while Citi lifted its target to $235 and also rates the shares Buy. Morgan Stanley remains more cautious with a $110 target.

Overall, analysts still rate DELL stock a “Moderate Buy.” After the bull run over the past year, the average 12-month price target of $489.14 is still giving 16% upside from the current share price, suggesting Wall Street believes much of the near-term AI optimism has room to grow.

www.barchart.com

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

The lack of Wikipedia coverage is a more acute concern in an era where more users get their information from AI tools like ChatGPT. The report cites data from the AI tracking site Profound, which shows that 7.8% of links to sources on ChatGPT go to Wikipedia, compared to 1.8% and 1.1% to Reddit and Forbes, respectively, in second and third place.

(Profound/Chainstory)

The report also cites data from Trakkr, which shows that Wikipedia accounted for 36% of the top-10 citation links on ChatGPT and 25% of the top 100.

(Trakkr/Chainstory)

Contrary to popular belief, not everyone can create a Wikipedia page. The domain for doing so involves passing through tiers of protection and moderation views, according to Chainstory’s report. Volunteer reviewer’s must check prospective new articles against a number of factors, such as notability, verifiability and reliable sources.

Even when an article clears the process, it can still be deleted by administrators or via a 7-day community vote, which cannot be appealed.

Not helping matters for crypto projects is Wikipedia’s guidelines for crypto-centric news organizations (including CoinDesk), which describe them as “overwhelmingly enthusiastic about cryptocurrencies” and “generally unreliable.”

Mainstream news outlets that cover crypto, such as Reuters and Bloomberg, are regarded as reliable, the report said,but they are less likely to explore niche areas of the industry, such as liquid staking and perpetual exchanges.

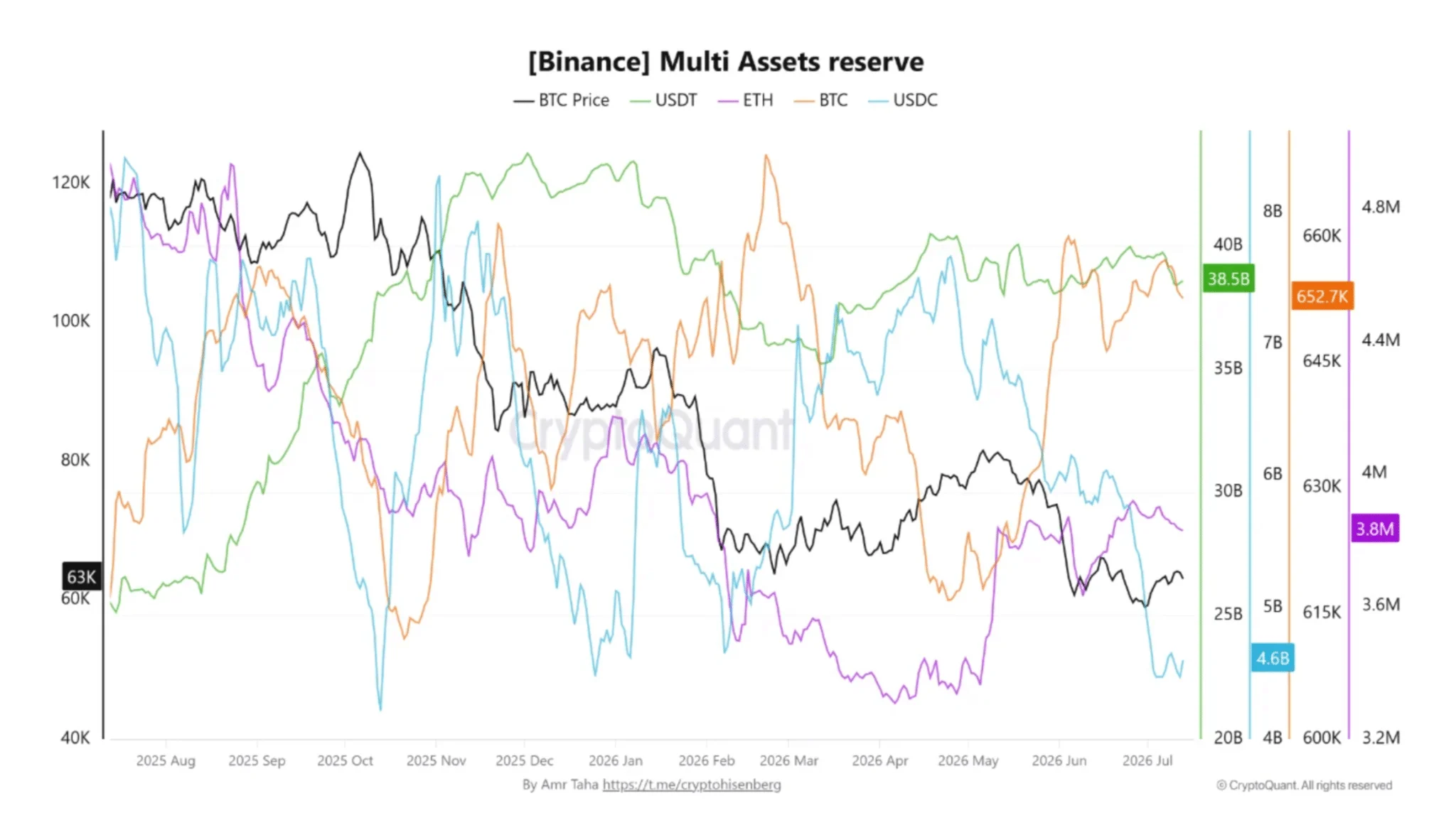

Binance continues holding deep stablecoin liquidity, yet its reserve mix has shifted noticeably in recent months. USD Coin [USDC] reserves dropped 40.3% from $7.7 billion to $4.6 billion as of writing, reversing most gains recorded during early 2026.

Meanwhile, Tether [USDT] reserves remained steady at $38.5 billion, widening the gap between both assets to nearly $33.9 billion. Such a divergence suggests that users prefer USDT over USDC for exchange balances, rather than signaling broad liquidity contraction.

Source: CryptoQuant

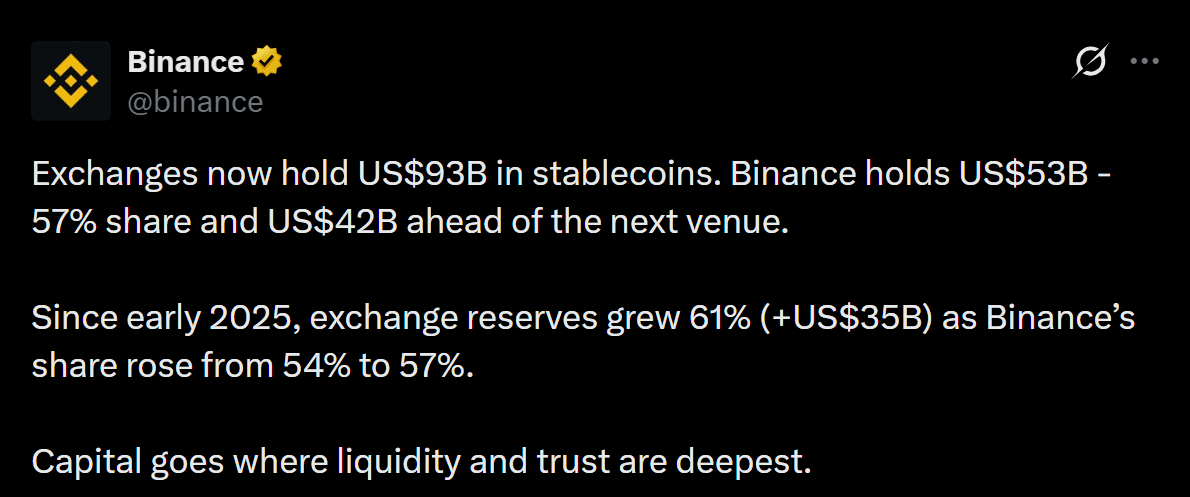

More importantly, Binance still controls roughly $53 billion, or 57% of the $93 billion held across exchange stablecoin reserves. Since early 2025, the dominant exchange stablecoin reserves have surged by 61%, adding $35 billion as Binance strengthened its market share.

Source: X

That preference strengthens Binance’s overall stablecoin base while concentrating liquidity in one dominant asset. If this trend persists, USDT could further reinforce its role as Binance’s primary settlement and trading stablecoin, while USDC risks losing relative market influence.

Stablecoin supply shifts beyond whale wallets

Still, that shift toward USDT has altered the way that stablecoin liquidity is distributed throughout the entire market. Over the last three months, the top 100 USDT wallets have reduced their portion of the total USDT supply by 0.6%.

Additionally, the largest USDC wallets reduce their portion of total USDC supply by 4.7%. Rather than concentrating liquidity among a handful of large holders, stablecoin reserves are spreading across exchanges, institutions, protocols, and retail participants.

Source: Santiment

This suggests capital is becoming more broadly available instead of remaining idle in whale wallets. As institutional adoption continues expanding, wider distribution could improve market resilience by reducing reliance on a few dominant holders.

Such a strong liquidity foundation could support healthier, more sustainable crypto market advances.

Can stablecoin liquidity drive the next rally?

The attention is now shifting from stablecoin liquidity to stablecoin participation. Rather than remaining just held by a few whale accounts, liquidity is increasingly spreading across a wider range of users.

This creates a better base of liquidity. However, just having broader ownership does not necessarily mean there will be a sustained bull run. Instead, active addresses, new wallet creation, and daily transactions must continue expanding to convert available capital into persistent demand.

Meanwhile, stablecoin supply remains near $312 billion, although risk asset accumulation has yet to fully accelerate. ETF flows and exchange balances also present mixed signals, suggesting much of that liquidity remains sidelined.

Therefore, the next advance in this market depends on investors’ willingness to utilize the available capital rather than how much capital is available.

Final Summary

Tether [USDT] continues strengthening its dominance as stablecoin liquidity becomes more broadly distributed.

USD Coin [USDC] and USDT now need stronger participation to drive the next market rally.

There’s a great deal to like about geothermal energy producer Fervo Energy (FRVO), including its large “potential backlog,” the fact that major tech and other energy companies have made deals with the firm, and its innovative technology. Most recently on the latter front, the firm disclosed significant improvement in its drilling rates.

Still, given the company’s enormous valuation, a meaningful logistical hurdle that it’s reportedly facing, and the weakness of FRVO stock in recent weeks, the shares appear to be too risky to hold at this point. Also worth considering, as I’ve pointed out in a number of articles, is the fact that the Street often is very bullish on new technologies in their early days and then subsequently sours a great deal on them. In fact, Fervo may already be undergoing this process.

More News from Barchart

About Fervo Energy

The firm has developed “enhanced geothermal systems” and seeks to deliver “utility-scale power.” In 2025, it generated just $138,000 of revenue, while its market capitalization is nearly $8 billion.

www.barchart.com

The Positives of Fervo Energy

The company has a huge “potential backlog” of $7.2 billion, and it has made power purchase agreements with a number of corporate heavyweights, including Alphabet (GOOG) (GOOGL), Shell (SHEL), and Southern California Edison, while Bill Gates and Alphabet are among its investors. A fairly large fossil-fuels exploration and development company, Devon Energy (DVN), has also invested in Fervo.

On the technology front, Fervo utilizes innovative “horizontal drilling and hydraulic fracturing techniques similar to what drove the shale revolution,” Politico reported. Further, on July 9, Fervo reported that it had improved its “drilling rates” by 143%. This accomplishment can help the firm attain its goal of lowering the cost of its first geothermal plant from a projected $5,500 per kilowatt to $3,000 per kilowatt in the long term.

Analysts are also tentatively positive on FRVO stock with a “Moderate Buy” consensus rating and an average price target that’s about 70% higher than its current price.

www.barchart.com

The Negatives of Fervo Energy

FRVO stock has a market capitalization of nearly $8 billion, even though analysts on average expect its revenue to come in at just $7.16 million this year and only $80 million in 2027. Even based on the 2027 figure, its price-sales ratio comes in at a gargantuan total of almost 100 times. Further, investment bank Jefferies has warned that the launch of the company’s energy systems could be delayed by electricity “transmission constraints” at “most (of its sites).”

Finally, in the last month, FRVO stock has tumbled 22%. In the past, I’ve noted that sometimes the shares of companies that have developed new technologies rise tremendously, only to subsequently tumble sharply. Among the energy companies that have undergone this phenomenon in the last 15 years are many solar energy producers, FuelCell Energy (FCEL), and Gevo (GEVO).

On the date of publication, Larry Ramer did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

It was just my husband and me at our kitchen table. All of the IVF supplies were out. Somehow, there were too many instructions, but also not enough. How do we know we’re mixing the medicine correctly? What if there’s an air bubble in the needle? What if there’s a really big air bubble?

I stood there half-naked with circles drawn on my belly to mark where to inject and where not to inject. And right as I was about to give myself the shot for the first time, my husband let out a nervous laugh.

I lost it. I was overwhelmed. Not just by the task at hand, but also by what the task would ultimately, hopefully, lead to: a baby.

I never told my husband this (or anyone else for that matter), but that night, I thought: I can’t do this. I’m throwing in the towel. It’s not too late to give up on IVF.

And yet, despite my conflicted emotions, it may surprise many to learn that we chose IVF proactively, not out of necessity, but because this is how we wanted to get pregnant.

Why we chose IVF

My husband and I delayed parenthood. We were both late bloomers. We both started new careers around 30, married five years later, and then a few years after that decided to try to have a baby. But by this time, I was 38 going on 39, so we chose IVF for three reasons:

Delivering a healthy baby: At my age, the chances of miscarriage and genetic abnormalities increase. With IVF, PGT-A (preimplantation genetic testing for aneuploidy) can be used to screen embryos for chromosomal abnormalities before transferring to the uterus. Selecting a chromosomally normal embryo may reduce the risk of miscarriage due to chromosomal abnormalities and lower the chance of transferring an embryo with certain chromosomal conditions.

Time and flexibility: We may want more than one child. As we age, our eggs only continue to deteriorate in quality, but with IVF, we will always have our embryos ready to go when the time is right for us. My age essentially becomes just a number.

Money: Both my husband and I received fertility benefits through our employers, so the financial burden of IVF wouldn’t be as heavy as it might have been; a true privilege that helped us make our decision.

The author said she and her husband have no regrets about living life to its fullest in their early and mid 30s.

Courtesy of Jacki Ochoa.

The right choice for our family

Don’t get me wrong. IVF is hard and expensive, and frankly, it is an emotional roller coaster. But I know in my bones that we made the right choice for our family. While my husband and I don’t have infertility diagnoses, genetic concerns, or really anything else (other than high cholesterol, oops!), because of my age, there are increased risks that keep me up at night.

With IVF, it matters less that I’m now 39 because doctors can carefully select the best, most healthy embryos.

That being said, we don’t know if our IVF journey will result in pregnancy yet. With one round of IVF, my body produced 34 eggs, resulting in 4 euploid embryos that are chromosomally normal. If the first transfer is successful, I’ll still have multiple embryos that could be used for future pregnancies, thus removing my age as a factor because they’ve already been deemed chromosomally normal and viable for pregnancy.

IVF gave us time back

My husband and I took our time starting our family, but we didn’t miss anything. We gained, we lived, we made memories together in our early and mid-thirties, and built a solid foundation for our relationship. And because of IVF, we hope to experience a healthy pregnancy and parenthood on our timeline.

They say time is our greatest, most expensive resource, and that’s exactly what IVF gave us.

This article is not a substitute for professional medical advice, diagnosis, or treatment. Always consult your qualified physician or healthcare provider.

Ironically, some critics of the bill have pointed to recent reporting by the Wall Street Journal on the Hong Kong exchange CoinEx as evidence of the risk. CoinEx is actually a story of how to use a public ledger to track, trace, and disrupt nation state activity.

Investigators traced roughly 3.84 billion dollars in transactions tied to Iran, connecting wallets controlled by Iran’s central bank to sanctioned military networks and to funds stolen separately by North Korean hackers. That level of detail is knowable today because it happened on a public blockchain, the same visibility critics are treating as the risk.

What the Clarity Act actually contains

Clarity contains nearly twenty distinct provisions addressing anti-money laundering, sanctions, and law enforcement authority.

As the bill is currently drafted, digital asset service providers get brought fully under the Bank Secrecy Act for the first time, with risk assessments, internal controls, a compliance officer, training, audits, and suspicious activity reporting all required.

Real-time information sharing between exchanges and law enforcement gets written into statute as recognized practice — the Beacon Network model of real time interdiction, seizure and disruption — replacing voluntary industry coordination with a legal standard.

An independent working group gets tasked with developing AI-powered tools to detect and disrupt terrorist financing and money laundering in digital asset markets. Kiosk operators face wallet pinning, hold periods, and daily transaction caps for first-time users, paired with blockchain intelligence requirements to catch scammers before funds leave the platform.