The FIFA World Cup has always been a spectacle of national pride, athletic drama and of course … billions of dollars in ad revenues.

As the tournament returned to North America this month, investors are increasingly asking not just who will lift the trophy, but how to get a piece of the economic action. Advertisements, streaming subscriptions and travel demand represent a meaningful slice of global consumer spending, not to mention opportunity for American brands to capitalize on new exposure to global consumers, said Jon Clements, managing director and co-founder of MarketDesk.

“Often, the best investment opportunities are found in secondary effects that are less obvious,” he said. “The World Cup is generating a lot of attention around US brands right now.”

You may have seen the memes: traveling sports fans experiencing American goodies for the first time, expressing awe online for treasures like Waffle House and Texas BBQ. That’s driving attention to American brands and opening them up to new demographics. It could also generate interesting signals for momentum investors over the following months, Clements said.

“You have a lot of global travelers in the US experiencing US brands, everything from Costco to food chains to different retail products that maybe are not available in their local markets,” he said. “Most US companies [already] operate on a very global basis, but I would imagine they’re collecting a lot of important data and information in terms of where there might be interest to expand markets.”

World Cup matches obviously also create demand spikes in the hospitality, airlines, ticketing platform and consumer discretionary sectors. Some of the largest funds in related themes include:

The Gabelli Opportunities in Live and Sports ETF (GOLS) holds Manchester United (which has several players currently represented in the cup) and is up 2.97% this year.

The US Global Jets ETF, which invests in commercial airlines and is up 10.98% over the same period.

Funds that track host countries at the macro level, like the iShares MSCI Mexico and Canada ETFs (which have the tickers EWW and EWC, respectively) could also benefit.

Data, Data, Data: Still, it’s going to take some time for the verdict to come in on which brands and regions show the most growth potential, Clements said. “Whether it’s Japanese tourists in Texas falling in love with different elements of US culture, these companies … [are] also collecting a lot more data,” Clements said. “Data is being collected in real time that I think you’re going to see being spoken about on earnings calls over the next two to three quarters.”

This post first appeared on The Daily Upside. To receive exclusive news and analysis of the rapidly evolving ETF landscape, built for advisors and capital allocators, subscribe to our free ETF Upside newsletter.

Bitcoin’s BTC$61,547.43 price drop ahead of Friday’s quarterly options settlement has once again cast doubt on the popular “max pain theory.”

The max pain level for this expiry stands at $72,000, significantly above current spot prices of around $61,700. On Friday at 8:00 ET, options worth $10 billion will expire on Deribit, the world’s largest crypto options exchange.

Max pain, as the name suggests, refers to the price level where options buyers – those who purchased call and put contracts to hedge against volatility – would lose the most money on expiry. In that scenario, option buyers suffer maximum losses, while their counter parties who sold options (also known as writers) stand to benefit.

The theory suggests that ahead of expiry, these option writers actively try to push the spot price toward the max pain level, effectively pinning bitcoin there. Crypto social media has long embraced the idea, particularly after BTC appeared to gravitate toward the max pain point ahead of several monthly and quarterly settlements in 2020–2021. That pattern, even if partly coincidental and driven by other market forces, helped solidify belief in the theory.

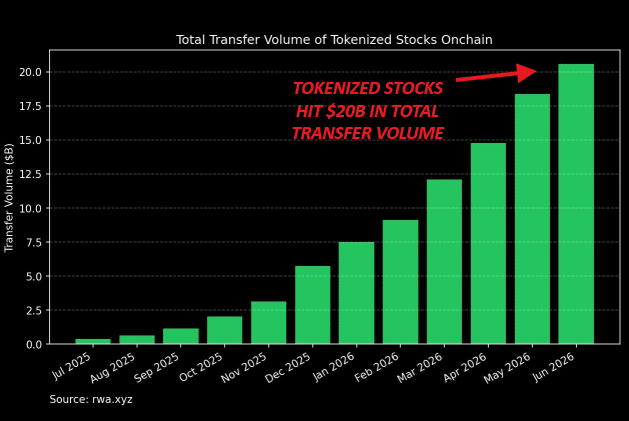

Tokenized stocks have crossed a critical threshold, cementing themselves as one of the clearest bridges between traditional finance and crypto.

According to RWA.xyz, the tokenized stock market recently surpassed $1 billion in total value for the first time. The sector has expanded by nearly 140% during the 2026 cycle alone, highlighting growing investor demand for on-chain exposure to equities.

And yet, many market participants see this as only the beginning, particularly after the launch of SpaceX’s SPCX token on Solana, setting the tone for what could be a defining trend in the years ahead.

The trade that put tokenized stocks in the spotlight

SpaceX’s SPCX launch has sparked a new wave of activity across the tokenized equity market. Still, what makes this different is not the idea itself, but the scale.

After all, SpaceX is not the first major company to have its shares tokenized on-chain. Tesla’s TSLA token is a good example. Since launching in Q3 2025, it has grown steadily and recently reached a record $62 million in tokenized value. However, SPCX appears to be operating on a different scale.

As the chart below shows, tokenized stocks have recorded $4.3 billion in on-chain trading volume over the last thirty days, pushing the cumulative transfer volume of onchain tokenized stocks above $20 billion for the first time in history.

Source: RWA.xyz

More importantly, the impact was visible almost immediately after the SpaceX IPO. On the 15th of June, tokenized stocks on Solana surpassed $100 million in 24-hour trading volume for the first time. The data clearly suggests that SPCX is not simply adding another stock to the tokenized equity market. Instead, it is helping accelerate activity “across” the sector.

With this in mind, the bigger question is whether SPCX is beginning to redefine crypto’s relationship with equities. The early data highlights that it may be doing exactly that. According to AMBCrypto, if adoption continues to accelerate, the impact of tokenized stocks could extend well beyond crypto, influencing how public equities are distributed, accessed, and traded in the years ahead.

The bull case meets valuation reality

Some analysts argue that much of the early demand for SpaceX stock may not be entirely organic.

Dan Niles, founder of Niles Investment Management, believes a significant portion of the buying could come from index funds that are required to purchase SpaceX as it is added to benchmarks such as the Russell, MSCI, and Nasdaq-100. As Niles noted:

Much of the early demand could be driven by forced buying from index funds as SpaceX is added to major benchmarks such as the Russell, MSCI, and Nasdaq-100. After the initial 15 trading days, however, I think it gets a lot more dicey.

A similar argument has been made around ETFs offering SpaceX exposure. According to Roundhill co-founder Will Hershey,

As more money flows into these funds, it becomes harder for managers to buy additional SpaceX shares because supply is limited. If ETF assets grow rapidly while managers are unable to acquire additional shares, SpaceX’s weighting within the fund can decline, reducing the benefit investors receive from any post-IPO rally.

Notably, SpaceX’s stock has struggled to hold onto its post-IPO gains. The stock is down more than 16%, with most of the decline occurring on the 22nd of June. The move lends some support to the view that early demand may have been boosted by index additions and ETF flows.

Now that those initial tailwinds are fading, investors appear to be paying closer attention to SpaceX’s valuation and longer-term growth outlook.

SPCX ignites a new phase for tokenized equities

While SpaceX’s shares faltered in traditional markets, SPCX’s on-chain demand tells a very different story.

According to RWA.xyz, the token’s total value has climbed above $26 million. For context, Tesla’s tokenized stock currently holds over $55 million in value. In other words, SPCX has already reached 50% of TSLA’s market size despite only launching recently, highlighting the pace at which capital is flowing into the asset.

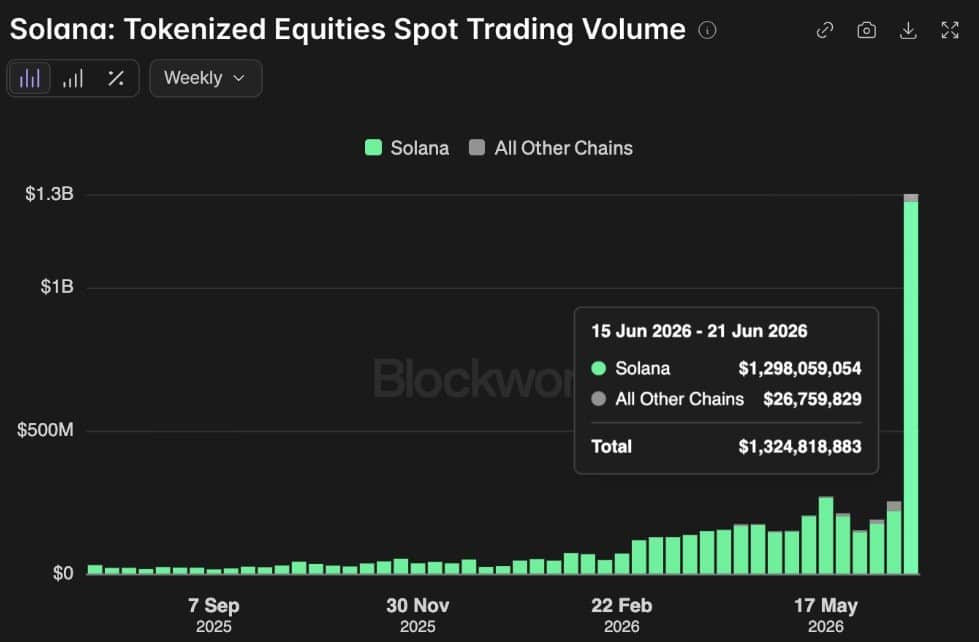

However, the key takeaway is the impact this is having on the broader tokenized equity sector. As the chart below shows, Solana recorded its biggest week ever for tokenized equities, reaching $1.29 billion in trading volume and capturing 95% of all trading activity. In essence, this reinforces the idea that SPCX’s launch didn’t just add another asset to the market. Instead, it helped accelerate activity across the space.

Source: Blockworks

Supporting this setup, Backpack has emerged as one of the main beneficiaries. Backpack is a crypto trading platform that brought fully redeemable SpaceX stock on-chain via Solana. Data shows its share of tokenized stock volume jumped from near 0% to over 50% in just five days after the SpaceX launch, highlighting how quickly liquidity has concentrated around new on-chain equity venues.

Calling this just the beginning, Backpack co-founder Armani Ferrante noted:

I think we’re probably at least two years off from this hitting, but the time to start building for this future starts now. Building resilient systems takes time.

In essence, SPCX’s launch marks more than just the arrival of another tokenized stock. While its $26 million tokenized value highlights strong investor demand, the real story is the surge in activity across the market.

Put simply, capital is no longer flowing only into SPCX. Instead, it is beginning to flow into the broader on-chain equity ecosystem. That shift suggests investors are becoming increasingly comfortable accessing stocks through crypto rails. If this trend continues, could tokenized equities eventually challenge the dominance of traditional stock market infrastructure?

Adoption is growing, but THESE challenges remain!

Despite the strong growth, tokenized equities still face several challenges.

This was highlighted when the SEC pushed back against proposals for special “innovation exemptions” for blockchain-based securities. One of the key concerns is liquidity fragmentation. According to Tiger Research’s Ryan Yoon:

Tokenized stocks can trade across multiple blockchains and platforms rather than a single exchange. As a result, liquidity becomes spread across different venues, which can lead to pricing differences and less efficient trading.

To put this into perspective, DeFiLlama data shows that more than 150 blockchains now host real-world assets, with Ethereum [ETH] leading the sector at over $14 billion in tokenized value. While this demonstrates how quickly the market is expanding, it also highlights the fragmentation challenge.

In that sense, tokenized equities still appear to be in their early growth phase. Liquidity remains fragmented, making market efficiency harder to achieve than in TradFi exchanges. However, SPCX has clearly accelerated adoption and brought greater attention to the sector, increasing the need for both regulatory clarity and more connected liquidity infrastructure as the market matures.

Moreover, SPCX’s launch is more than a headline event; it is a turning point. With Solana capturing record volumes, platforms like Backpack reshaping liquidity, and regulators grappling with fragmentation, the sector is no longer a side experiment. It is becoming a structural bridge between crypto and public markets.

If adoption continues at this pace, tokenized equities could challenge the dominance of traditional stock infrastructure and redefine how global investors access equities in the years ahead.

Final Summary

SPCX has accelerated growth across the tokenized equity market.

Regulation and liquidity remain the most difficult challenges as the sector moves toward broader adoption.

It’s a buyer’s market for U.S. housing, with 47% more sellers offering homes than buyers in April 2026, according to data from Redfin. When buyers are scarce, sellers often try to stand out by offering concessions like the 2-1 buydown, which is a temporary rate buydown that reduces mortgage payments for the first two years of a loan.

A 2-1 buydown is an attractive concession when interest rates are high but are expected to drop. Melissa Cohn, regional vice president at William Raveis Mortgage, points to a potential peace deal with Iran and falling oil prices as indications that mortgage rates may fall soon.

“It’s a good time to offer something that’s temporary, knowing that the buyer will hopefully have the opportunity to refinance at a much better rate at some point in the near future,” Cohn said.

A 2-1 buydown is an agreement to lower the payments on a home loan for the first two years. Lenders allow sellers, builders, or borrowers to pay money up front in exchange for paying less interest during the buydown period.

In the first year of a 2-1 buydown, the interest rate the borrower pays is two percentage points below the note rate, or the interest rate that’s set in the mortgage documents. In the second year, the interest rate is one percentage point below the note rate. And in the third year, the interest rate goes back to the note rate.

How does a 2-1 buydown work?

A 2-1 buydown starts with drafting a buydown agreement, which is signed by the borrower and the seller, builder, or whoever is purchasing the buydown. The purchaser deposits a sum of money, called the subsidy, into an escrow account. The lender then uses that money to cover some of the interest on the loan during the first two years.

The rate listed in the mortgage promissory note doesn’t change, and the borrower has to qualify for the loan with the full, unsubsidized payment.

To understand how a 2-1 buydown lowers payments temporarily, take a look at an example. Here are the rate and monthly principal and interest payments a borrower would pay on a 30-year mortgage with a $400,000 principal and a 6.5% note rate, according to calculations by PrimeLending.

Other buydown structures

A buydown can take other forms that lower the interest rate the borrower pays over different time periods. The following are typical buydown arrangements.

1-0 buydown. For the first year, the borrower pays an interest rate that’s one percentage point lower than the note rate. In the second year, the interest rate goes back to the note rate.

3-2-1 buydown. In the first year, the interest rate the borrower pays is reduced by three percentage points; in the second year, two percentage points; and in the third year, one percentage point. The rate goes back to the note rate in the fourth year.

Permanent buydown. The borrower pays discount points worth 1% of the loan amount, and each point lowers the interest rate by a set increment for the life of the loan.

Usually, a seller or builder pays for a 2-1 buydown. According to research from HomeLight, interest rate buydowns were among the most common seller concessions as of the third quarter of 2025. A lender can also pay for a temporary rate buydown as a promotional offer.

A borrower can pay for a 2-1 buydown, too, but it may not make sense to do so. A borrower who pays the buydown subsidy themselves would simply be paying a portion of their interest in advance. It’s more common for borrowers to purchase permanent buydowns because if you keep the loan long enough, you can eventually break even on the buydown and save money.

How much does a 2-1 buydown cost?

The up-front cost of a 2-1 buydown is the same as the interest savings over the two years of the buydown period. So, the cost depends on the loan amount and the interest rate you’re starting with. For a $400,000 30-year loan with a 6.5% interest rate, the cost is about $9,100. Sellers may cover the cost of this buydown in place of a price reduction.

When does a 2-1 buydown make sense?

A 2-1 buydown may make sense if you’re expecting interest rates to drop within a couple of years. In that case, you can enjoy lower payments during the buydown period and then refinance before you have to pay the full interest rate.

A temporary buydown can also be helpful if you’re growing your income and want a reprieve from higher payments for a year or two. For example, maybe you’re starting a business and expect to earn more income as you grow your customer base. Likewise, you might consider a temporary buydown if you have higher short-term expenses, such as increased childcare costs for a year or two until a child is old enough for school. You can devote more of your budget to childcare during the buydown timeframe, then make higher payments on the mortgage going forward.

Temporary buydowns tend to make sense when the seller, builder, or another party pays for them. If you’re buying down the rate yourself, paying interest upfront for a temporary buydown generally isn’t worth it because there’s no savings over time.

A 2-1 buydown isn’t a good idea if you won’t be able to afford the full payment in the third year and beyond, so plan out the effect on your budget and make sure you can actually absorb the higher costs later. Keep in mind that some living expenses, like childcare, tuition, and out-of-pocket healthcare spending, aren’t included in your debt-to-income ratio and therefore don’t factor into lenders’ decisions to qualify you for a loan.

2-1 buydown vs. permanent buydown — which is better?

A 2-1 buydown or another temporary buydown can be a good choice when the seller is paying for it, and you need a temporary break from higher mortgage payments, such as when your expenses are momentarily high, or your income is going to rise soon. It’s also the better choice when you plan to refinance within a couple of years.

A permanent buydown is often the better option if you plan to hold on to the mortgage long-term. You can save money over time, and it can be easier to qualify for the loan because you get to qualify at the reduced rate. But paying the up-front cost is worth it only if you’re not going to move or refinance in the near future.

“A permanent buydown, I think, only makes sense when you believe that we’re at the bottom of a rate cycle and that’s a rate that you’re going to keep for a long time. Knowing that you’re likely to be refinancing in the next year or two, I think it’s just throwing money out the door,” Cohn said.

And if you’re paying for a buydown yourself, consider whether you’d be better off making a larger down payment instead.

Temporary vs. permanent rate buydown FAQ

Is a 2-1 buydown worth it?

Whether a 2-1 buydown is worth it depends on who’s paying for it and how you expect your financial situation to change in the next two years. A temporary buydown is more likely to be advantageous if the seller or builder is covering the cost. If you plan to refinance soon or if you’ll have higher income or lower expenses in two years, agreeing to a buydown offer might make sense.

Can a seller pay for a 2-1 buydown?

A seller can pay for a 2-1 buydown, as can a builder, lender, or other interested party to the sale of the home. It’s common for sellers to fund temporary buydowns as a concession to attract buyers.

What happens to the buydown funds if I refinance early?

If you refinance before the buydown timeframe is over, the unused funds remaining in the escrow account typically go toward paying off the loan principal. However, some buydown agreements state that the funds are released to the borrower or the lender in this situation.

Bitcoin dropped to $59,175 overnight, its lowest point since early June, before recovering to about $61,500 by Thursday morning, per CoinDesk data. Nearly $1 billion worth of futures positions were liquidated across crypto majors, such as bitcoin, ether, solana, and others, to tokenized versions of stocks, such as Micron Technology Inc (MU) and Sandisk (SNDK).

The dip triggered roughly $430 million in long liquidations on bitcoin-tracked futures, or bets on higher prices that were automatically closed as the price fell.

No single catalyst drove the move. Bitcoin has lost about 10% since Monday’s peak near $65,500, pulled lower by the same forces that have dominated all week: a hawkish Fed, six straight weeks of ETF outflows, thinning summer liquidity, and a quarter-end options expiry on June 30 that traders say is keeping the market unstable.

Major market-maker Wintermute had flagged $59,000 as the bear-market low to watch in its Tuesday’s note.

The bounce came from outside crypto. Micron Technology reported quarterly earnings after the close that shattered analyst estimates, sending its shares sharply higher and lifting the broader memory chip complex.

SK Hynix separately disclosed plans for a U.S. stock listing seeking roughly $29 billion, one of the largest offerings ever. Samsung and Kioxia rallied in Asia Thursday morning.

The same AI chip trade that sent the Kospi down 10% on Monday on fears the spending boom was stalling is now the thing steadying crypto, with Micron’s results reading as confirmation that demand for AI memory is structural, not speculative.

The quarter-end remains the week’s live risk. Bitcoin’s $59,000 low held, but $1.6 billion in leveraged long positions sit clustered below $58,000, per CoinGlass, meaning a break there would accelerate the drop.

Thursday’s PCE inflation print, the Fed’s preferred price gauge, is the next data point that could move the market in either direction.

Holding money bunched in fist by Iana Miroshnichenko via iStock

The dollar index (DXY00) climbed to a 13-month high on Tuesday and finished up by +0.36%. The dollar rallied on Tuesday’s plunge in equity markets, boosting liquidity demand for the currency. The dollar also has carryover support from last Wednesday, when the FOMC projected higher interest rates later this year. Tuesday’s US economic news was mixed for the dollar as the Jun S&P manufacturing PMI unexpectedly increased, but the Jun Richmond Fed manufacturing survey of current conditions fell more than expected.

The US Jun S&P manufacturing PMI unexpectedly rose +0.6 to 55.7, stronger than expectations of a decline to 54.6 and the strongest pace of expansion in 4 years.

More News from Barchart

The US Jun Richmond Fed manufacturing survey of current conditions fell -9 to 4, weaker than the 8 expected.

The swaps markets are discounting the odds at 36% for a +25 bp rate cut hike at the next FOMC meeting on July 28-29.

EUR/USD (^EURUSD) tumbled to a 1-year low on Tuesday and finished down by -0.42%. The euro extended Monday’s losses on Tuesday amid negative carryover from dovish comments by ECB President Lagarde, which reduced the chances of additional ECB rate hikes, as she said she sees no need for a more forceful ECB response to the US-Iran war. Tuesday’s Eurozone PMI reports were mixed for the euro: the manufacturing PMI was weaker than expected, while the composite PMI was stronger than expected. Losses in the euro were limited after hawkish comments from ECB Chief Economist Philip Lane, who said that ECB Officials face the risk that inflation will hover above their goal “for quite some time.”

The Eurozone Jun S&P manufacturing PMI fell -0.3 to 51.3, weaker than expectations of no change at 51.6. However, the Jun S&P composite PMI rose +1.0 to 49.5, stronger than expectations of 49.2.

Eurozone May new car registrations rose +3.2% y/y to 955,000 units, the fourth consecutive monthly increase.

ECB Chief Economist Philip Lane said ECB Officials face the risk that inflation will hover above their goal “for quite some time.”

The markets are discounting a +10% chance for a +25 bp rate hike by the ECB at its next policy meeting on July 23.

USD/JPY (^USDJPY) on Tuesday fell by -0.01%. The yen rose slightly on Tuesday amid signs of strength in Japan’s economy, following the June S&P manufacturing and services PMIs, which expanded. Lower T-note yields on Tuesday were also supportive of the yen.

Gains in the yen are limited amid concerns that the BOJ is falling behind the curve in normalizing monetary policy. Last week, BOJ Deputy Governor Uchida said that the BOJ will assess the impact of rate hikes on the economy, signaling it will move at a glacial pace on policy tightening.

The risk of intervention in currency markets to support the yen is rising after Japanese Finance Minister Satsuki Katayama said she spoke with US Treasury Secretary Scott Bessent on Tuesday, and they agreed to take “bold” steps on currencies if needed, and that the nations are increasingly “aligned” on foreign-exchange policy. With the yen firmly above 160 per dollar, intervention risks have increased, as Japanese authorities have intervened in the forex market several times in the past when the yen reached that level.

The Japan Jun S&P manufacturing PMI rose +0.4 to 54.9. The Jun S&P services PMI rose +1.8 to 51.8.

The markets are discounting a +3% chance of a +25 bp BOJ rate hike at the next policy meeting on July 31.

August COMEX gold (GCQ26) on Tuesday closed down -53.30 (-1.27%), and July COMEX silver (SIN26) closed down -3.513 (-5.36%).

Gold and silver prices sold off sharply on Tuesday, with gold falling to a 1.5-week low and silver sliding to a 3-month low. Tuesday’s rally in the dollar index to a 13-month high is bearish for metals. Also, Tuesday’s sharp selloff in equity markets fueled the liquidation of long precious metals holdings as investors sought funds to cover margin calls. In addition, hawkish comments on Tuesday from ECB Chief Economist Philip Lane weighed on precious metals when he said ECB Officials face the risk that inflation will hover above their goal “for quite some time.”

Precious metals found some support from Tuesday’s plunge in equity markets, which has boosted safe-haven demand for the metals. Also, Tuesday’s decline in WTI crude oil prices to a 3.5-month low has eased inflation expectations and could prompt global central banks to ease monetary policy, a bullish factor for precious metals. In addition, precious metals have safe-haven demand amid political uncertainty in the UK following Keir Starmer’s announcement on Monday that he would step down as Britain’s prime minister.

Recent fund liquidation of precious metals is bearish for prices, as long holdings in gold ETFs fell to a 7.5-month low last Wednesday, after reaching a 3.5-year high on February 27. Also, long holdings in silver ETFs fell to an 11-month low last Friday from the 3.5-year high posted on December 23.

Strong central bank demand for gold is supportive of gold prices, following news that bullion held in China’s PBOC reserves rose by +320,000 ounces to 74.96 million troy ounces in May, the largest monthly increase in 17 months, and the nineteenth consecutive month the PBOC boosted its gold reserves.

On the date of publication, Rich Asplund did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

DeFi is having a difficult year, with a marked rise in hacks and security breaches. As more protocols get exploited, investor confidence is taking a hit.

This loss of trust could be one reason why capital is moving out of DeFi.

DeFi TVL falls 39% in 2026

DeFi’s capital base has been falling throughout 2026. According to data from CryptoRank, total DeFi TVL has fallen every month this year. In fact, the number has dropped from around $115 billion in January to nearly $70 billion in June.

YTD decline was at about 39% too so, it’s not been a short-term dip.

Source: X

This comes after a big phase in late 2025, when DeFi TVL was above $150 billion. Since then though, the market has calmed down and capital has moved out of riskier projects.

Ethereum [ETH] still has the largest share, but even its dominance has not been enough to stop the overall decline. Most major chains have seen pressure this year, with TRON [TRX] and Hyperliquid [HYPE] being rare exceptions with 5% and 7% growth, respectively.

Hacks affecting trust in DeFi?

Alarm bells get louder when you consider this alongside the rise in security breaches. According to CryptoRank, Q2 2026 recorded 85 hacks, making it the busiest quarter for crypto exploits by incident count.

While losses have not crossed past dollar-value peaks, the frequency of attacks is enough to make users sleep with one eye open.

Source: X

The capital outflow can also be chalked down to a confidence problem. When users see repeated exploits across protocols, they are less likely to keep funds locked on-chain.

AMBCrypto previously reported that DeFi’s TVL has already fallen from nearly $178 billion to around $72.5 billion. Stablecoin supply stayed close to $315 billion too.

While liquidity has not disappeared from crypto, investors are more selective about where they put their money.

With 2026 already seeing 121 hacks and nearly $1 billion in losses, security is now a major pressure point for DeFi. Until protocols prove they can protect capital better, TVL recovery will most certainly remain uneven.

Final Summary

DeFi TVL has dropped by 39% YTD to nearly $70 billion.