Bitcoin’s BTC$66,465.91 drop below $60,000 earlier this month spurred investors to pile into the largest cryptocurrency, with almost 260,000 BTC bought over 10 days and one measure of demand increasing to its highest possible level.

Investors have bought a net 259,298 BTC since June 5, paying between $59,000 and $67,000, according to Glassnode UTXO Realized Price Distribution data. Glassnode’s Accumulation Trend Score by Wallet Cohort, which measures the relative strength of purchasing fervor based on both the size of buyers and the amount acquired over the previous 15 days, stands at 1.0, the top reading.

Buying has been broad-based across wallet cohorts, ranging from holders with less than 1 BTC, typically retail investors, to those with as many as 1,000 BTC. Notably, from March through May, most groups were net distributors, or sellers, as bitcoin stagnated around $70,000.

The aggregate Accumulation Trend Score has now remained at a peak level for more than two weeks, indicating aggressive buying across cohorts and marking the strongest accumulation behavior observed during the current drawdown.

Zcash [ZEC] has shown relative upside strength over the past three days, closing at higher highs. The altcoin breached the $500 resistance and touched a local high of $545 before slightly retracing.

As of this writing, Zcash traded at $525, up 5.94% on the daily charts, signaling dominant upside volatility. With Zcash trading above $500, short-position holders are incurring massive losses.

Zcash whale takes a $3.8 million loss

As the market’s upside momentum continued, bears were forcefully flushed out, while others closed positions to avoid further losses. According to Onchain Lens, a wallet linked to karna0x fully closed its $9.8 million ZEC short position.

In the process, the whale incurred a loss of over $3.8 million. The decision to close indicated the whale saw the risk of liquidation as the market continued to pump.

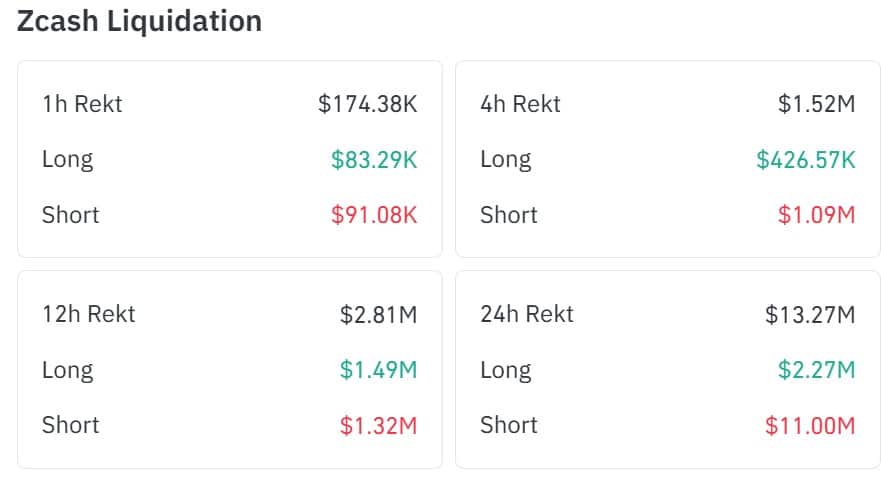

In fact, Zcash short-position holders have seen massive liquidations. CoinGlass data showed that over $11 million in short positions were liquidated, while only $2.2 million in longs were liquidated.

Source: CoinGlass

Historically, a short squeeze has always inspired an uptrend. As traders continue to fund their positions to avoid liquidations, demand for the asset recovers. As a result, momentum strengthens, further flashing out more bears and leading to a strong market reaction.

Ideally, the prevailing market conditions position Zcash towards such an outcome.

On top of that, threatened by rising short liquidations, other traders flipped to longs. In fact, the altcoin’s Long/Short Ratio jumped to 1.095 at press time.

Source: Coinglass

The ratio’s reclamation of 1 suggests that most traders turned bullish and have been anticipated more gains.

Can ZEC bulls hold on?

Zcash has recovered significantly since crashing from $630 to $251. Amid this market recovery, upside momentum has strengthened significantly, with bulls retaking control.

As a result, the altcoin’s upside momentum has strengthened significantly, as evidenced by the DMI and ADX smoothing indicators.

ZEC is currently experiencing a modest bullish bias with a developing trend. Currently, bulls have a slight edge as +DI sits above -DI while ADXR sits above ADX.

Source: TradingView

Although the gap is narrow, it shows a strengthening trend in its continuation potential. Thus, if the conditions persist, Zcash could flip $550 and target $600 resistance.

However, sellers remain active, as -DI sits at 24 and +DI at 25, suggesting a narrow gap. If profit-taking increases at current levels, ZEC could fall below $500 again.

Final Summary

A wallet linked to karna0x fully closed its $9.8 million ZEC short position, taking a $3.8 million loss.

Zcash is exhibiting strong upside momentum, with bears retaking the market as they eye a move towards $600.

Magnera has reached an agreement to transfer its operations in Caerphilly, Wales, to Polyart Group, which is held by Prudentia Capital.

Financial terms of the deal remain undisclosed.

The move follows a review by Magnera of its production technologies, product range and the markets it supplies.

As part of that work, the company assessed options for the Caerphilly business, which makes metallised paper used in areas such as premium labelling, gift wrap and food packaging.

Magnera said the assessment led to a formal sale process and an arrangement under which Polyart will acquire all shares in the Caerphilly business.

Magnera CEO Curt Begle said: “We are deeply grateful for the dedication and commitment of our Caerphilly team, and we wish them continued success as they join Polyart.

“We also value the loyalty of our customers and remain fully committed to supporting a seamless transition, ensuring exceptional service and continued success for all stakeholders.”

Polyart is a specialist manufacturer of coatings and films. The group was created in 2020 through the combination of Arjobex, MDV, Tech Folien and Reisewitz.

It produces paper and film materials for speciality labels, including industrial, decorative and security uses, as well as applications in digital printing and display.

Polyart also undertakes custom coating work. The company is based in Boulogne-Billancourt, France, and is owned by Prudentia Capital.

Prudentia Capital founding partner Dominik Zwerger commented: “Prudentia Capital is pleased to add the Caerphilly operations to our growing portfolio of companies. We’re excited about the additional value we can bring to our existing customers and about growing the business, which serves customers globally.

“Our vision is to leverage the expertise of the management team to continue providing high-quality products.”

Magnera said it supplies more than 1,000 customers globally with materials used in absorbent hygiene products, protective clothing, wipes and food and beverage-related items.

It operates 44 production sites worldwide and has 8,000 employees.

“Magnera to divest Caerphilly-based metallised paper unit to Polyart” was originally created and published by Packaging Gateway, a GlobalData owned brand.

US spot bitcoin ETFs lost a net $64 million on Monday, even as spot ETFs for ether, XRP, Solana and Hyperliquid all pulled in fresh cash. On the surface, that looks like a clean rotation out of bitcoin and into everything else.

Ether funds gained $22.5 million, Hyperliquid funds $17.2 million, and the XRP and Solana funds about $2.8 million each. That tracks Monday’s price action, where the alts ran well ahead of bitcoin, with XRP up about 7%, Solana 6% and Hyperliquid 11% on the day. The flows followed the tape.

[@portabletext/react] Unknown block type “image”, specify a component for it in the `components.types` prop

It is worth keeping the scale in mind. Bitcoin ETFs still hold about $83 billion in assets, against roughly $10 billion for ether and around $1 billion each for the XRP, Solana and Hyperliquid products.

The bitcoin number needs a second look. The outflow was not broad, as BlackRock’s IBIT, the largest fund, actually took in $66 million. The net loss came almost entirely from Grayscale’s GBTC, the high-fee legacy trust that has been shedding assets since these funds launched, which lost $124 million on the day. Strip out GBTC and bitcoin ETFs had an ordinary session

[@portabletext/react] Unknown block type “image”, specify a component for it in the `components.types` prop

The real question is durability. If the altcoin ETFs keep drawing inflows once GBTC’s drag fades, the rotation is real. If not, Monday was a blip dressed up as a trend.

Silver (SI=F) July futures opened at $68.90 per ounce on Monday, 1.4% higher than Friday’s closing price of $67.97. The price of silver continued to move higher in early trading to $70.75 by 7:16 a.m. ET.

Like gold, silver prices are up this morning following the announcement of a ceasefire deal between the U.S. and Iran, setting the stage for a formally signed agreement that could be reached as soon as this week.

This most significant step toward long-term peace in the Middle East has prompted oil prices (BZ=F) to fall and inflation concerns to ebb at least somewhat. With the Fed almost certainly keeping rates unchanged this week, the prospects for higher precious metal prices improved a great deal.

The opening price of silver futures on Monday was up 1.4% compared to Friday’s close. Here’s how the opening silver price has changed versus last week, month, and year:

One week ago: +2.1%

One month ago: -14.5%

One year ago: +90.3%

For context, silver’s year-over-year growth was 173.3% on May 14.

Want to learn more about the current top-performing companies in the silver industry? Explore a list of the top-performing companies in the silver industry using the Yahoo Finance Screener. You can create your own screeners with over 150 different screening criteria.

How beginners can invest in silver

There are several ways to invest in silver, from buying the metal itself to choosing financial products tied to its price. Here’s how each option works.

Physical silver

The most direct way to invest in silver is to buy it in physical form, either as bullion bars or government-minted coins. This gives you direct ownership of the metal, with no counterparty risk from an exchange or financial institution.

The trade-off is logistics. You’ll need to think about storage, security, and potentially insurance. Dealers also charge a markup above the spot price, which means prices need to rise enough to cover that premium before you’re in profit. Still, for investors who want tangible ownership of their assets, physical silver is a straightforward option.

Silver ETFs

Silver exchange-traded funds (ETFs) trade on stock exchanges the same way individual stocks do. Some ETFs hold physical silver directly, giving shareholders fractional ownership of real metal. Others invest in silver mining companies rather than the commodity itself.

ETFs are generally the most accessible and liquid way to get silver exposure. You can buy and sell them through any standard brokerage account, and there’s no storage or insurance to worry about.

Keep in mind, though, that some silver funds are taxed as collectibles rather than investments, which can mean a higher tax rate. It’s worth confirming the tax treatment with a professional before investing. You’ll also have to keep an eye on expense ratios.

Whether you’re tracking the price of silver since last month or last year, the price-of-silver chart below shows the precious metal’s value journey so far this year.

Are “yields” becoming a defining driver of the 2026 cycle?

At a structural level, the CLARITY Act is under scrutiny partly because it introduces the concept of yield-bearing stablecoins. If stablecoins begin to generate yield, capital could flow into DeFi-native rails, raising competitive pressure on traditional finance and contributing to the ongoing regulatory hesitation.

Source: X

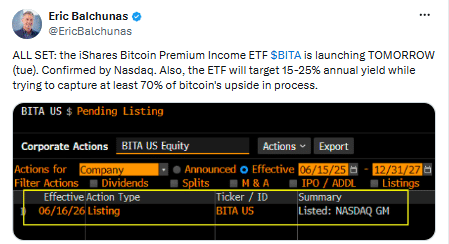

In parallel, yield is being absorbed into institutional crypto products. BlackRock’s iShares Bitcoin Premium Income ETF (BITA), set to launch on Tuesday, the 16th of June, reflects this shift as it monetizes volatility via options on IBIT.

Put simply, instead of pure spot Bitcoin exposure, BITA generates yield by selling options on iShares Bitcoin Trust for steady income. It targets a 15-25% yield while still aiming to capture 70% of BTC’s upside.

Basically, the fee it collects from selling those options becomes the income paid out to investors.

In terms of flow, if demand for BITA grows, it buys more IBIT shares, which can lead IBIT to hold more Bitcoin to back them. So the BTC doesn’t go to BlackRock.

Instead, it stays inside IBIT, but demand for BITA can indirectly increase Bitcoin held in the ETF system.

In essence, the shift signals something bigger: Crypto exposure is moving away from pure directional bets toward structured income products built on top of Bitcoin [BTC] volatility. So, instead of “just holding BTC,” issuers are offering investors ways to actively monetize it.

But looking at recent ETF sentiment, this move is clearly more strategic than random.

Bitcoin ETFs enter a new phase as yield becomes the core narrative

Looking at ETF flows, it’s clear investors are moving away from pure speculation toward more stability.

Yield is becoming the bridge in this shift.

Unlike traditional ETFs that provide direct Bitcoin exposure, BlackRock’s BITA targets stability by generating income from Bitcoin volatility instead of just tracking price. While this looks like a structural upgrade, it also reflects rising FUD around both BTC and its ETF ecosystem.

From a technical standpoint, BTC has pulled back over 25% this year. That move has weighed on iShares Bitcoin Trust, with shares dropping from around $50 to roughly $37 at press time.

That weakness has also shown up in sentiment, with Bitcoin ETFs seeing about $2.5 billion in net outflows in Q2, which has in turn added pressure on Bitcoin itself, creating a feedback loop where price weakness triggers outflows, and outflows reinforce further downside.

Source: SoSoValue

Against this backdrop, BlackRock’s launch of an income-based Bitcoin ETF is clearly a strategic move.

The logic is simple: By linking returns to options on iShares Bitcoin Trust, the structure shifts Bitcoin exposure away from pure price speculation and toward yield generation, where volatility itself becomes the source of income rather than just risk.

Therefore, this could mark a key inflection point for the entire ETF ecosystem, as Bitcoin transitions from a directional asset into a volatility-backed income engine.

Final Summary

BITA makes yield by selling options on iShares Bitcoin Trust, giving up some upside in return for income.

If more people buy BITA, it buys more IBIT, which can lead to more BTC being held inside the ETF system.

Bybit, one of the world’s top cryptocurrency exchanges by trading volume, has launched options trading on Tether Gold (XAUT), a token that provides you ownership of real physical gold.

The XAUT options are now live and allow traders to hedge risk, speculate on gold price movements, trade volatility, and build custom strategies through Bybit’s Request for Quote (RFQ) system for over-the-counter (OTC) deals.

Bybit partnered with Orbit Markets, a leading crypto options market maker, to ensure deep liquidity from the start. Orbit’s team brings significant expertise, including former senior executives from precious metals trading desks, notably the ex-APAC Head of Currencies and Precious Metals at Deutsche Bank.

“As tokenization accelerates, we believe the distinction between crypto and TradFi will continue to narrow,” said Jimmy Yang, co-founder of Orbit Markets. “Gold options are a cornerstone of traditional derivatives markets, and we are excited to see growing interest in TradFi derivatives within crypto.”

The XAUT options are European-style contracts settled in dollar-pegged stablecoin USDT, with each options contract corresponding to one XAUT token, which itself represents one troy ounce of physical gold.

What Are Options?

Options are derivative contracts that give the buyer the right, but not the obligation, to buy or sell the underlying asset at a set price before or on a specific date. A call option gives the right to buy, while a put option gives the right to sell.