On May 26, Piper Sandler lowered its price recommendation on Corebridge Financial, Inc. (NYSE:CRBG) to $31 from $35. It reiterated an Overweight rating on the shares. The firm said the change reflects recent stock performance and the passage of time. Piper noted that it has generally increased price targets for most insurance carriers while lowering targets for some insurance brokers. Its analysis takes a bottom-up approach. Following first-quarter results, the firm believes investors may be better served focusing on insurance carriers rather than brokers. According to Piper, underwriting performance provided stronger-than-expected support for carriers, while brokers delivered weaker organic growth results.

On May 13, BofA raised its price goal on CRBG to $41 from $40 and maintained a Buy rating on the stock. The analyst said that neither Corebridge nor Equitable (EQH) is currently included in the S&P indices. If a combination between the two companies were to occur and the merged company gained entry into the index, it could generate substantial demand for the shares. The analyst added that such demand could potentially exceed the impact of a share repurchase program.

Corebridge Financial, Inc. (NYSE:CRBG) provides retirement solutions and insurance products across the United States. The company works with financial professionals and institutions to help individuals plan, save, and build more secure financial futures.

While we acknowledge the potential of CRBG as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you’re looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on thebest short-term AI stock.

Prime Video has announced its first set of talent appearing at their inaugural Obsessed Fest – an immersive, all-day fan experience bringing audiences face-to-face with the creators and stars of the most popular YA shows, including Off Campus, Elle, The Love Hypothesis, The Devil’s Mouth, and more. The event celebrates the streaming platform’s expansive new initiative, Obsession Is In Session, which celebrates young adult storytelling, fandoms, and the communities that keep it going.

Taking place on Saturday, June 27 at nya Studios in Los Angeles, Prime Video transforms the fandom into an all-day celebration with exclusives, surprise moments, and access to your favorites, including Lili Reinhart and Tom Bateman from The Love Hypothesis; Benito Skinner, Wally Baram, and Mary Beth Barone from Overcompensating; Belmont Cameli, Stephen Kalyn, Jalen Thomas Brooks, Antonio Cipriano, Ella Bright, Mika Abdalla, Josh Heuston and creator/EP Louisa Levy from Off Campus; Matt Cornett, Michael Bradway, author Carley Fortune and showrunner/EP Amy B. Harris from Every Year After; Lexi Minetree from Elle; Gavin Casalegno, Lana Condor, and Tommi Rose from The Devil’s Mouth; Asha Banks and author Mercedes Ron from Your Fault: London; Ester Expósito from Drawn Together; Damian Hardung from Maxton Hall; Maia Reficco, Fernando Lindez, and author/producer Anna Todd from The Last Sunrise; and author Casey McQuiston from Red, White & Royal Wedding. More guests may be announced.

Prime Video’s Obsessed Fest

Prime Video

There will be tons of programs for fans to enjoy, including the main stage, which will have talent-led panels with exclusive footage and interactive fan moments. There’s a special book club designed for deep dives with your favorite YA authors, as well as signings, conversations, and workshops. Please remember to bring your own book!

For content creators, or budding ones, there will be a suite of cinematic content studios where fans can recreate scenes from popular titles and capture personalized photos and videos. There will also be a dedicated screening room to exclusive merchandise, food and drinks for purchase from LA’s food trucks, and a communal fan space to chat about what you’re obsessed with.

Amazon Music, the official audio sponsor for the event, will have its Amazon Music Lounge for fans to discover all the music from the Obsessed Fest shows, and “dive deeper into their favorite stories through exclusive programming.” There will also be a day-long DJ set to keep fans entertained.

For more information on Prime Video’s Obsessed Fest or to get tickets, click here.

The two biggest DeFi exploits of the past two months have one thing in common. They used a tool that does not exist on the XRP Ledger.

Thorchain lost roughly $10.8 million on May 15 to a cross-chain attack that drained funds across Bitcoin, Ethereum, BSC, and Base. Drift Protocol, a Solana-based decentralized perpetual exchange, and KelpDAO, a liquid restaking protocol on Ethereum, together accounted for more than $600 million in losses through April alone.

Cross-chain bridges have lost over $2.8 billion to attacks since 2021, per Chainalysis. And a significant share of these exploits used some variant of the same mechanic: flash loans.

A flash loan is a smart contract feature that lets a trader borrow millions of dollars with no collateral, on the condition that the loan is repaid inside the same transaction. The legitimate use cases include arbitrage between exchanges, collateral swaps without unwinding positions, and liquidation bots that maintain solvency in lending markets.

The attack pattern is the same mechanic pointed in the wrong direction.

A borrower takes out the loan, uses the funds to manipulate an oracle or drain a poorly designed pool, profits from the manipulation, and repays the loan, all before the transaction settles. If any step fails, the whole sequence rolls back, so the attacker risks nothing but gas fees.

The XRP Ledger does not let this work. A draft amendment filed on the XRPL standards repository earlier this week, proposing concentrated liquidity and StableSwap-style pools for the chain’s native automated market maker, included a single line in its Security Considerations section: “Flash loan attacks are structurally impossible. XRPL transactions are atomic without composable intra-transaction calls.”

What that means is that XRPL transactions either fully succeed or fully fail, like an Ethereum transaction. But unlike Ethereum, an XRPL transaction cannot call into another contract during its execution. The borrow-manipulate-repay sequence that defines a flash loan attack needs at least three nested operations inside a single transaction envelope.

That is a meaningful architectural choice, and it has a cost. Flash loans are not only an attack tool. They have become a structural component of Ethereum DeFi, with Aave, dYdX, and other major protocols offering them as a product. Arbitrage traders use flash loans to clear price differences between exchanges in a single atomic action.

Liquidation bots use them to keep over-collateralized lending positions solvent. Sophisticated DeFi users use them for collateral swaps that would otherwise require capital that gets tied up for hours. XRPL gives up all of that in exchange for closing the attack class entirely.

For most of XRPL’s history, the tradeoff did not matter because the chain’s DeFi footprint was small. That is changing. Tokenized real-world assets on the XRP Ledger have crossed $3 billion in total value, including the Ripple-JPMorgan-Mastercard-Ondo Finance pilot last month that processed a tokenized U.S. Treasury redemption in under five seconds.

The draft AMM amendment, if it passes, would close the capital-efficiency gap that has held XRPL DeFi behind Ethereum, opening the chain to a wider set of trading and yield strategies.

If the AMM amendment passes and XRPL’s DeFi liquidity grows toward something institutional capital can deploy at scale, the question becomes whether structural exploit resistance is a real competitive advantage or just a feature that institutions ignore in favor of where the liquidity already is.

Nvidia has been one of the most traded stocks in the world, and the leveraged ETFs that track it have become some of the most active names in daily ETF flows. NVDL, the GraniteShares 2x Long NVDA Daily ETF, is at the center of this trade — and it deserves a clear-eyed explanation before you buy in.

What Is NVDL?

NVDL is a single-stock leveraged ETF that seeks to deliver 2x the daily return of Nvidia (NVDA). If Nvidia goes up 3% in a day, NVDL aims to rise roughly 6%. If Nvidia falls 3%, NVDL falls roughly 6%.

It does this using total return swaps — derivative contracts with a counterparty that provide leveraged exposure without the fund actually owning 2x the Nvidia shares. The fund is managed by GraniteShares and trades under the ticker NVDL on the Nasdaq.

NVDL vs NVDU: Two Leveraged Nvidia ETFs

There are two main competitors in the leveraged Nvidia space:

Feature

NVDL

NVDU

Issuer

GraniteShares

Direxion

Leverage

2x daily

2x daily

Full Name

GraniteShares 2x Long NVDA Daily ETF

Direxion Daily NVDA Bull 2X Shares

Expense Ratio

1.05%

0.92%

AUM

Larger (more established)

Smaller

Options Activity

Higher volume

Lower volume

Both ETFs do the same thing and track each other closely day-to-day. NVDL has been around longer and has more trading volume, making it the more liquid choice. NVDU has a slight cost advantage on paper. For most investors, NVDL is the default due to liquidity.

How 2x Leverage Actually Works

The key word in NVDL’s name is daily. The fund resets its leverage each trading day, which has an important consequence: the leverage compounds daily, not over the long term.

Here’s a simple example of why this matters:

Day

Nvidia Return

NVDA Price

NVDL Return

NVDL Price

Start

—

$100.00

—

$100.00

Day 1

+10%

$110.00

+20%

$120.00

Day 2

-10%

$99.00

-20%

$96.00

After two days, Nvidia is down 1% ($100 → $99). But NVDL is down 4% ($100 → $96). The asymmetry gets worse the more volatile the underlying stock is. This effect is called volatility decay (or “beta decay”) and it’s the primary reason leveraged ETFs underperform over time, even when the underlying stock ends up in the same place.

Volatility Decay: The Hidden Cost of Leverage

Volatility decay isn’t a fee or a mistake — it’s a mathematical reality of daily-rebalancing leverage. The more a stock swings up and down without trending, the more value a 2x ETF bleeds.

For Nvidia specifically, this is a big deal. NVDA regularly moves 3–8% in a single session around earnings, analyst calls, or macro events. That kind of volatility accelerates decay dramatically.

In a strong, sustained uptrend — like Nvidia’s 2023 AI-driven surge — NVDL can dramatically outperform. In a choppy, sideways market, it loses money even if the underlying stock is flat. In a sharp drawdown, the losses compound faster than most investors expect.

The Real Performance Numbers

When Nvidia is on a tear, NVDL looks extraordinary. When Nvidia corrects or consolidates, NVDL’s losses can be brutal and don’t automatically recover when NVDA bounces back to its prior high — because the leveraged fund needs a bigger recovery percentage than the stock itself to get back to even.

For example: if NVDL falls 50%, it needs a 100% gain just to break even. If Nvidia itself fell 25% (causing NVDL to drop ~50%), Nvidia only needs a ~33% recovery to get back to its high — but NVDL needs twice that, in perfectly trending conditions, with no additional volatility drag.

Who NVDL Is For

NVDL is a legitimate trading tool — but it’s built for specific use cases, and most retail investors aren’t in those use cases.

NVDL makes sense if you are:

A short-term trader holding for hours to days, not weeks or months

Using it as a hedge against a short position in Nvidia

An options trader using it as a liquid underlying for expressing near-term directional views

Comfortable monitoring and sizing the position carefully as part of a broader active trading strategy

NVDL does not make sense if you are:

A long-term investor who wants Nvidia exposure in a buy-and-hold portfolio

Dollar-cost averaging into a position over months

Investing money you can’t afford to lose a significant percentage of quickly

Trying to “catch up” after missing Nvidia’s run — the math punishes late entries in volatile markets

NVDL vs Buying Nvidia Directly

For most investors, this comparison isn’t close: buying Nvidia stock directly is almost always the better long-term choice.

Here’s why:

No volatility decay. NVDA stock doesn’t have the daily-reset problem. It compounds normally over time.

No expense ratio drag. NVDL charges 1.05%/year; NVDA costs nothing to hold (beyond trading commissions).

No counterparty risk. NVDL’s returns depend on swap contracts with financial counterparties. NVDA is direct ownership of the company.

Cleaner tax treatment. Leveraged ETFs can generate more short-term capital gains due to daily rebalancing activity inside the fund.

If your conviction is “I want to own Nvidia for the long run,” owning more Nvidia shares is cleaner, cheaper, and more reliable than owning NVDL.

The case for NVDL over direct NVDA is essentially: you want amplified short-term gains and you’re actively managing the position. That’s a trading argument, not an investing one.

Position Sizing and Risk Management

If you do trade NVDL, position sizing is critical. Because of leverage decay, large allocations can devastate a portfolio during a Nvidia downturn. Most experienced traders who use leveraged single-stock ETFs keep them to a small percentage of total portfolio value — often under 5% — and treat them as a tactical trade with a defined exit, not a core holding.

A stop-loss order and a clear thesis (“I’m holding this through earnings, then exiting”) are essential. “I’ll hold until it recovers” is not a strategy for a daily-reset leveraged product — it can take far longer and require far higher prices to recover than intuition suggests.

The Bottom Line

NVDL is one of the most actively traded ETFs in the market right now for a reason — Nvidia’s AI dominance has made it the most watched stock in the world, and leveraged versions amplify every move. But amplification cuts both ways, and the daily-reset mechanism means NVDL is a wasting asset in anything other than a straight-line uptrend.

For traders with a defined short-term view on Nvidia: NVDL or NVDU are useful tools. For long-term investors who simply want Nvidia exposure: own the stock directly. The fees, the decay, and the complexity of leveraged ETFs work against you over any horizon longer than a few days.

This article was generated with the assistance of artificial intelligence and reviewed by ETF.com staff.

Investment Risk Disclosure The information provided on this website is for informational and educational purposes only and does not constitute investment advice, financial advice, trading advice, or any other sort of advice. Nothing on this site should be construed as a recommendation to buy, sell, or hold any security or financial product. General Investment Risks Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. The value of investments may fluctuate, and investors may receive back less than they originally invested. There is no guarantee that any investment strategy will achieve its objectives. ETF-Specific Risks Exchange-traded funds (ETFs) are subject to risks similar to those of stocks and other equity securities. ETF shares are bought and sold at market price, which may differ from the fund’s net asset value (NAV). Brokerage commissions may apply and will reduce returns. ETFs may be subject to the following additional risks:

Market Risk: The value of an ETF may decline due to broad market fluctuations unrelated to the underlying securities. Liquidity Risk: Some ETFs may have limited trading volume, which could make it difficult to buy or sell shares at a desired price. Tracking Error Risk: An ETF may not perfectly replicate the performance of its benchmark index. Concentration Risk: Sector or thematic ETFs may be concentrated in a particular industry or geography, increasing volatility. Currency Risk: ETFs that invest in international securities may be affected by exchange rate fluctuations. Leverage and Inverse Risk: Leveraged and inverse ETFs are designed for short-term trading and may not be suitable for long-term investors. These products use derivatives and may experience significant losses.

No Warranty While efforts are made to ensure the accuracy of information presented, no warranties are made regarding completeness, accuracy, or timeliness. Information may change without notice. Not a Fiduciary This site does not act as a fiduciary on behalf of any user. Users are encouraged to consult with a registered investment advisor, financial planner, or other qualified professional before making any investment decisions.

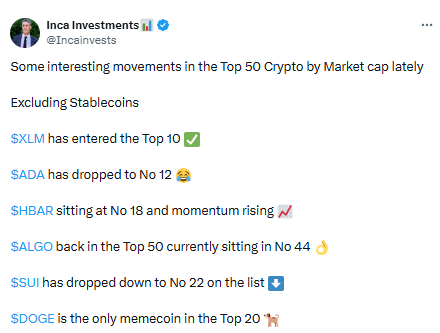

A notable shift is underway in the top 50 crypto rankings.

While some assets have slipped, others have climbed the market cap ladder, giving a clear picture of where liquidity may be flowing. This shift stands out because the market remains in a risk-off phase. During these periods, traders typically hunt for short-term rotation plays that can generate quick returns, while conviction around many large-cap assets remains relatively weak.

Nothing highlights this trend better than the post below.

Historically, risk-off phases have often seen capital flow into speculative assets such as memecoins. This time, however, the picture looks different. While Dogecoin remains the only memecoin in the top 20, the Hedera network recently climbed to 18th place as its market capitalization surged to around $4.6 billion.

Source: CoinMarketCap

Meanwhile, Stellar’s native asset, XLM, recently broke into the top 10 after its market cap hit a record $10 billion, signaling a similar rotation of capital.

The rise of both HBAR and XLM in the rankings is unlikely to be a coincidence. Instead, it points to a broader shift in market preferences. Rather than chasing high-beta narratives, investors appear to be allocating capital towards networks with stronger fundamentals, growing utility, and consistent on-chain activity.

The memecoin sector reinforces this view too. After shedding nearly 15% of its market capitalization this year, the sector has struggled to attract the same level of liquidity seen in previous cycles. And yet, the evidence extends beyond memecoins, making this trend an important signal of where capital is actually flowing.

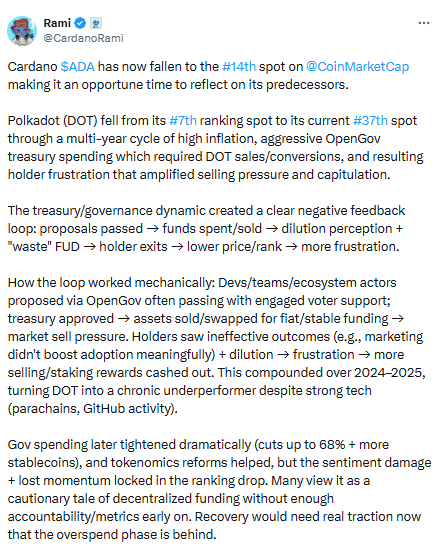

The top-10 shake-up signals a shift in crypto leadership

The shake-up in the top 10 has drawn the most attention.

According to CoinMarketCap, Cardano [ADA] fell out of the top 10, down to 13th place at press time. Its market capitalization slipped to around $8 billion, marking one of its lowest levels in nearly three years and highlighting the broader loss of momentum behind the asset.

However, the real story lies in the on-chain data. In a recent post, one analyst compared ADA’s declining position to Polkadot [DOT], which dropped from 7th place to 37th after years of token inflation.The analyst argued that many holders felt the spending failed to translate into meaningful growth, creating a cycle of weakening confidence.

In essence, ADA’s exit from the top 10 further seems to reinforce AMBCrypto’s thesis.

Source: X

The market is becoming increasingly selective.

Investors are no longer chasing narratives alone. Instead, they are allocating capital towards networks that can demonstrate sustained activity, growing adoption, and measurable economic value.

As a result, a new crypto order is beginning to emerge, with investors prioritizing fundamentals, on-chain activity, and real economic value over speculative narratives, particularly in a risk-off environment.

Final Summary

Money is moving towards stronger crypto networks like HBAR and XLM, while memecoins and weaker assets lose ground.

The market is now rewarding real usage and fundamentals instead of pure hype.

Bitcoin BTC$74,053.87 added as much as 0.4% since midnight UTC on Friday and was recently just 0.07% higher after slumping to its lowest level since early April the day before.

Thursday’s drop extended a decline that has emerged over the past three weeks after a failed attempt to climb above $83,000. There is now a chance that the rejection will have contributed to a series of lower highs dating back to October — a key characteristic of a bear market.

Ether (ETH) tracked bitcoin. It fell to $1,965 on Thursday before staging a recovery back above $2,000.

U.S stocks continued to outperform the crypto market on Friday, with S&P 500 and Nasdaq 100 index futures both posting 0.15% gains as the equity gauges approached fresh record highs.

There is no clear explanation why the crypto market is struggling against sectors it has historically been correlated with. The divergence since early October, however, aligns with a leverage wipeout that the market has failed to fully recover from.

Derivatives positioning

BTC open interest sits at $20.05 billion, up from $19.7 billion a week ago, with speculative positioning showing slight growth.

Funding rates remain positive across multiple venues at under 10% annualized. The exception is Deribit, where they spiked to 44%.

The three-month annualized basis pushed closer to 3%, led by Deribit, rising from 2.2% last week, pointing to a mild improvement in institutional risk appetite.

Options positioning shows mixed signals: one-week 25-delta skew ticked up to 12.85% from 12.4%, suggesting slightly higher demand for downside protection.

Front-end implied vol (DVOL) compressed to about 36 – the lowest since September — while the 1 month–6 month term structure slope sits at -6%, keeping the curve in contango. Markets are pricing near-term calm alongside longer-dated uncertainty.

Coinglass data shows $224 million in 24-hour liquidations, with a 54-46 split between longs and shorts. BTC ($46 million) and ETH ($43 million) were the leaders in terms of notional liquidations. The Binance liquidation heatmap indicates $72,280 as a core liquidation level to monitor, in case of a price drop.

Token talk

Stellar (XLM) was the top-performing altcoin on Friday, rising by 25% in the past 24 hours and 4.5% since midnight UTC after it was announced that The Depository Trust & Clearing Corporation (DTCC) is planning to connect its tokenized securities platform to the network.

There were also double-digit gains for ALGO, INJ, HBAR and HYPE over the past 24 hours as the altcoin market showed strength while the major cryptocurrencies showed weakness.

One asset that continued its woeful performance of late was BCH$303.37. The token that spawned out of a Bitcoin fork in late 2017 lost 7.2% of its value in the past 24 hours and has now shed 20% in the past week alone.

DeFi tokens are also losing their luster, with ENA, JUP and UNI dropping as much as 18% over the past week.

CoinMarketCap’s “Altcoin Season” indicator reflected the weakness on Friday, falling to 34/100 from 37/100.

Super Micro Computer (SMCI) has spent much of 2026 in the penalty box, with investors weighing AI demand against export-control risk and a series of legal headlines. But now the good news just came when Super Micro said it was working with Taiwanese authorities to prevent the illicit diversion of server technology.

Investors liked the news, and shares jumped 8.14% in Thursday’s trading.

More News from Barchart

In its statement, the company said the cooperation led to the arrest of three suspects and the seizure of 50 servers that had been deceptively acquired after being sold to an authorized reseller. But the story is not just about enforcement. It is about Super Micro trying to show tighter control over its channel at a time when its brand has been bruised by smuggling allegations.

The backdrop is still uncomfortable. Reuters reported in May that Taiwanese prosecutors were investigating three people over the alleged illegal export of high-end AI servers made by Super Micro, equipped with Nvidia chips (NVDA), in a scheme that allegedly involved falsified export documents.

Reuters had previously reported in March that U.S. authorities charged three people tied to Super Micro in a smuggling case involving billions of dollars of AI chips.

For Super Micro, the upside of the Taiwan action is reputational as much as operational. If management can show it is actively helping authorities shut down gray-market diversion, that could support customer trust and reduce the chance that one bad channel story becomes a broader indictment of the business. That is an inference, but it is a reasonable one given the centrality supply-chain credibility for an AI server vendor.

The Stock Still Appears Cheap on Paper

SMCI has rallied 55.72% year-to-date (YTD), fueled by booming AI-server demand, strong revenue guidance, Blackwell GPU shipments, and optimism around liquid-cooled AI infrastructure despite compliance and smuggling-related concerns.

Even after the outperformance, SMCI still trades like a stock with plenty of skepticism built in, with a forward price-to-earnings ratio of 18.05 times and a price-to-sales ratio of 0.63 times. Those are low multiples for a company tied to one of the market’s most important growth themes, and they suggest investors are paying more attention to risk than to growth.

That discount is partly because the market is not only pricing in slower AI spending, but also the possibility that Super Micro’s business model stays under pressure from compliance issues and channel scrutiny.

www.barchart.com

The Latest Quarter Still Showed Real AI Demand

Super Micro’s fiscal third-quarter 2026 results argued that demand has not disappeared. Net sales came in at $10.2 billion, down from $12.7 billion in the prior quarter but up sharply from $4.6 billion a year earlier.

Net income rose to $483 million, diluted EPS was reported at $0.68, beating the estimate by 23.6%. The company also reported $6.6 billion in cash flow used in operations, a reminder that growth is still carrying some working-capital strain.

Management’s outlook was also strong. For the fourth quarter of fiscal 2026, Super Micro projected net sales of $11.0 billion to $12.5 billion and EPS of $0.65 to $0.79. That kind of guidance helps explain why bulls still see the company as a major AI infrastructure winner, even if the stock has been weighed down by non-operating concerns.

The Last Word: Analysts Remain Split

Analyst views on Super Micro remain mixed. Goldman Sachs has a $26 target and a “Sell” rating, while JPMorgan cut its target to $28 and stayed “Neutral.” Citi lifted its target to $31, also with a “Neutral” view, and Northland has a $22 target.

Further, 19 analysts covering the stock rate it with a consensus “Hold” and an average price target of $35.73, implying 22.23% downside from current levels.

That split is probably the right way to read the stock. Super Micro is still a major AI hardware player with healthy demand, but the market is telling investors that execution, compliance, and trust will matter just as much as growth from here. The Taiwan crackdown is a useful step, not a full reset.

www.barchart.com

www.barchart.com

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com