Binance Coin [BNB] remained under pressure after facing rejection at $632 a week ago.

Since then, the altcoin lost the $600 support level and traded below it for four straight days.

At press time, BNB traded at $592 after gaining 0.65% over the past 24 hours. As the altcoin attempted to reclaim resistance, whales appeared to be positioning for a potential recovery.

Why did a whale swap gold for BNB?

With Tether Gold [XAUT] trading 24% below its January peak of $5,595, some investors appeared to be rotating into other assets.

According to Onchain Lens, a wallet linked to TechnoRevenant sold 492 XAUT worth $2.05 million. The wallet then used the proceeds to buy 3,457 BNB at an average price of $595. TechnoRevenant gained prominence for turning a $15 million early investment in World Liberty Financial (WLFI) into a position worth roughly $250 million and for making multi-million-dollar trades on Hyperliquid.

The move suggested the investor viewed BNB as offering stronger upside potential than XAUT at current levels.

Are whales still buying BNB?

TechnoRevenant joined a broader trend of whale accumulation. Even after BNB fell below $600, large investors remained active in the market.

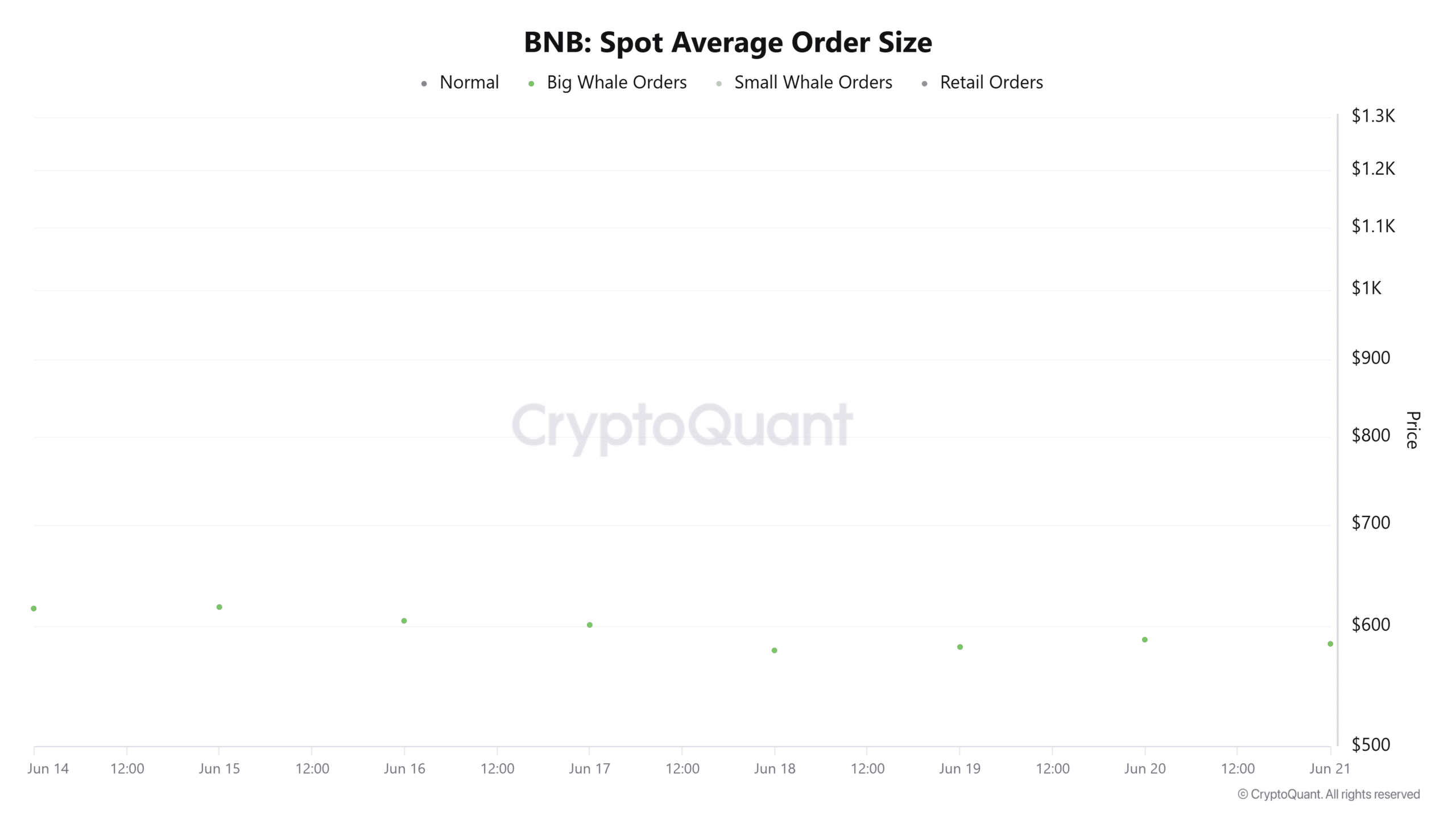

CryptoQuant’s Spot Average Order Size showed elevated whale-sized orders for seven consecutive days.

The metric reflected sustained participation from large traders. However, it did not reveal whether those orders were buys or sells. That shift set up a closer look at demand-side activity.

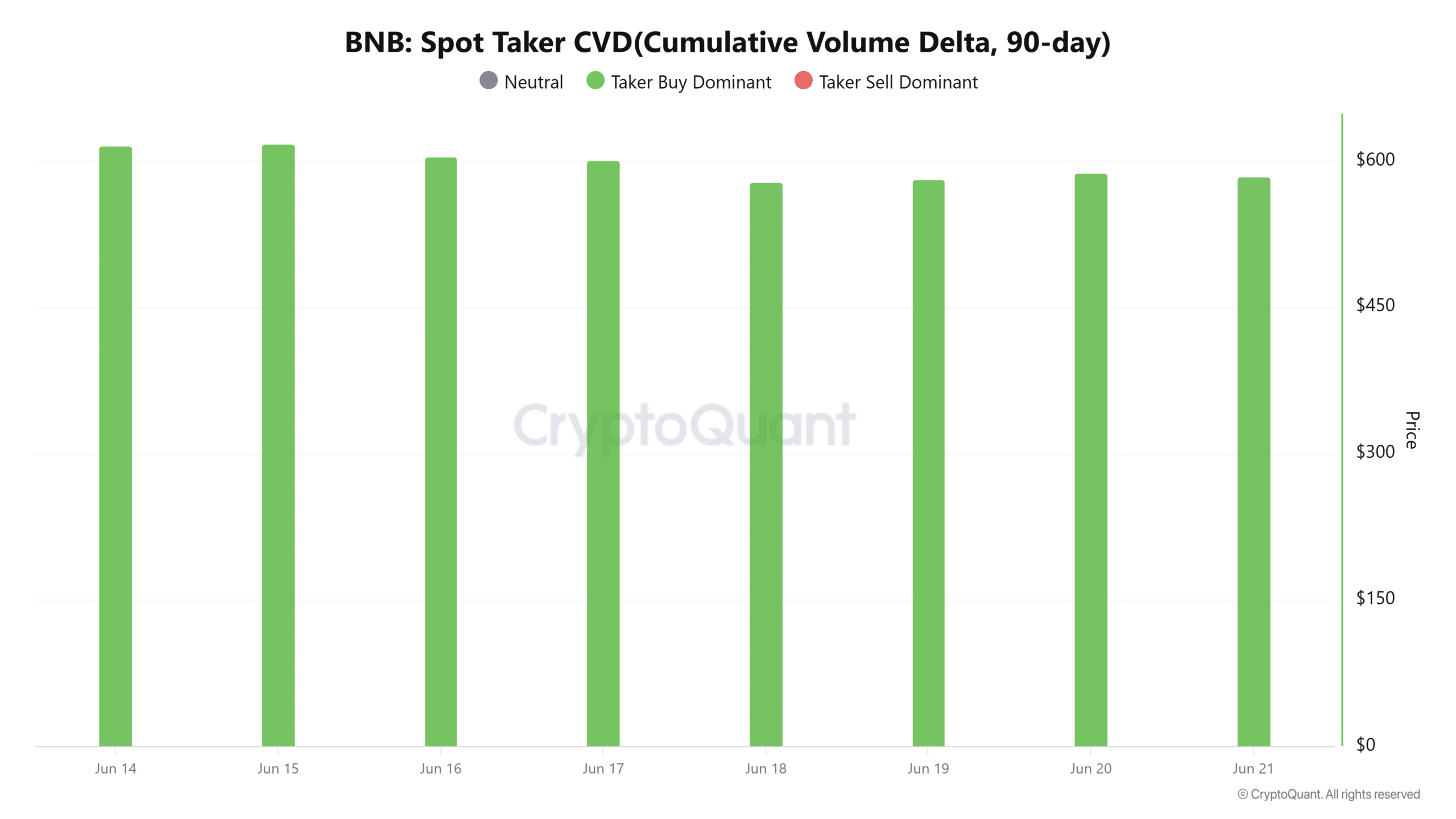

When combined with Spot Taker CVD, the picture appeared more constructive.

Spot Taker CVD remained buyer-dominant. Alongside elevated order sizes, this suggested whales continued accumulating BNB despite recent weakness.

Can BNB reclaim $600?

Whale demand coincided with signs of improving price strength. BNB recovered from $570 to nearly $595 over recent sessions.

The Relative Strength Index (RSI) formed a bullish crossover and climbed to 44. The move suggested that buying momentum was gradually returning. Even so, the RSI remained below the neutral 50 level.

With RSI at 44 and its signal line near 42, sellers still appeared active. That left traders focused on whether buyers could sustain momentum.

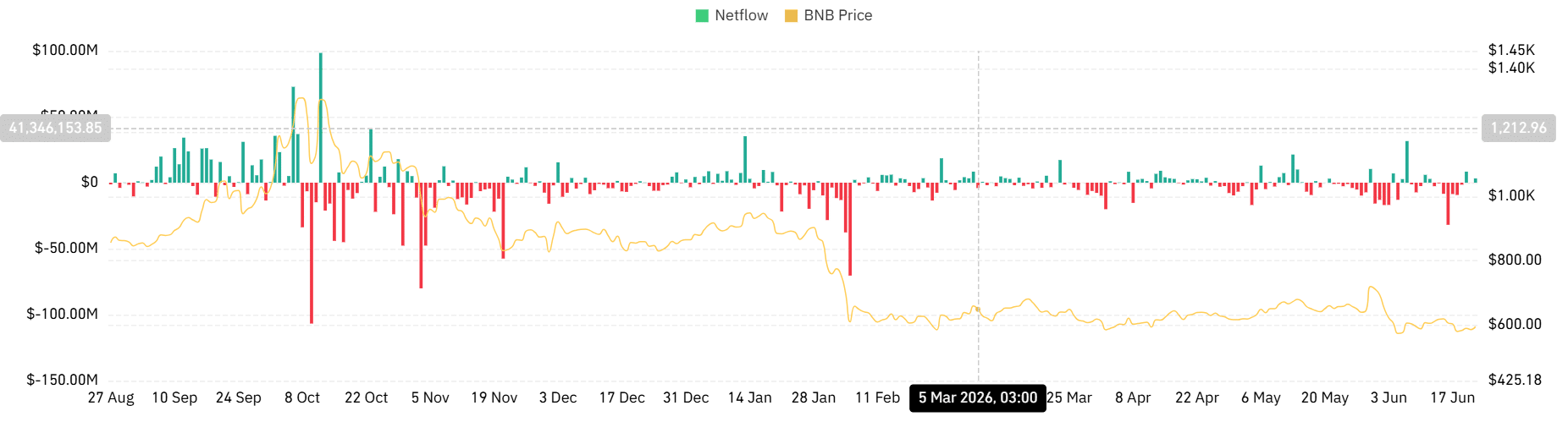

Spot Netflow offered a note of caution. The metric rose to $3.2 million on the 22nd of June, signaling increased exchange deposits.

Higher exchange inflows often indicate growing sell-side pressure. If whale demand remains strong, BNB could reclaim $600 and target $633. However, if exchange deposits continue rising, the altcoin could revisit the $560 support zone.

Final Summary

- A wallet linked to TechnoRevenant sold 492 XAUT for $2.05 million and bought 3,457 BNB.

- Binance Coin [BNB] shows slight bullish momentum as whales eye a move above $600.