Bitcoin BTC$76,720.46 may be entering a new period of outperformance against traditional assets as inflation pressures persist and bond markets weaken, according to Risk Dimensions chief investment officer Mark Connors.

Connors, who spent years as the global head of portfolio management at Credit Suisse, said bitcoin recently broke out of what had been its longest stretch of underperformance against the S&P 500 in history, a 142-day period that ended in early May.

“I think bitcoin’s underperformance versus markets is over,” Connors said in an interview. “It’s in the consolidation phase [that] has shifted into an outperformance phase.”

The shift comes as investors grapple with stubborn inflation, rising oil prices and uncertainty around interest rates. Connors argued that bonds, traditionally viewed as defensive assets, are increasingly under pressure as markets adjust to a “higher-for-longer” rate environment.

“Bitcoin, as it always does, takes it on the chin early, but then it always comes out first,” he said, adding that bitcoin could continue outperforming both equities and fixed income “as we grind through the straits of poor news and oil persistently being high.”

Connors tied much of the current macro environment to persistent geopolitical tensions and elevated energy prices. Oil has remained structurally high this year, he said, fueling inflation concerns while forcing markets to look toward technology and productivity gains as a counterweight.

He argued that AI and blockchain are becoming increasingly linked as businesses look for decentralized systems to support machine-driven transactions and automation.

“The only way to punch through that inflationary pressure is through technology,” Connors said.

He also pointed to shifting investor preferences between gold and bitcoin. Connors compared the current environment to 2020, when gold initially outperformed during the early stages of the pandemic before bitcoin began a strong resurgence.

“Gold has had its run,” he said. “Bitcoin is now on its resurgence.”

The U.S House Oversight and Governance Reform Committee has launched an investigation into prediction markets for alleged insider trading.

In a CNBC interview, Congressman James Comer (R-Kentucky), Chair of the Oversight Committee, claimed that prediction markets are “the wild west.” He added, “this is so new, and there are no written laws. Prediction markets have never been a problem until recent months.”

Comer cited the U.S soldier who profited by over $400K after betting on Venezuelan President Nicolás Maduro’s capture using insider intelligence.

He also mentioned the insiders who benefited from bets on the U.S-Iran war, alongside politicians trying to manipulate markets tied to their election races.

He continued,

We launched the investigation to see how widespread this (insider trading) is. But also to prove a case that we’ve got to pass some type of legislation like banning members of Congress, government employees, and people in the President’s administration from prediction markets.

In fact, a recent report showed that insiders on Polymarket made over $2.4 million on Iran bets. For Comer, the widespread insider trading activity is a sign that “Congressional action may be necessary.”

House press Kalshi, Polymarket for internal controls against insider trading

Kalshi is one of the largest prediction markets regulated by the Commodity Futures Trading Commission (CFTC). Its rival, Polymarket, has gotten approval to re-enter the U.S market, but has a massive global market share thanks to its lack of KYC (Know Your Customer) requirements.

Similarly, Kalshi has expanded to 120 global markets. However, the lack of KYC provisions for offshore markets is now raising concerns about bad actors gaming the markets. In a letter to Kalshi’s CEO Tarek Mansour, the Committee pressed,

The rapid global expansion of Kalshi’s platform raises questions about whether internationally placed event contracts are subject to equivalent identity verification and insider trading prohibitions as domestic event contracts.

A similar letter was sent to Polymarket’s CEO Shayne Coplan. Now, the Committee wants to know their KYC systems, whether it applies to global users, the trading history of any U.S government employee, including military officers, among others.

For example, India has banned prediction markets under the Promotion and Regulation of Online Gaming Act (PROGA). Recently, the Ministry of Electronics and Information Technology (MeiTY) flagged VPNs (virtual private networks) being used to bypass domestic restrictions on these betting markets.

Final Summary

The U.S Congress has officially launched an investigation into Polymarket and Kalshi for insider trading to help inform policy formulation.

India is cracking down on prediction markets and their enablers (VPNs), underscoring heightened global regulatory pressure.

President Donald Trump’s latest immigration crackdown is triggering alarm, confusion, and fierce debate among lawyers, advocates, and many in the business world who rely on visa holders for skilled labor.

On Friday, US Citizenship and Immigration Services announced it would grant “adjustment of status” — the process that allows some immigrants already in the US to apply for a green card without leaving the country — “only in extraordinary circumstances,” potentially forcing many applicants to return to their home countries and wait abroad while their cases are processed.

While a USCIS spokesperson told Business Insider that applicants who “provide an economic benefit or otherwise are in the national interest” may still qualify for exemptions, it remains unclear how broadly the administration plans to enforce the new restrictions or how many immigrants could ultimately be affected.

The administration has framed the move as a return to the original intent of immigration law, while critics warn it could upend the lives of foreign workers, mixed-status families, and long-term visa holders who have relied on the process for decades.

Here’s what smart people are saying about the sweeping policy shift.

Blake Scholl

Blake Scholl

Bloomberg/Getty Images

Blake Scholl, founder and CEO at Boom Supersonic, a company developing a supersonic airliner, said on X that he understands why “we don’t want people to come to the US to be criminals” and “mooch on welfare.”

“But I don’t understand why we make it harder for motivated, ambitious, hardworking people to come to the land of opportunity,” Scholl added.

Nick Davidov

Nick Davidov, the founder of Davidovs Venture Collective, a VC that supports repeat AI founders at the seed level,calledthe changes in the green card application rules “the biggest bullshit move by DHS in its history” and the “worst imaginable way to disrupt important work for the country.”

“So everyone on a O1 or H1B visa would have to stop working legally in the US, go back to their country and wait for years of backlog?” Davidov wrote on X on Friday. “This includes top scientists in our universities, founders of billion dollar companies.”

Davidov added in subsequent tweets that Iranians and Ukrainians can’t really return to their home countries for safety reasons, and that immigrants such as Elon Musk, Jensen Huang, and Sergey Brin have created some of the country’s most valuable companies.

Andrew Ng

Andrew Ng

Big Event Media/Getty Images for HumanX Conference

Andrew Ng, AI entrepreneur and cofounder of Coursera, called asking green card applicants to apply outside the US only “a capricious attack on legal immigration.”

“It will hurt families, leave us with fewer doctors, teachers and scientists, and hurt American competitiveness in AI,” Ng wrote on X on Friday.

Reid Hoffman

Reid Hoffman

Bloomberg/Getty Images

Reid Hoffman, cofounder of LinkedIn and a prominent Trump critic in Silicon Valley, wrote on X that the DHS’s new policies are a “harmful move for tech, business, and America broadly.”

“Does this mean AI Researchers, employees, and students will now have to leave the country and wait through a backlog process to continue their work?” Hoffman wrote.

Yvette Clarke

Rep. Yvette Clarke

Bill Clark/CQ-Roll Call, Inc via Getty Images

Rep. Yvette Clarke, a Democrat from New York, called the new green card policies “a disgrace.”

“It will rip talented, hardworking immigrants out from America and our economy, congest an already overburdened backlog, and further break an already broken immigration system,” said Clarke on X.

“And that’s by design,” Clarke added. “This administration has made the pain of immigrants a priority, and that won’t change until there’s no one left to hurt.”

David J. Bier

David J. Bier

Kayla Bartkowski/Getty Images

David J. Bier, the director of immigration studies at the Cato Institute, a libertarian think tank, called for new leadership of USCIS in a series of posts on X on Friday, where he said that the new policies show “total malice against the applicants.”

“The policy is a radical expansion of DHS’s ‘quiet quitting’ on legal immigration that has been going on for months,” Bier also wrote in a blog post. “Now USCIS’s new memorandum details a plan for mass denials. USCIS has gone from the ‘quiet-quit’ to walking out on 1.2 million green card applicants.”

“Forcing green card applicants to leave will render many green card applicants ineligible because, when they leave the United States, they will trigger the 3- or 10-year bars on receiving an immigrant visa based on accrual of unlawful presence,” Bier added.

Yann LeCun

Yann LeCun

Yui Mok – Pool/Getty Images

Yann LeCun, a pioneer in AI research and the former Chief AI Scientist at Meta, had a very curt and perplexed response to the change in green card policy.

“Why?” wrote the ACM Turing Award Laureate on X, who reposted an article detailing the DHS’s announcement.

LeCun was born in France and immigrated to the US in the late 1980s.

Garry Tan

Y Combinator CEO Garry Tan

Hutton Supancic/SXSW Conference & Festivals via Getty Images

Garry Tan, the CEO of the startup accelerator Y Combinator, called the new guidance “bad and misguided.”

“We need to keep smart people in the country to build the future and build tomorrow’s businesses that employ millions of people,” he wrote on X.

Ash Jogalekar

Ash Jogalekar, a Microsoft senior project manager working on agentic AI, described the memorandum as “self-sabotage” in an X post on Friday.

“As a scientist and immigrant who loves this country, I cannot think of worse ways to cripple American scientific competitiveness while other countries surge ahead,” Jogalekar wrote. “It is completely pointless. Between the funding cuts and rash, irrational policies like these, China could not have done worse if they had decided to sabotage science in the U.S.”

Jason Calacanis

Investor and All-In podcast co-host Jason Calacanis

Bridget Bennett/Bloomberg via Getty Images

Jason Calacanis, investor and co-host of the All-In podcast, said in an X post on Saturday that the US should encourage more immigration in response to the administration’s new green card policy.

“America’s goal should be to expand our Empire,” he wrote. “Be it immigration, acquisition or invitation, if you believe we have the best system then you should embrace expansion.”

The investor also posted a clip of an interview All-In did with Trump in 2024, during which the president said college graduates should “automatically” get a green card.

“More green cards for extremely talented immigrants!” Calacanis wrote in the post. “Strong agree President Trump.”

Every generation of Wall Street workers learns the same lesson the hard way. The bank you joined is rarely the bank you retire from. Roles get reshuffled, divisions get sold off, and the career path that looked rock-solid on day one almost never matches the one that pays out at year 30.

For decades, the safe play inside a giant like JPMorgan Chase (JPM) was simple. Learn the products, build a book of business, climb the ladder. The senior bankers who shepherded clients through deals, financings, and downturns were the ones who got promoted, paid, and protected when the cycle turned.

That model still works. But it is being quietly rewritten in real time, and the man running the rewrite has spent the past few years warning anyone who would listen that the next decade in finance would look nothing like the last.

Now Jamie Dimon has put a sharper edge on what he means. The JPMorgan chief executive told Bloomberg Television that the bank will hire more artificial intelligence specialists and fewer traditional bankers in certain categories as automation accelerates across Wall Street.

Jamie Dimon said JPMorgan plans to reduce headcount, shift hiring

Speaking at JPMorgan’s China Summit in Shanghai on May 21, Dimon was direct about where headcount goes next.

“I think it will reduce our jobs down the road,” he said in the interview, according to Bloomberg.

“There will be all different types of jobs, and I think we will be hiring more AI people and fewer bankers in certain categories, and it will make them more productive,” Dimon added.

More AI:

Dimon’s framing matters. He is not talking about a sudden wave of pink slips. He is talking about a steady reshaping of who gets a job offer in the first place, while existing staff get retrained, redeployed, or pushed toward early retirement.

JPMorgan’s annual attrition runs at roughly 10%, or about 25,000 to 30,000 employees a year, which gives leadership real room to shift the mix without dramatic layoffs, reported Bloomberg.

When I look at what JPMorgan has been quietly building over the past 18 months, the math behind Dimon’s comment becomes obvious. The bank’s tech budget sits near $20 billion, with roughly $2 billion of that earmarked specifically for AI, reported Fast Company. JPMorgan has also started tracking and ranking its engineers on internal dashboards based on how heavily they use AI tools.

That is not a bank trying to manage AI on the side. That is a bank rebuilding its operating model around it.

Jamie Dimon tells Bloomberg AI will reduce the firm’s jobs down the road.Photo by Bloomberg on Getty Images

Why JPMorgan is rewiring its hiring around AI

Dimon is not the only Wall Street chief making this call. He is just the loudest.

Wells Fargo (WFC) CEO Charlie Scharf said in December that the bank expected fewer employees in 2026 than 2025, with AI cited as a major reason.

Generative AI tools have already made the bank’s engineering teams “30% to 35% more efficient in terms of writing code today,” Scharf said, according to Reuters.

Across emerging markets, Standard Chartered chief executive Bill Winters has been even more blunt, telling staff the bank is replacing “lower-value human capital” with technology and eliminating 8,000 support roles over the next four years, reported Bloomberg.

A few data points stand out when I run them together:

JPMorgan Chase: 318,153 employees as of September 2025, with annual attrition of about 25,000 to 30,000, Bloomberg noted.

Wells Fargo: 275,000 employees in 2019 down to about 210,000 by Sept. 30, 2025, according to Reuters.

Standard Chartered: 8,000 support roles slated to be cut over the next four years, Bloomberg confirmed.

Six major U.S. banks: Combined $47 billion in a recent quarter, up 18%, while shedding 15,000 employees collectively, Entrepreneur reported.

Global banks: Up to 200,000 jobs at risk over the next three to five years, according to Bloomberg Intelligence.

Tomasz Noetzel, the senior analyst who authored the Bloomberg Intelligence report, told Bloomberg that “any jobs involving routine, repetitive tasks are at risk,” adding that AI “will not eliminate them fully, rather it will lead to workforce transformation.”

That is the polite version of Dimon’s same point.

What the AI hiring shift means for your money

For consumer-investors, the AI banking story has two sides, and they pull in opposite directions.

On the equity side, Bloomberg Intelligence forecasts that AI could lift bank pre-tax profits by 12% to 17% by 2027, adding as much as $180 billion to the sector’s collective bottom line. Eight in 10 surveyed executives expect generative AI to boost productivity and revenue by at least 5% over the next three to five years, according to Bloomberg.

In plain English, that is a strong tailwind for the same megabank stocks held by every major S&P 500index fund and most retirement target-date portfolios. The earnings power inside your 401(k) is quietly being supercharged by what is happening to the people on these banks’ payrolls.

On the household side, the picture is less comforting. Citi previously found that about 54% of banking roles carry a high likelihood of AI displacement, the highest exposure of any sector studied, the Bloomberg Intelligence report noted.

What stood out to me when I lined those numbers up was the speed. Wells Fargo alone has shrunk by roughly 65,000 employees in six years. Six of the country’s largest banks dropped 15,000 jobs in a single recent quarter while booking record profits.

The compression was real before generative AI hit Wall Street’s desks. Now it is accelerating, the kind of shift TheStreet has been tracking inside the broader forever layoffs cycle.

If you bank with one of these giants, expect fewer humans on the phone, more chatbots, more automated underwriting decisions, and faster but less negotiable customer interactions. If you work in financial services, the safest seats look increasingly like the ones tied to client relationships, judgment calls, and direct revenue generation, not the ones tied to repeatable middle-office tasks.

Dimon’s message in Shanghai was not really about layoffs. It was about a hiring filter. Going forward, JPMorgan wants people who can build, deploy, and oversee AI more than it wants people who can simply run the existing process.

For shareholders, that is likely good news for margins. For ambitious junior bankers eyeing the next 10 years inside a Wall Street giant, it is a quieter reminder. The safest career in 2026 may not be the one their predecessors chose. It may be the one that did not exist three years ago.

After crumbling about 4% late Friday into early Saturday, bitcoin BTC$76,382.75 has more than retraced those losses in the past few minutes after President Trump announced a coming agreement with Iran and other Middle Eastern countries.

“An Agreement has been largely negotiated, subject to finalization between the United States of America, the Islamic Republic of Iran, and the various other Countries,” wrote Trump in a Truth Social post.

“In addition to many other elements of the Agreement, the Strait of Hormuz will be opened,” the president continued.

The news sent bitcoin sharply higher to $76,700 after having fallen to nearly $74,000 earlier on Saturday.

Pudgy Penguins [PENGU] is down 14% in the past 24 hours. PENGU had the biggest loss among CoinMarketCap’s top 100 crypto tokens during this period.

A couple of factors influenced this sudden crash, which occurred after a week of positive gains across the crypto sector.

Monthly unlocks fuel selling pressure

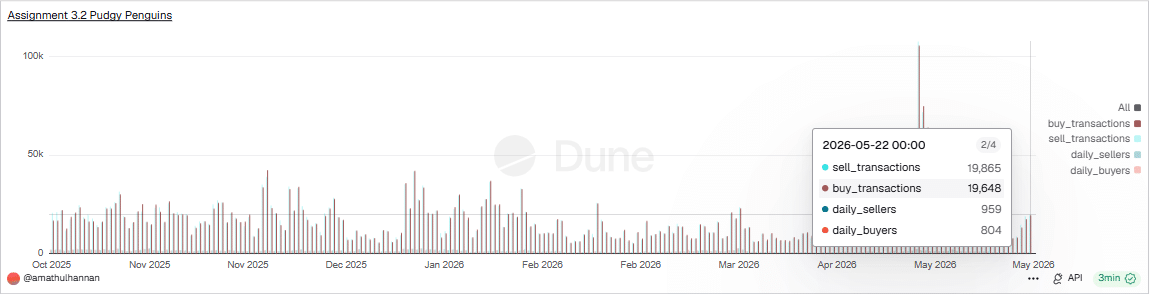

The number of transactions was growing, but sellers dominated them more. According to Dune Analytics, sell transactions were 19,865, while those of buyers were 19,648. However, the difference was not that big.

Additionally, the number of daily sellers was 959, while the number of buyers was 804.

Source: Dune Analytics

This sale came as a result of monthly unlocks of 712.4 million PENGU worth $6.25 million.

Of this amount, 279.3 million PENGU worth $2.45 million was meant for the company, while 433.1 million tokens valued at $3.80 million went to the current and future teams.

Network data from Arkham showed the teams distributed their tokens this week, valued at $3.40 million. Hence, this development potentially sparked sell pressure from on-chain traders.

Source: Arkham

Furthermore, capital was leaving the broader altcoin market, and trending tokens like PENGU were taking the hardest hit. An increase in daily trading volume by 17% to around $181 million affirmed the sell pressure.

Additionally, the decline in collections like Bored Apes spread into PENGU because it is intertwined with the NFT sector. The memecoin is highly sensitive to sentiment shifts away from digital collectibles.

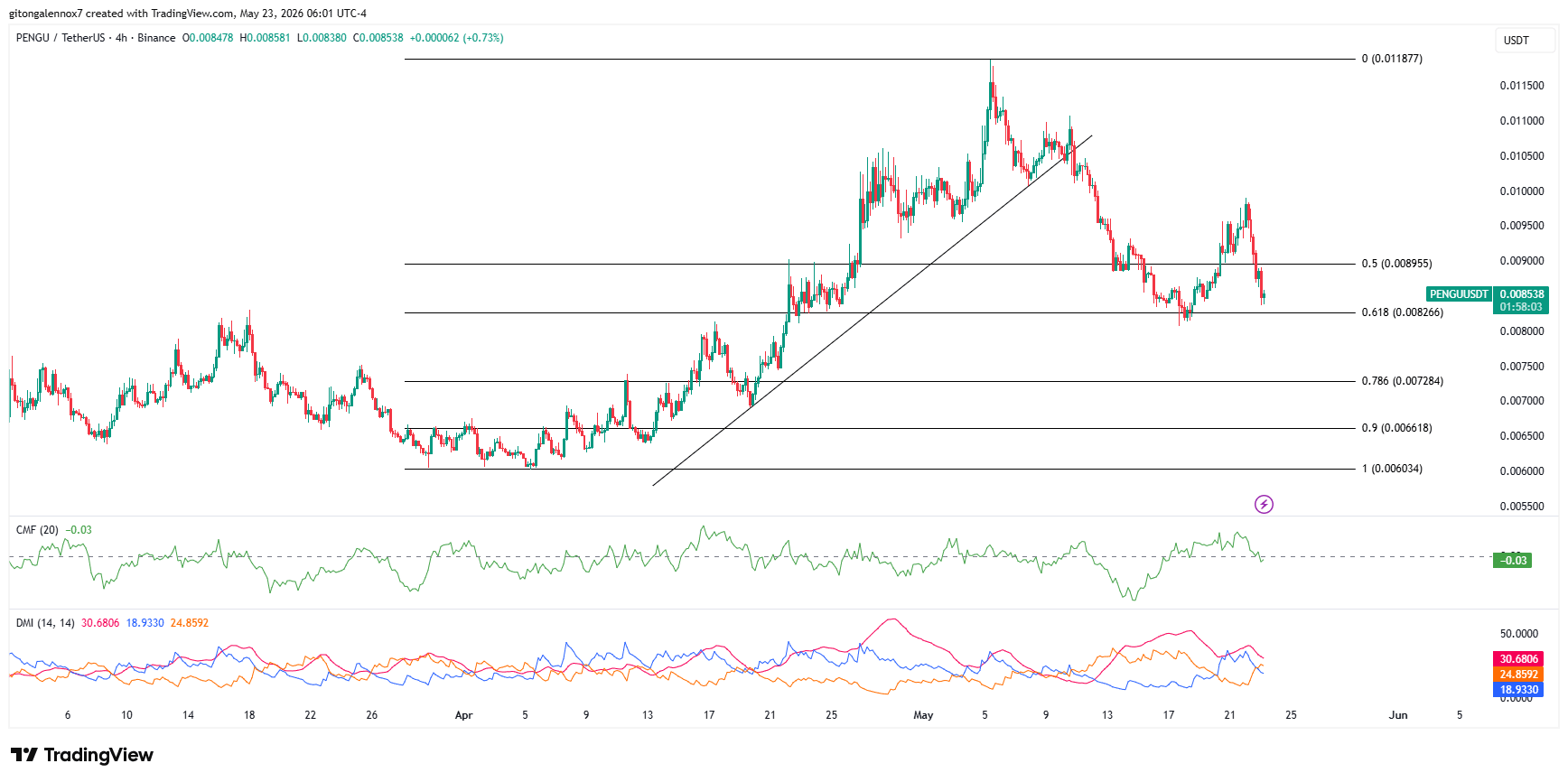

Can PENGU bounce off the 0.618 Fib level?

PENGU broke a rising trendline support and dropped to the 0.618 Fibonacci Retracement level. At this level, the memecoin has recovered half of the 31% crash but is approaching the level for the second time.

Bulls are returning at this level even though capital flows are negative. The Chaikin Money Flow is -0.02, as well as a declining Directional Movement Index (DMI). The DMI lines are all pointing downwards.

As price forms a potential turning point at $0.008266, the second touch of the 0.618 Fib level could spark a rebound. This would need PENGU breaking above $0.009846 to confirm an uptrend continuation.

Otherwise, if sellers maintain their momentum, they might break the level down. As a result, the next targets would be at $0.007284 or lower.

Source: PENGU/USDT on TradingView

Therefore, the crash may not last, especially if the market prices in the unlocked tokens of this month.

Final Summary

PENGU loses 14% in the past 24 hours amid broader crypto market correction and massive monthly token unlock.

Price approaches the 0.618 Fib level for the second time, which, if defended, could ignite a reversal.

An Egyptian French-made Dassault Rafale fighter jet deployed to the United Arab Emirates. (UAE Ministry of Defense photo)

UAE Ministry of Defense

The U.S.-Israel war against Iran, launched on February 28, saw Tehran take the unprecedented step of repeatedly targeting all six Arab Gulf monarchical member states of the Gulf Cooperation Council with ballistic missile and explosive drones. After the April 8 ceasefire halted hostilities, some in the Gulf states began questioning why larger regional powers like Egypt didn’t do more to help defend them against Iran.

Iran and its regional militia proxies fired missiles and drones at the Gulf states throughout the war, with the United Arab Emirates enduring the brunt of these attacks. The UAE’s world-class air defense found itself under unprecedented strain, and the daily Iranian attacks undermined its carefully cultivated reputation for security and stability that Abu Dhabi strove to uphold for decades.

The Emirates and other GCC states provided grants and investments worth tens of billions of dollars to Egypt to prop up its economy since 2013. The war consequently left some Gulf Arabs wondering aloud why Egypt, which has the largest army of any Arab country, didn’t do more to assist them militarily.

In another unprecedented development of the war, Israel forward-deployed troops to operate Iron Dome anti-rocket and even the new Iron Beam laser defense system to help defend Emirati airspace from these constant attacks.

Tareq al-Otaiba, a former official in the Emirati national security council, wrote a scathing article for the Arab Gulf States Institute, charging that the Iran war exposed “the hollowness of Arab solidarity.”

“In the face of Iranian aggression, several states have stepped up to provide real assistance to the UAE,” he wrote. “Primarily, the United States and Israel have proved to be true allies by offering support through extensive military aid, intelligence sharing, and diplomatic backing.”

“The same support has not come from the Arab world.”

Al-Otaiba also correctly noted that the crisis was the worst the Gulf has seen since August 1990, when Saddam Hussein’s Iraq infamously invaded and annexed the GCC member state of Kuwait. On that occasion, the U.S. responded by assembling a multinational coalition that expelled the Iraqi Army in the ensuing 1991 Persian Gulf War.

Since then, the United States has remained the predominant military backer and arms supplier of the Gulf states, which host various American air and naval forces in large bases throughout the region that Iran bombarded during this latest war.

None of this necessarily means that other regional powers did nothing as the GCC faced its worst crisis since 1990.

Almost a month after the April 8 ceasefire, the UAE Ministry of Defense revealed that Egypt had deployed some of its French-made Dassault Rafale multirole fighter jets to the Gulf state. Egyptian President Abdel Fattah el-Sisi even visited and “conducted an inspection visit to the Egyptian fighter detachment stationed” there with his Emirati counterpart, Mohamed bin Zayed al-Nahyan. How many of these jets, where they are stationed, and whether they played an active role in helping the UAE shoot down drones during the conflict, remains unclear. Nevertheless, their deployment is a symbol of Egypt’s support for its Gulf ally’s defense and certainly isn’t nothing.

France deployed 12 Rafales to the UAE during the war which intercepted several drones. The French fighters expended at least 80 MICA air-to-air missiles, an expensive and unsustainable way of shooting down relatively inexpensive Iranian drones. France has already modified the Rafale’s cannon to intercept such drones more cost-effectively, something the UAE has probably taken note of, given the pending delivery of 80 Rafale F4s Abu Dhabi ordered in December 2021. In the meantime, Egyptian Rafales could conceivably augment their French counterparts if Iranian drone attacks resume in the near future.

The United Kingdom has also armed its Eurofighter Typhoons operating in the Middle East with the cost-effective Advanced Precision Kill Weapon System, which uses relatively inexpensive laser-guided rockets rather than conventional air-to-air missiles to intercept drones. The UAE and several other Gulf states have made large orders of thousands of APKWS rockets after their respective experiences in dealing with unrelenting Iranian drone barrages during the war.

The Wall Street Journal recently reported that Egypt also deployed ground-based air defenses to the UAE and other Gulf states during the war. The systems in question were reportedly the Skyguard Amoun, which integrates anti-aircraft guns and surface-to-air missiles, making it suitable for providing point defense for bases and critical infrastructure. As with the Rafales, it’s unclear if these intercepted anything.

Additionally, Reutersreported that Saudi Arabia’s longtime ally, Pakistan, had deployed 8,000 troops, along with JF-17 Thunder multirole fighter jets and long-range Chinese-made HQ-9 air defense missile systems to the kingdom. Islamabad has stationed troops on Saudi soil during past regional crises, including the Iran-Iraq War and the 1991 Persian Gulf War, to help bolster its defenses. The Iran war was no different. It’s also long been suspected that Pakistan and Saudi Arabia have an understanding in which the former would put its nuclear arsenal at the disposal of the latter if the kingdom faced an existential threat.

Today, Pakistan, Egypt, and Turkey, which also have troops and F-16 fighter jets stationed in GCC member Qatar, are earnestly pushing for negotiations aimed at ending hostilities with Iran. They have a vested interest in doing so: both for regional security and stability and, of course, to mitigate the risk that their troops and military hardware in the Gulf could come under Iranian fire if this regional war resumes.

The war wasn’t the first time the GCC had found its regional allies somewhat lacking in providing an alternative or parallel military support to the U.S. and other Western armed forces.

In the 1980s, leading GCC states supported Saddam Hussein’s Iraq during the Iran-Iraq War with the notable exception of Oman. Muscat has always had the closest ties to Tehran of any GCC state, but that still didn’t spare it from Iranian attacks this year. Back then, Oman shrewdly understood that “only Tehran could potentially act as a balance to an immensely powerful Baghdad,” which Saudi Arabia and Kuwait were financing and helping to become a predominant military power in the region with an enormous army. A mere two years after the Iran-Iraq War ended, Saddam Hussein infamously annexed Kuwait, sending shockwaves throughout the GCC states. In 2019, then-Iranian President Hassan Rouhani even argued that Saudi Arabia and the UAE only survived that crisis because Tehran didn’t cooperate with Saddam Hussein against them.

While the U.S.-led coalition liberated Kuwait and shielded the GCC, these states briefly explored a regional non-American solution for their defense. The subsequent March 1991 Damascus Declaration envisioned the GCC financing a long-term deployment of Egyptian and Syrian troops in Kuwait and Saudi Arabia to defend them against Iraq. Both Arab countries had provided sizable troop detachments to the U.S.-led coalition that fought the Gulf War.

However, grand plans for a permanent force of up to 100,000 Egyptian-Syrian troops were quickly reduced to a much more “symbolic” force of a mere 3,000 to 5,000. Even newly liberated Kuwait expressed its belief that there was “no substitute for Western might.”

Egyptian and Syrian troops left the Gulf by the summer of 1991, and talk of any Egypt-Syria force was abandoned by the end of the year or, in the words of one retrospective analysis, “achieved the status of a footnote in history.”

Whether the current Egyptian and Pakistani deployments will become a similar footnote remains to be seen, though it’s already apparent that, at least as far as some in the GCC states are concerned, they cannot adequately substitute for American military might.