The rest was scattered. ZachXBT traced more than $12 million to deposit addresses at the KuCoin exchange and about $8 million to instant swap services, which convert one coin into another quickly and often without identity checks.

Another $8 million was moved off Tron onto the Bitcoin and Ethereum networks through Near Intents, a cross-chain swap tool. Spreading funds across coins, exchanges and blockchains is a common way to break the trail.

Then Tether stepped in. The company can freeze USDT held at a specific address, and ZachXBT said it blacklisted an address tied to the entity holding 72 million USDT. Once frozen, those tokens cannot be moved or cashed out.

It is unclear where the $120 million originally came from. But the pattern, fast movement into a privacy coin, instant swaps and cross-chain hops, is the kind used to launder illicit funds, and Tether’s freeze suggests it reached the same conclusion.

UPDATE (June 12, 12:40 UTC): Amends headline and body to include percentage figure for XMR’s gains.

The next 48 hours could be one of the most volatile periods for risk assets this year, starting Monday.

Between the 15th and 16th of June, the Bank of Japan (BOJ) will release its much-anticipated interest rate outlook. This will be followed by the FOMC meeting on the 16th and 17th of June, where the Federal Reserve will announce its policy decision.

In essence, two of the world’s most influential banks will take center stage.

Market expectations are fairly one-sided.

Why could this week move crypto?

According to CME FedWatch, over 97% of participants are pricing in no change in interest rates at the upcoming Fed meeting. On the BOJ side, however, rate hike expectations are much more active, something that has historically lined up with short-term corrections in crypto.

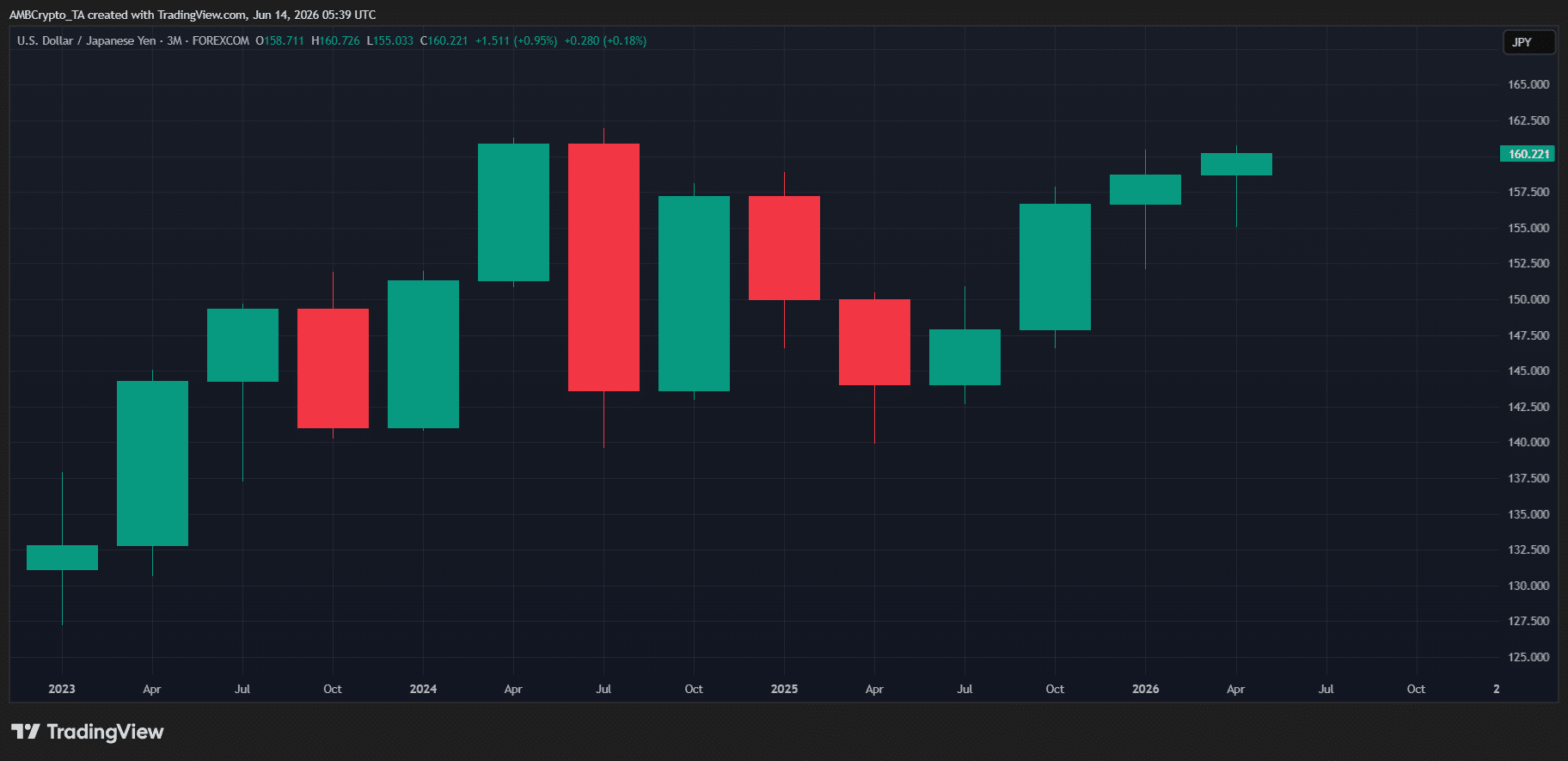

Source: TradingView (USD/YEN)

From a technical view, the Japanese yen keeps weakening against the U.S. dollar. USD/JPY is up around 2.5% year-to-date, pushing back toward the 160 level last seen in early Q3 2024.

In other words, we’re seeing continued dollar strength and yen weakness heading into a pretty key macro event window.

From an economic perspective, a weaker yen puts pressure on the BOJ’s interest rate path.

As the currency depreciates, import costs rise, which can feed into higher inflation in Japan. That, in turn, increases the likelihood that the BOJ considers tightening policy or signaling a more hawkish stance.

More importantly, the timing of this volatility window couldn’t really be worse. The simple idea is this: Even a slightly “cautious” tone from the Fed could be enough to shake markets, and given the current setup in crypto, the market’s ability to absorb that kind of pressure looks pretty limited.

Crypto enters a decision zone, not a trend phase

The upcoming macro week is shaping up alongside a highly volatile crypto market.

On the technical side, high-cap assets still trade over 20% below their earlier 2026 peaks. The recent sell-off lines up with stronger-than-expected labor data, which pushed Bitcoin [BTC] below $60k.

BTC has since bounced nearly 7%, but the market is still split on whether a bottom is in, with bearish signals keeping the risk of another correction on the table.

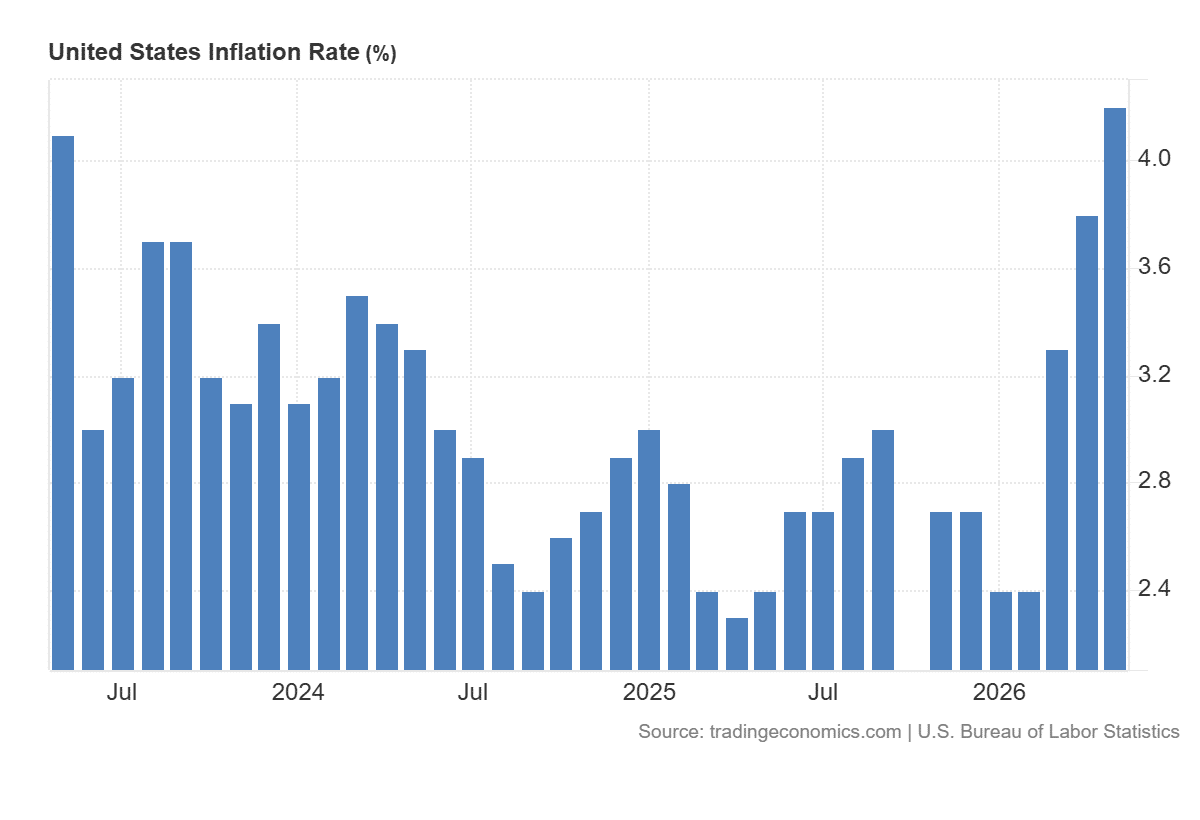

On the macro side, inflation data suggest the Federal Reserve may stay cautious.

As shown in the chart below, U.S. monthly inflation came in at 4.2%, the strongest reading since the Q2 2023 cycle. In simple terms, sticky inflation keeps the Fed tilted toward a no-rate-cut stance heading into the upcoming FOMC.

Source: TradingEconomics

Against this backdrop, the recent Bitcoin rally starts to look like a textbook bull trap.

The logic is simple: BOJ pricing in a potential rate hike, the Fed staying cautious, weak technicals, and an already volatile crypto market all point to a setup that doesn’t look strong enough to carry through the upcoming macro week.

That kind of pressure puts longer-term positioning under stress and keeps overexposed longs at risk of liquidation.

In this setup, a breakdown below $60k for BTC stays firmly in focus.

Final Summary

BOJ and Fed meetings this week could trigger sharp moves as markets stay highly sensitive to interest rate signals.

Weak crypto momentum and sticky inflation keep BTC at risk of a drop below $60K if selling pressure picks up.

Moneywise and Yahoo Finance LLC may earn commission or revenue through links in the content below.

High net worth individuals — typically those with $1 million or more in investable assets — held large portions of their total portfolio in cash in 2024. According to a survey conducted by Goldman Sachs, wealthy individuals park roughly 20% of their net worth in cash and cash equivalent holdings (1).

Higher market volatility and fears regarding persistently high inflation levels are a few major contributors to the shift away from equities and bonds.

Top Picks

The ultra-rich use these 5 real estate strategies to build wealth while they sleep — you can start with just $100

The IRS usually taxes gold as a collectible — but this little-known strategy lets you hold physical bullion tax-free. Get your free guide from Priority Gold

Dave Ramsey warns nearly 50% of Americans are making 1 big Social Security mistake — here’s how to fix it ASAP

And at least some ultra-high-net-worth individuals seem to agree. Before retiring on Dec. 31, 2025, Warren Buffett — the former Berkshire Hathaway CEO and the world’s ninth-richest person according to Forbes real-time net worth tracker (2) — had built the company’s cash balance to a staggering $381.7 billion by the end of the third quarter of 2025 (3).

The strategy paid off — Buffett’s net worth grew by roughly $21 billion last year, despite a tumultuous market backdrop.

Buffett isn’t the only one quietly ditching stocks. Billionaire investor and co-founder of PayPal, Peter Thiel, sold roughly $100 million worth of Nvidia shares through his hedge fund, Thiel Macro, in the third quarter of 2025 (4).

While Nvidia’s stock price surged by nearly 35% in 2025, such moves by the ultra-wealthy spark concerns about a potential AI bubble (5).

As U.S. equities grapple with uncertainties amid the ongoing tariff concerns and potential market overvaluation, cash and cash equivalents might help you hold onto your wealth in stormy weather.

Better investment alternatives

The richer investors get, the more likely they are to look beyond traditional investments. The Goldman Sachs survey revealed that nearly 4 in 10 people with $1 million to $5 million in investable assets have exposure to alternative investments. For those with more than $10 million, alternatives are even more common, with 80% holding them in some form.

For those who don’t want to deal with stock market volatility, there are accessible ways to invest in alternative assets and shield yourself from a potential crash.

One alternative option that can provide returns amidst economic turmoil is real estate.

Rental properties have long been a proven source of steady, passive income for investors. But managing properties costs time, effort and serious cash that many investors simply don’t have.

With that said, that doesn’t mean that there aren’t options for those looking to tap into real estate as an investment vehicle without the hassle of property management.

Turn your cash into rental income

One way to get into this market is by investing in shares of vacation homes or rental properties through Arrived.

Backed by world-class investors, including Jeff Bezos, Arrived allows you to invest in shares of vacation and rental properties, earning a passive income stream without the extra work that comes with being a landlord.

To get started, simply browse through their selection of vetted properties, each picked for their appreciation and income-generating potential. Once you choose a property, you can start investing with as little as $100, reaping any quarterly dividends.

Become a corporate landlord

Residential real estate isn’t the only option if you’re keen to diversify.

If diversifying into multifamily rentals appeals to you, you could consider investing with Lightstone DIRECT, a new investing platform from the Lightstone Group, one of the largest private real estate companies in the country with over 25,000 multifamily units in its portfolio.

Since they eliminate intermediaries — brokers and crowdfunding middlemen — accredited investors with a minimum investment of $100,000 can gain direct access to institutional-quality multifamily opportunities. This streamlined model can help reduce fees while enhancing transparency and control.

And with Lightstone DIRECT, you invest in single-asset multifamily deals alongside Lightstone — a true partner — as Lightstone puts at least 20% of its own capital into every offering. All of Lightstone’s investment opportunities undergo a rigorous, multi-stage review before being approved by Lightstone’s Principals, including Founder David Lichtenstein.

How it works is simple: Just sign up with your email, and you can schedule a call with a capital formation expert to assess your investment opportunities. From here, all you have to do is verify your details to begin investing.

Founded in 1986, Lightstone has a proven track record of delivering strong risk-adjusted returns across market cycles with a 27.6% historical net IRR and 2.54x historical net equity multiple on realized investments since 2004. All told, Lightstone has $12 billion in assets under management — including in industrial and commercial real estate.

As such, even if multifamily rentals don’t appeal to you, Lightstone could still serve you well as an investment vehicle for other real estate verticals.

Fine art tends to maintain its value during turbulent markets. According to a 2025 survey conducted by UBS, high-net-worth collectors are still maintaining their confidence in art — allocating roughly 20% of their wealth in the asset on average in 2025 (6).

Until recently, this world was off-limits to many investors. Not everyone has the time — or cash — to secure a beloved piece of contemporary art. Besides, much of the art world is locked behind a network of brokers, gallery owners and appraisers.

Now, with Masterworks, you can buy fractional shares in multimillion-dollar works by icons like Banksy, Picasso and Basquiat. While art can be illiquid and typically requires a long-term hold, it offers unique portfolio diversification.

Masterworks has sold 25 artworks so far, yielding net annualized returns like 14.6%, 17.6%, and 17.8%.

Even better, if you’re interested in art you can skip the waitlist and go straight to investing.

Note that past performance is not indicative of future returns. Investing involves risk. See important Regulation A disclosures at Masterworks.com/cd

You May Also Like

Join 250,000+ readers and get Moneywise’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

Over 40 million Americans have reported using GLP-1 drugs for weight loss, a behavior reshaping everything from the healthcare industry to pop culture and consumer behavior—and the drugs’ use could balloon into as much as a $240 billion market.

While these weight-loss drugs pumped billions into pharma giants Eli Lilly and Novo Nordisk as social media and celebrity endorsements drove more people to buy them, the companies may not be the only ones to financially benefit. According to a new study released by the National Bureau of Economic Research (NBER), taking GLP-1s for obesity might also save middle-aged Americans hundreds of thousands of dollars in lifetime medical bills.

“Obesity is a big comorbidity for a lot of different chronic conditions, so if you start GLP-1s, like that’s gonna kind of trickle down, and it’s gonna save money,” the study’s lead author, Felipe Montano-Campos, told Fortune.

NBER’s report estimated that people between the ages of 40 and 50 saved on average $192,735 in lifetime medical bills. Surprisingly, those savings climbed to $220,000 for adults within the same age range without college degrees. Largely, this is due to GLP-1s treating obesity without the usual tried-and-true means to lose weight, namely, a strict regimen of diet and exercise, explained Montano-Campos.

“Everyone gets a positive treatment effect, but the ones that are benefiting the most are these lower-educated individuals,” he said, explaining that because GLP-1s directly target appetite and metabolism, they make it easier for people with more time constraints, like those working multiple jobs or of a lower socioeconomic status, who may not have the time to stick to go to a gym or purchase healthier foods.

Researchers simulated the U.S. adult population 25 and up to estimate the lifetime health and economic effects of using GLP-1s for weight loss. They tested life-long pathways for two scenarios: one in which adults did not use GLP-1s, and the other with sustained GLP-1 consumption for adults who met the criteria for obesity—defined as having a BMI above 30.

Using a standard health economics method to classify health improvements and cost savings into dollars, the researchers found that people without college diplomas saved $219,000 to $220,000, while that amount fell for college-educated individuals to $163,000.

Financial barriers to access

Though the 40-50 age group has the highest observed rates of GLP-1 use, the savings compound if people start in their twenties and thirties. The study estimates beginning GLP-1 usage at ages 25 to 30 can save individuals up to $270,800 over the course of their lifetime.

Fatima Cody Stanford, an obesity medicine physician at Massachusetts General Hospital, said while these numbers look promising in abstract, achieving the full extent of health benefits from GLP-1s would require paying at least hundreds of dollars per month “indefinitely.”

“When you pull these medications back, meaning [you] don’t utilize them any longer, patients will have weight regain and re-emergence of the cardiometabolic diseases that they were meant to treat,” Stanford told Fortune.

The average American taking GLP-1s could pay anywhere from about $350 to $450 per month, namely for the GLP-1s approved by the FDA for weight management like Wegovy, according to Stanford. She said that price tag is “outside of reach” for most Americans, meaning those who “might glean the most benefit” from GLP-1s won’t be able to foot the bill. Her numbers align with the $349 to $399 range on TrumpRx for direct-to-consumer purchase, but Wegovy without insurance typically costs $1,350 per month.

Montano-Campos acknowledged the study doesn’t take into account discontinuation of GLP-1 use for financial reasons, since the simulation assumes lifetime access to the drug on a consistent basis.

The NBER study also didn’t account for the high likelihood of discontinuation due to side effects, another factor health plan providers weigh when choosing to cover GLP-1s for obesity. That’s according to Morgan Lee, lead researcher of Pharmaceutical Strategies Group (PSG)’s 2026 survey, which surveyed 237 benefits leaders representing employers, health plans and unions.

“Even if you choose to cover the drug—let’s say you can get the price right and cover it—you also want to make sure that people are staying on the drug long enough and having that continuation, so that they can experience long-term health benefits,” Lee said. Health care providers “want to see long-term return on investment in terms of better health for their members, but they also want to be sure that these are going to be people who are able to then stay on the drug to get to those outcomes to begin with.”

About 75% of health plan providers don’t cover GLP-1s for obesity-related weight loss, according to the PSG survey. Nearly half “indicated they would not cover GLP-1s for obesity at any price,” per the report.

Ultimately, Montano-Campos hopes his study will help lead to increased GLP-1 access for healthcare purposes.

“We hope that it anchors the conversation about access because our findings essentially show that this type of medical innovation compresses health inequality,” he said.

One person familiar with the matter told CoinDesk that xStocks and its distribution partners gathered more than $1 billion in customer orders. But when underwriters finalized allocations, many of those requests went unfilled.

Binance Wallet, Bybit and Bitget Wallet received no shares and canceled their offerings. Meanwhile, customers of Kraken and xStocks received only a fraction of the allocations they requested.

The shortfall wasn’t limited to crypto platforms, though. Data compiled by Access IPOs showed that some retail investors at traditional brokerages received only a portion of the shares they had sought.

An xStocks spokesperson said “overwhelming demand” prevented all orders from being fulfilled and that funds tied to unfilled subscriptions had been returned.

The firm’s tokenized SpaceX stock, trading under the ticker SPCXx, was still launched after the IPO. About $24 million in tokenized shares were circulating onchain at the time of publication, according to Arkham data. Ondo Finance and Dinari, which did not offer pre-IPO access, also launched tokenized SpaceX products following the company’s market debut.

‘Performed as designed’

The episode underscores a key lesson for tokenized assets. Creating a token is easy; securing the underlying asset is crucial.

“What appears to have gone wrong… is that demand significantly exceeded the available supply of underlying shares,” a spokesperson for tokenization platform Dinari said.

“If the underlying stock cannot be sourced, allocated and held within the necessary regulatory framework, there is ultimately no asset to tokenize.”

If you’re thinking about getting a HELOC but have decided to hold off until rates move lower, you could find that what you’ve waited for all along is higher interest rates. According to the CME Group’s FedWatch tool, the probability that the Fed will raise rates grows with each meeting throughout this year. The probability of a June increase is 0%. But look ahead two meetings: the probability rises to 26.5% in September and finally to 41.6% by December.

HELOC and home equity loan rates: Saturday, June 13, 2026

The average HELOC rate is 7.25%, according to real estate analytics firm Curinos. HELOCs first hit a 2026 low of 7.19% in mid-January, then again in March, and again in May. The national average rate on a home equity loan is 7.86%, far from its 2026 low of 7.36%, which we first saw in mid-March, then again at the end of April, and in mid-May.

With mortgage rates remaining around 6%, homeowners with home equity and a low primary mortgage rate may feel frustrated about not being able to access the growing value in their home. A second mortgage in the form of a HELOC or HEL can be a workable solution.

HELOC and home equity loan interest rates: How they work

Home equity interest rates are calculated differently than primary mortgage rates. Second mortgage rates are based on an index rate plus a margin. That index is usually the prime rate, which is currently 6.75%. If a lender added 0.75% as a margin, the HELOC would have a rate of 7.50%.

A home equity loan may have a different margin because it is a fixed-interest product.

Each lender has its own pricing methodology for second-mortgage products, such as a HELOC or home equity loan, so it pays to shop. Your rate will depend on your credit score, the amount of debt you carry, and the amount of your credit line compared to the value of your home.

And average national HELOC rates can include “introductory” rates that may only last for six months or one year. After that, your interest rate will become adjustable, likely beginning at a higher rate.

Again, because a home equity loan has a fixed rate, it’s unlikely to have an introductory “teaser” rate.

An introductory rate will be well below the market rate

The best HELOC lenders offer low fees, a fixed-rate option, and generous credit lines. A HELOC allows you to easily use your home equity in any way and in any amount you choose, up to your credit line limit. Pull some out; pay it back. Repeat.

Look for a lender offering a below-market introductory rate. For example, FourLeaf Credit Union is currently offering a HELOC APR of 5.99% for 12 months on lines up to $500,000. That introductory rate will convert to a variable rate in one year. When shopping for lenders, be aware of both rates.

Also, pay attention to the minimum draw amount of a HELOC. The draw is the amount of money a lender requires you to initially take from your equity.

The best home equity loan lenders may be easier to find, because the fixed rate you earn will last the length of the repayment period. That means just one rate to focus on. And you’re getting a lump sum, so no draw minimums to consider.

And as always, compare fees and the fine print of repayment terms.

What is a good interest rate on a HELOC right now?

Rates vary from one lender to the next — and by where you live. You may see rates from nearly 6% to as much as 18%. It really depends on your creditworthiness and how diligent a shopper you are. The national average for an adjustable-rate HELOC is 7.25%, and for a fixed-rate home equity loan is currently 7.86%. Try to match or beat those rates.

Is it a good idea to get a HELOC right now?

For homeowners with low primary mortgage rates and a significant amount of equity in their house, it’s likely one of the best times to obtain a HELOC or home equity loan. You don’t give up that great mortgage rate, and you can use the cash drawn from your equity for things like home improvements, repairs, and upgrades. Or just about anything else.

What is the monthly payment on a $50,000 home equity line of credit?

If you withdraw the full $50,000 from a line of credit on your home and pay a 7.25% interest rate, for example, your monthly payment during the 10-year HELOC draw period would be about $302. That sounds good, but remember that the rate is usually variable, so it changes periodically, and your payments will increase during the 20-year repayment period. A HELOC essentially becomes a 30-year loan. HELOCs are best if you borrow and repay the balance within a much shorter period.

Pyth Network [PYTH] has joined the growing list of cryptocurrencies battered by heavy capital outflows sweeping the market. In fact, more than $584 billion in value have drained away over the past month, with the same weighing down on some assets harder than others.

PYTH, for its part, carved out a fresh all-time low and slid to roughly $0.04 on 6 June, before staging a 14% rebound. This suggested that investors may be rotating capital back into the asset.

Now, the move may look bullish on the surface, but one question lingers – Is this a sustainable recovery, or a temporary rally set to trap buyers at the top?

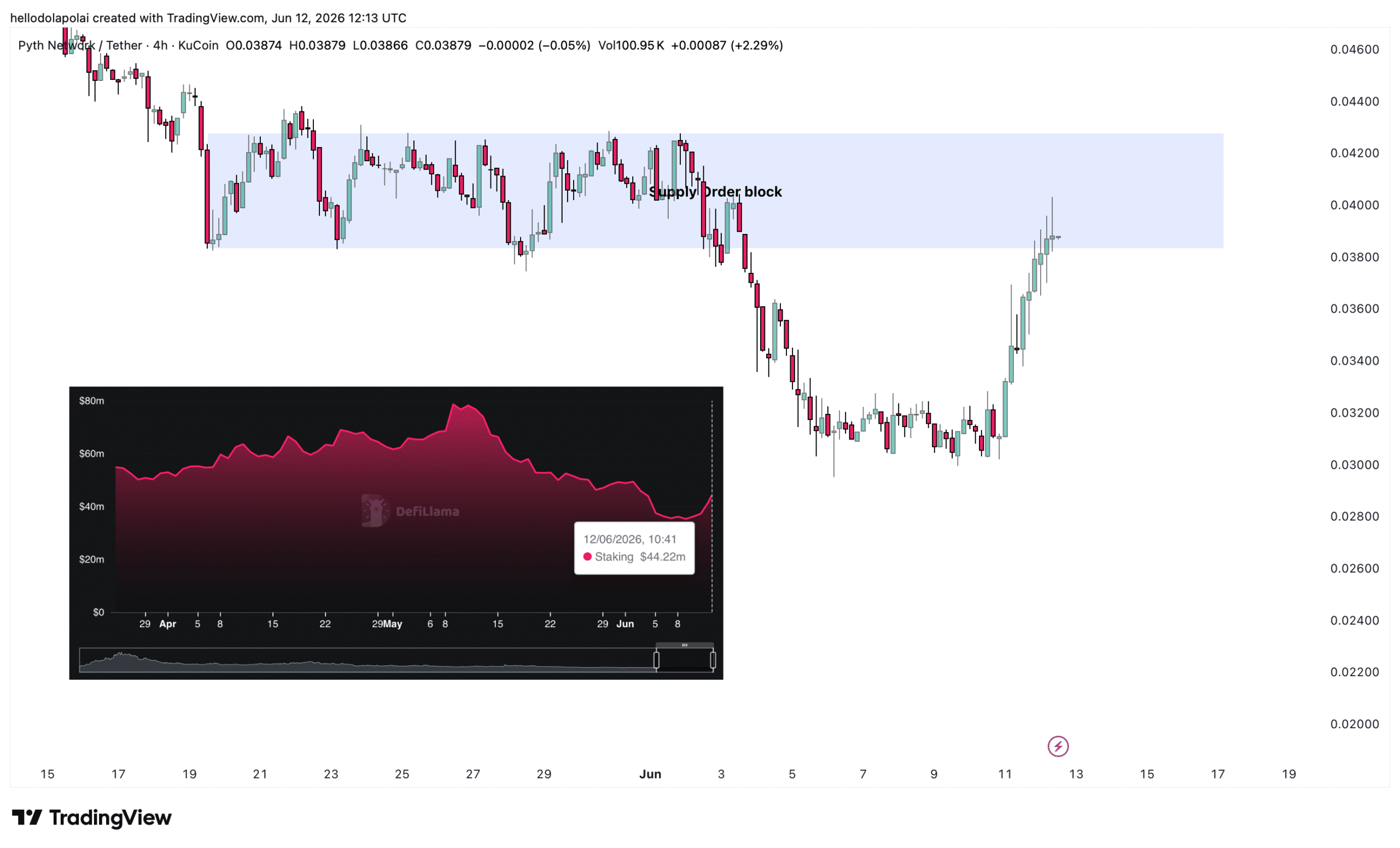

A supply zone threatens to cap PYTH’s rally

A clear hurdle now sits in PYTH’s path as the latest leg of its recovery pushed the price directly into a major supply order block.

Supply blocks mark the zones on a chart where heavy concentrations of sell orders tend to sit, and a move into one of these areas often triggers a price decline.

At the time of writing, sellers were yet to mount an aggressive push lower. This seemed to imply that buyers may be absorbing the supply and defending the level for now.

Source: TradingView

That resilience seemed to track with the fundamentals too as Pyth’s total value staked edged up to $44.22 million – An increase of roughly $8.92 million in the three days since 9 June.

Structure tells only part of the story behind whether PYTH is truly positioned to climb though. Hence, the momentum indicators are worth looking at too.

Momentum indicators reinforce PYTH’s upside

The first indicator behind this bullish case was the Average Directional Index (ADX) – A tool traders rely on to gauge whether a trend is strong. At the time of writing, the ADX hinted at PYTH sitting within a strong bullish environment, leaving the probability for an upswing intact.

The Money Flow Index (MFI), which tracks the inflow and outflow of capital tied to an asset, showed more money moving into PYTH. The indicator had a reading of 57 – Firmly inside the bullish region above 50. This seemed to be a sign that capital has kept flowing into the market.

That’s not all either as volume climbed by 21% to $41 million too. A simultaneous surge in both volume and price often signals growing bullish strength, raising the odds that the upside extends itself.

PYTH’s positive funding rate signals fresh demand

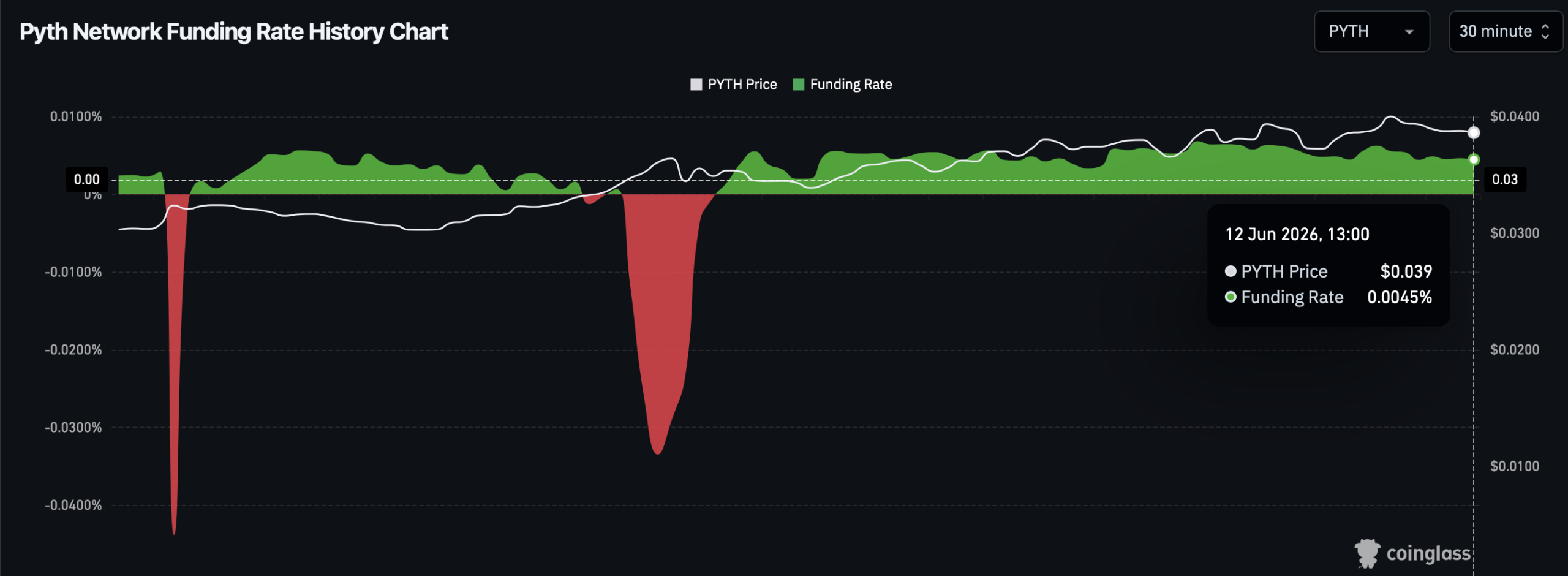

Finally, what strengthens the case for PYTH clearing the resistance barrier is the bullish tone in its perpetual futures market.

According to Coinglass, the average funding rate had a mildly positive reading of 0.0045% at press time.

Source: Coinglass

A positive funding rate, paired with the surge in perpetual capital, implied that fresh money entered the leveraged market and more traders may be positioning themselves for further PYTH upside.

This blend of rising perpetual capital behind a rally that is yet to overheat, a hike in staking, and steady capital inflows leaves PYTH positioned for a sustained move higher.

Final Summary

PYTH rebounded 14% from a record low, a sign that buyers may be stepping back in after a heavy market-wide selloff.

While a wall of sell orders sat above the press time price, rising demand and steady staking suggested the recovery may have room to run.