Pendle [PENDLE] traded under pressure throughout the session and lost more than 10% of its value at press time despite a noticeable increase in market participation. However, trading volume rose by roughly 20% to $36.9 million, showing that traders remained highly active during the decline.

Rising volume during a sell-off often reflects stronger conviction from market participants, and that pattern appeared across PENDLE’s latest move. Rather than attracting follow-through buying, the increased activity accompanied sustained downside pressure.

As a result, sellers maintained control of price action even as liquidity entered the market.

Why PENDLE buyers stayed active despite weakness

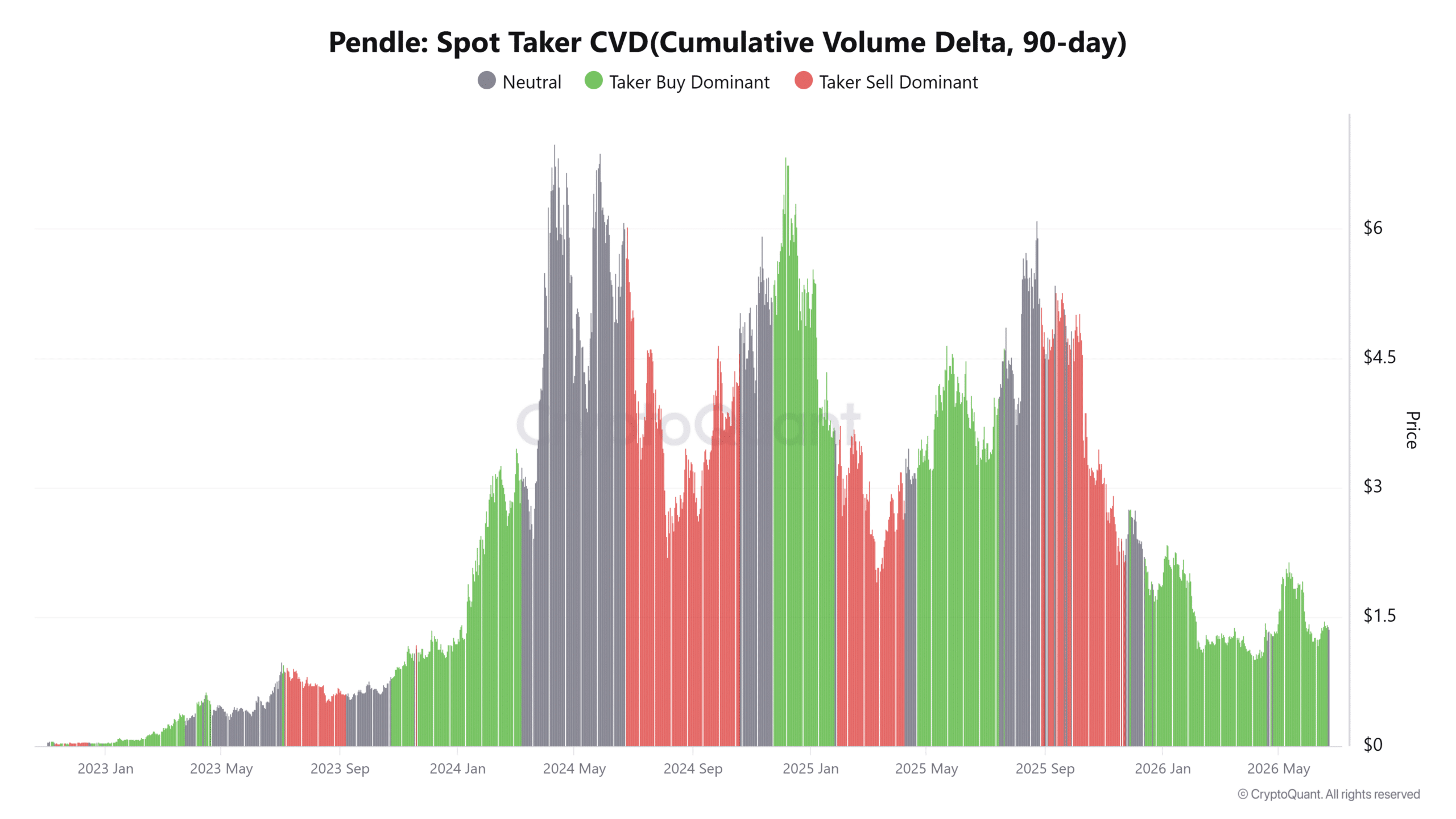

Spot market data revealed a different story beneath the decline. At the time of writing, Spot Taker CVD remained firmly positive and continued trending higher even as PENDLE moved lower. This divergence suggested that aggressive buyers continued entering the market through market orders.

However, their activity failed to translate into immediate price appreciation. Instead, sellers appeared to absorb incoming demand and prevented buyers from regaining control. This imbalance highlighted a market where participation remained healthy but directional conviction remained split.

While buyer aggression persisted, the prevailing supply across the market limited upside progress. If this divergence continues, traders could begin watching for signs that demand eventually overcomes the remaining sell-side pressure.

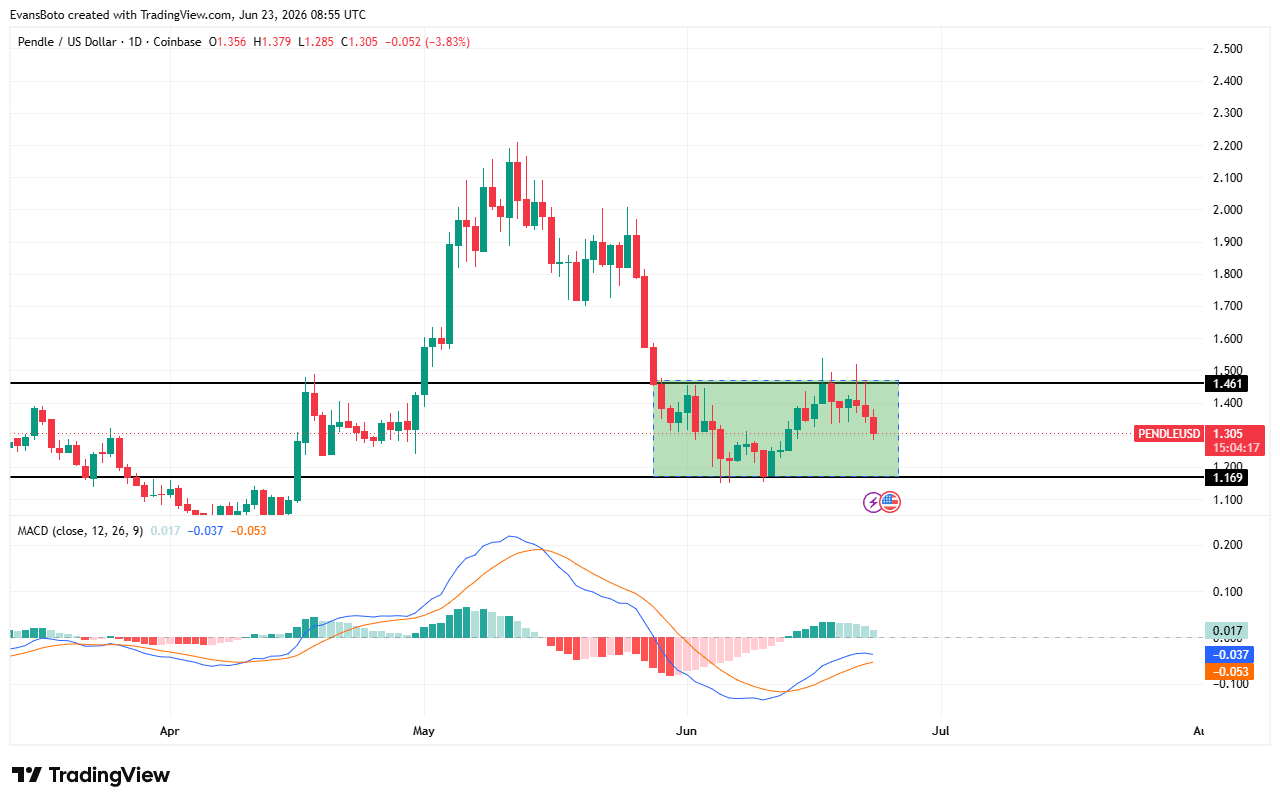

Can PENDLE hold $1.16 as MACD weakens?

PENDLE remained trapped within a well-defined range after its recent decline and continued trading just above the key $1.16 support zone. Buyers repeatedly defended this area, preventing a deeper breakdown despite persistent selling pressure.

However, each rebound attempt lost strength before reaching the upper boundary near $1.40, leaving the asset compressed inside the range. The chart also showed a lower-high structure developing, which reflected fading bullish conviction.

Meanwhile, at press time, the MACD histogram remained negative and the MACD line continued drifting beneath the signal line, confirming that bearish pressure had persisted throughout the latest move. If bulls continue defending $1.16, PENDLE could revisit resistance around $1.40.

However, a loss of this support level could expose the asset to a sharper decline as sellers regain stronger control.

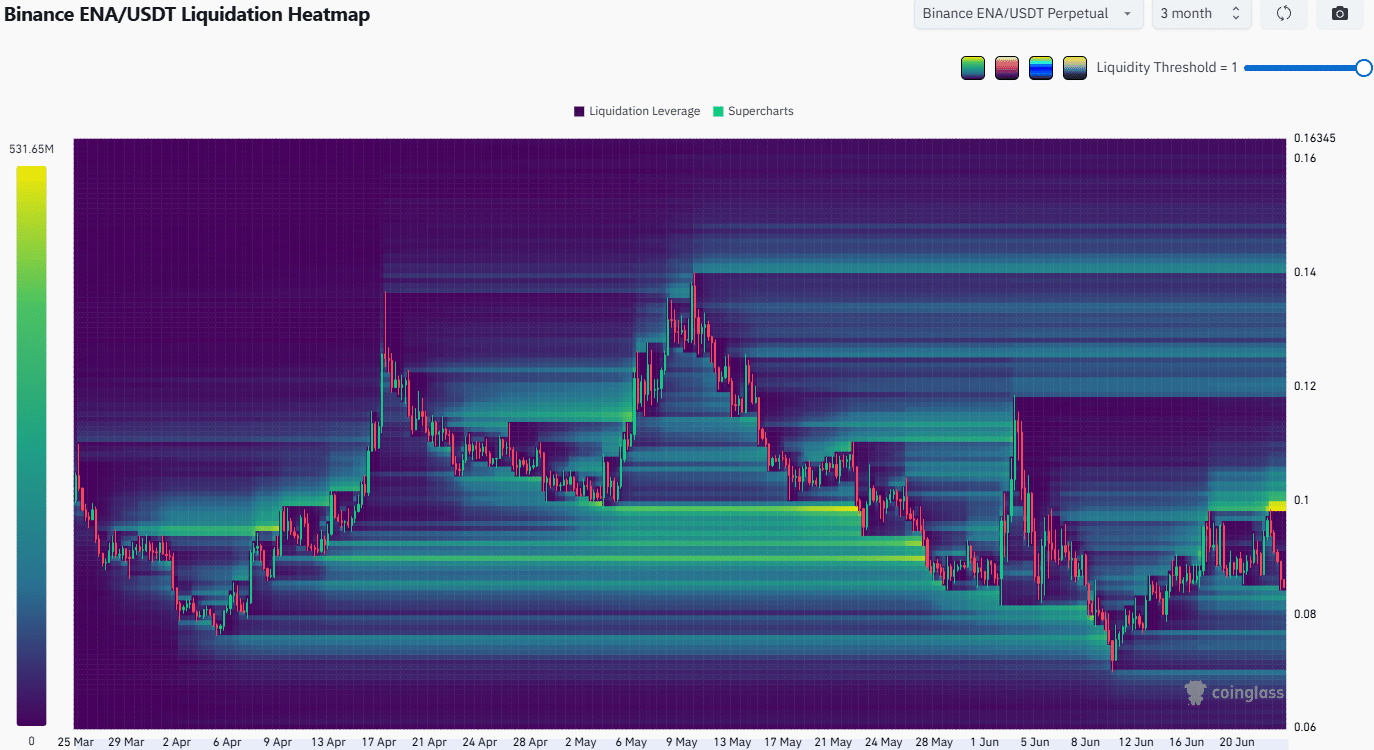

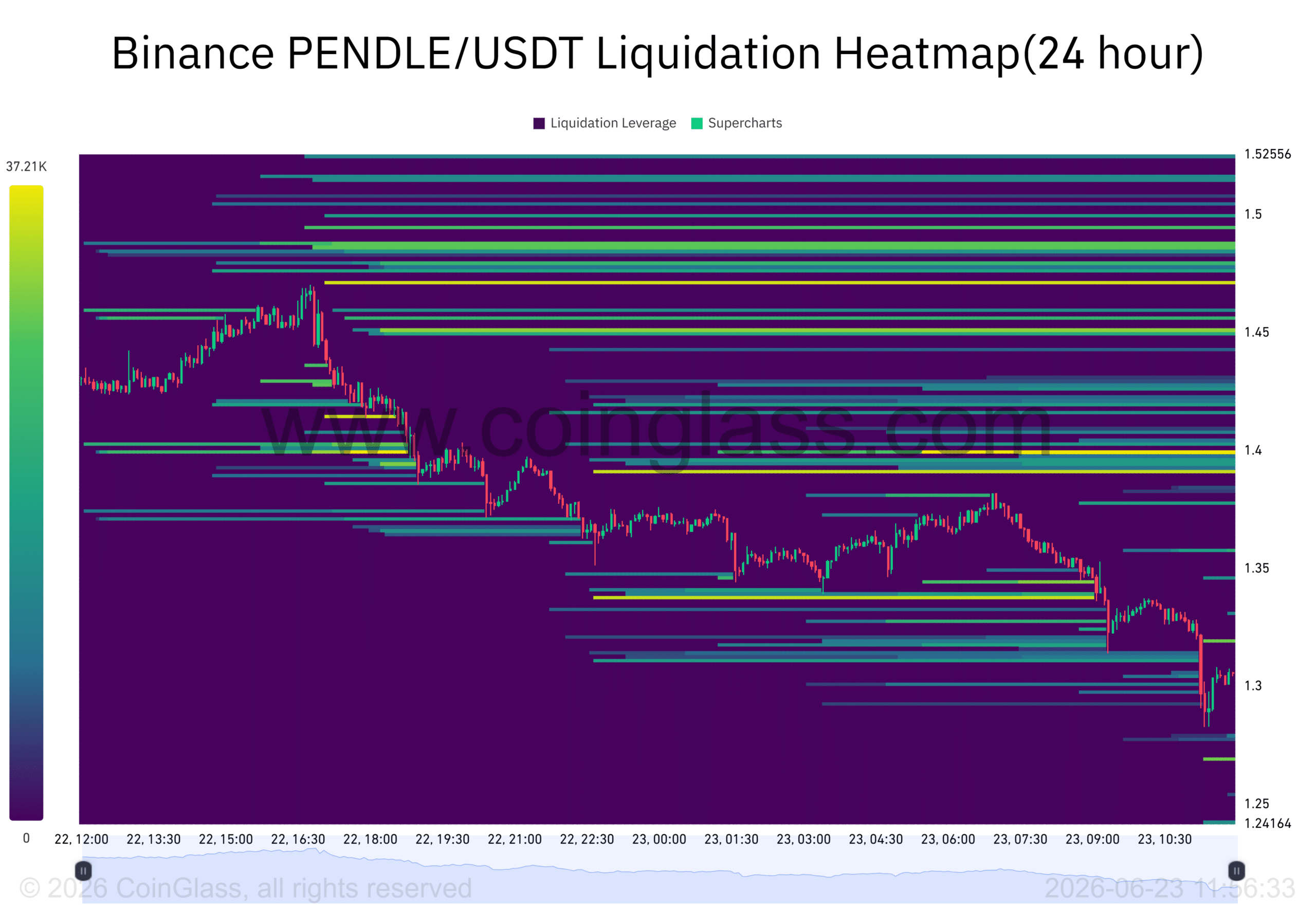

Why does the $1.40–$1.50 zone matter?

Liquidation heatmap showed a clear concentration of leveraged positions above the current market price. The largest liquidity pockets clustered between $1.40 and $1.50, creating an area that could attract price if buyers regain strength.

Markets frequently gravitate toward heavily populated liquidation zones because they contain significant amounts of leveraged exposure. In contrast, liquidity below current levels appeared considerably lighter. This imbalance placed greater attention on the overhead region rather than lower targets.

If PENDLE stages a recovery from support, traders could focus on the $1.40–$1.50 range as a potential destination. Until then, those liquidity clusters remain an important reference point for short-term market participants.

Final Summary

- Buyers remained active, but sellers continued absorbing demand across the market.

- Defending $1.15 remains crucial before any move toward higher liquidity zones.