Ripple Labs is reportedly leading an effort to raise at least $1 billion for a new public-market vehicle that would accumulate XRP, per Bloomberg, testing whether the digital asset treasury trade still works beyond bitcoin.

The raise would be done through a special purpose acquisition company, the report citied to people familiar with the matter. The funds would sit inside a new XRP-focused digital asset treasury, and Ripple is expected to contribute some of its own XRP to the vehicle.

Terms are still under discussion and could change. Ripple did not immediately respond to CoinDesk’s requests for comment or confirmation.

If completed, the deal would be the largest known XRP treasury vehicle to date. XRP is the world’s fifth-largest token, with a market value of about $138 billion. It has gained 13% this year, compared with a 16% rise in bitcoin.

Digital asset treasury companies became one of crypto’s biggest stock-market trades in 2025, as listed firms used SPACs, reverse mergers and equity issuance to buy tokens. The model worked while crypto prices rose and investors paid premiums for balance-sheet exposure.

That trade has weakened, however. Shares of major token accumulators, including Strategy and Metaplanet, have fallen sharply in recent months as crypto prices turned choppy and investors started questioning how many public companies can run the same accumulation play at once.

Ripple’s plan would test whether XRP has enough institutional demand to support a similar structure.

XRP has not drawn the same treasury-company interest as bitcoin. One of the larger examples came in May, when VivoPower announced a $121 million raise to pivot toward XRP investing.

Ripple has its own reasons to back a larger vehicle. The company held 4.74 billion XRP in wallets as of July 31, worth about $11 billion at current prices, according to its website. Another 35.9 billion XRP were locked in on-ledger escrow accounts scheduled for monthly release.

A public XRP treasury company could create a new buyer for the token while giving Ripple another way to place part of its holdings with investors.

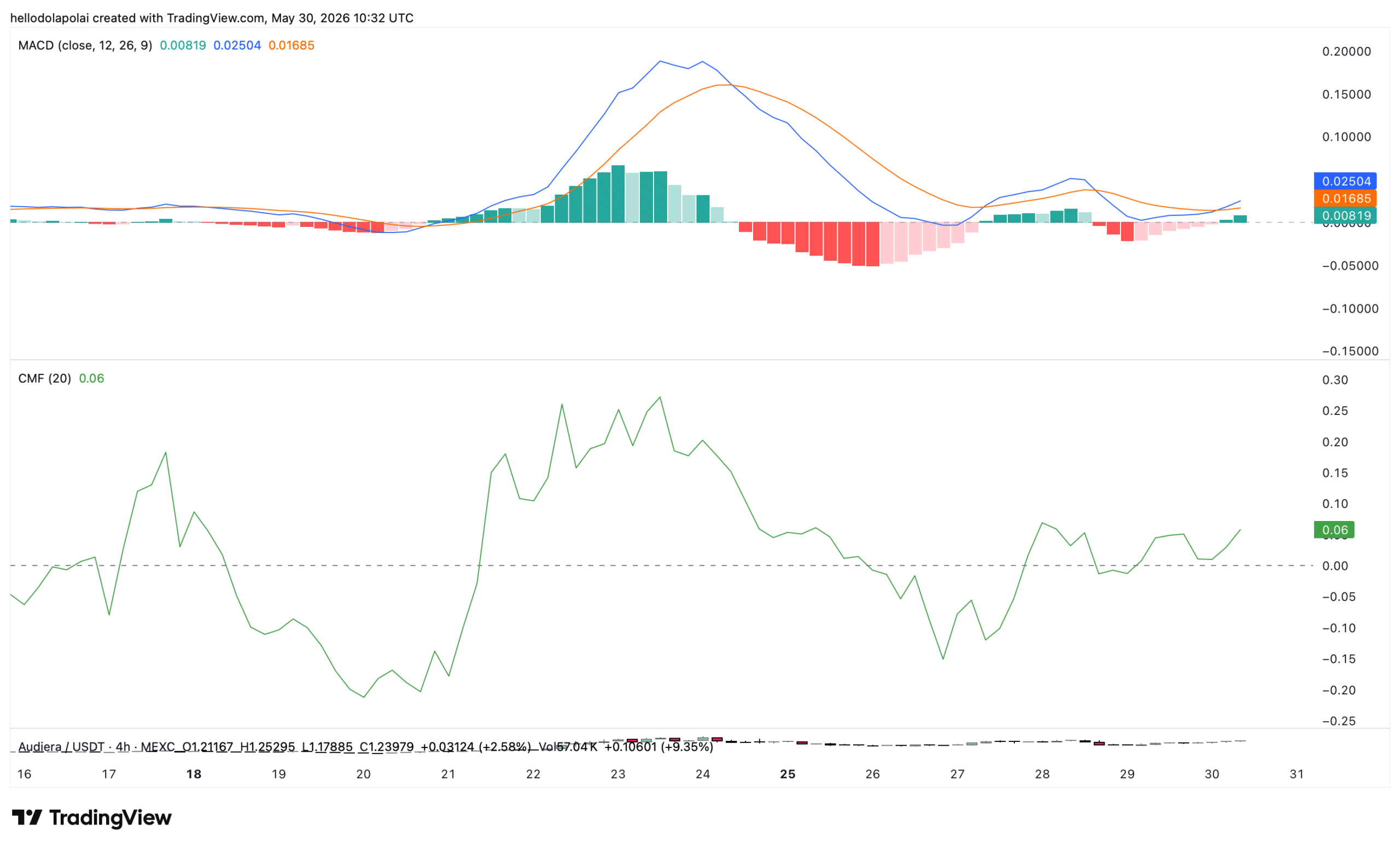

![Why Audiera [BEAT] is THE token to watch out for this weekend](https://moneyvests.com/wp-content/uploads/2026/05/Why-Audiera-BEAT-is-THE-token-to-watch-out-for-696x392.webp "Why-Audiera-BEAT-is-THE-token-to-watch-out-for.webp")