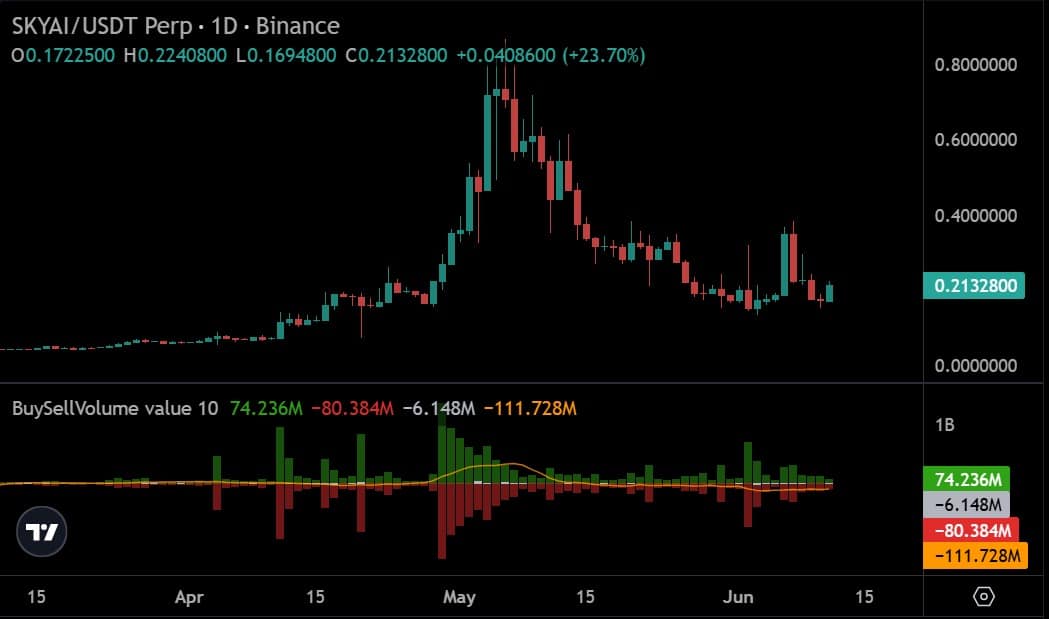

After four consecutive days of losses, SKYAI appeared to find a local bottom. The altcoin rebounded from $0.15, reclaimed $0.20, and reached a local high of $0.22.

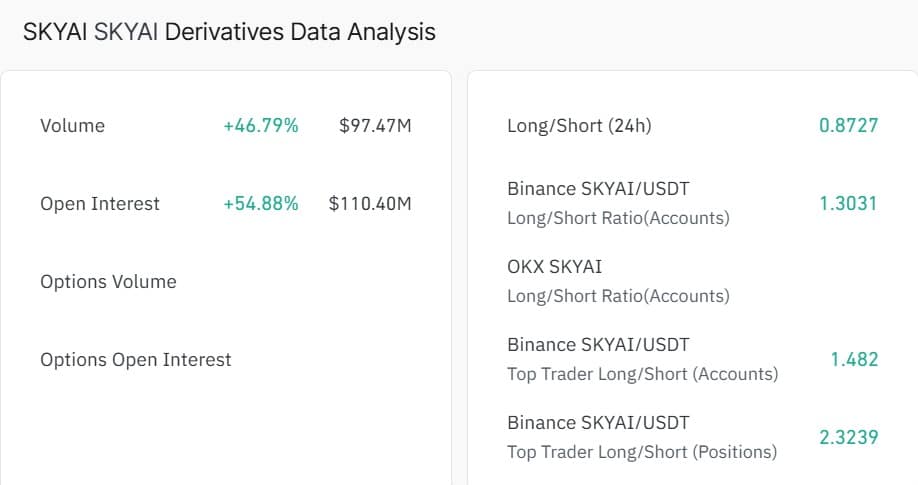

At press time, SKYAI traded at $0.21 after gaining 26% over the past 24 hours. Trading Volume also rose 56% to $88 million, signaling renewed market activity.

The surge in activity encouraged traders to open new positions. Open Interest climbed 54.8% to $110.4 million, while Derivatives Volume rose 46% to $97 million.

Source: CoinGlass

The increase suggested fresh capital entered the market, supporting the latest price recovery.

Are traders still betting against SKYAI?

Despite the rebound, market participants remained cautious. Activity across both Spot and Futures markets suggested many traders used the rally to reduce exposure.

In the Futures market, sellers remained active. On Binance, Perpetual Sell Volume reached 80 million, compared to 74 million in buy volume.

Source: Coinalyze

As a result, Perpetual Netflow fell to negative $6.14 million, while Net Buying remained at negative $111 million.

These readings suggested sellers continued to dominate trading activity.

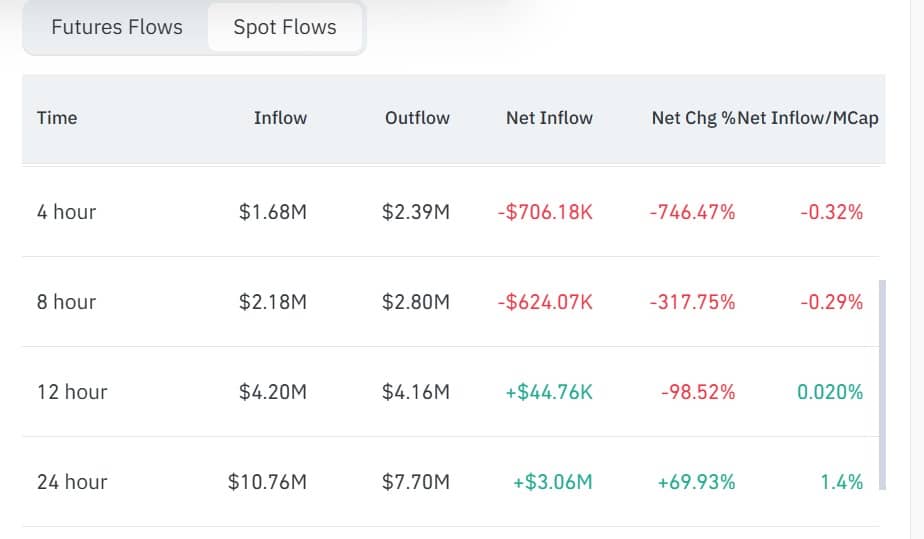

On top of that, profit-taking accelerated in the Spot market. Spot Inflow rose to $10.7 million, while Spot Outflow stood at $7.7 million.

Source: CoinGlass

That pushed Netflow up 69% to $3.06 million. A positive Netflow typically indicates more tokens moved onto exchanges, increasing potential selling pressure.

With sellers active across both Spot and Futures markets, traders appeared unconvinced that the recovery would last.

Can SKYAI extend its rebound?

SKYAI’s price recovered sharply, and derivatives activity strengthened. Even so, technical indicators continued to support the bullish case. The Aroon indicator showed Aroon Up at 71, above Aroon Down at 42.

Source: TradingView

This setup suggested buyers retained control of the short-term trend. The altcoin also moved above its Short-Term Moving Average, reinforcing bullish momentum.

Taken together, these indicators suggested the current recovery could continue.

If buying pressure remains strong, SKYAI could target $0.30 next.

However, renewed selling pressure could trigger another pullback. In that scenario, the altcoin may lose $0.20 support and revisit $0.16.

Final Summary

SKYAI’s rebound attracted fresh traders, but conviction remained surprisingly weak.

Profit-taking increased even as price momentum accelerated higher.

The task force would become the main point of coordination for preventing and investigating the theft of cryptocurrency, which is a problem that plagues the young industry. From fraud and so-called pig butchering by complex criminal networks to state-backed attacks from hackers, digital assets have long been a target. Many of the sector’s most vocal political opponents often cite that undercurrent of criminal abuse as proof the sector is risky for consumers.

Despite $11 billion in thefts and scams last year, “victims have nowhere to turn,” Gottheimer, a New Jersey Democrat, argued. This change would provide “a single federal point of contact.”

This legislative effort suggests that the responses to theft cases have been inconsistent across the jurisdictions, including federal agencies and down through state and local law enforcement.

“By housing a coordinating task force at the Justice Department, this bill gives victims, investigators and local law enforcement the unified federal response they have been missing, all on a voluntary basis that respects local control,” said Dannis Porter, co-founder and CEO of the Satoshi Action Fund that advocates for digital assets policy, in a statement.

Before the arrival of the pro-crypto administration of President Donald Trump, the DOJ had maintained its own National Cryptocurrency Enforcement Team, but the agency quickly disbanded it during the new administration, with new leaders arguing it was regulating the industry through enforcement.

Is EME a good stock to buy? We came across a bullish thesis on EMCOR Group, Inc. on The Wealth Dynasty Report’s Substack. In this article, we will summarize the bulls’ thesis on EME. EMCOR Group, Inc.’s share was trading at $827.78 as of June 9th. EME’s trailing and forward P/E were 27.81 and 28.09 respectively according to Yahoo Finance.

weerasak saeku/Shutterstock.com

EMCOR is a high-quality infrastructure and construction services company benefiting from the AI-driven data center buildout, manufacturing reshoring, and long-term building electrification trends, but despite exceptional fundamentals, its valuation has expanded significantly, leading to a 12–18 month target price of $810 implying roughly 10–11% upside.

The business operates across electrical and mechanical construction, building services, industrial services, and UK operations, with its strongest momentum coming from electrical and mechanical segments tied to hyperscale data center demand.

In 2024, EMCOR delivered record revenue of $14.6 billion, net income of $1.0 billion, operating margins of 9.2%, and diluted EPS of $21.52, supported by 60%+ free cash flow growth to $1.337 billion and strong conversion dynamics. The balance sheet remains highly conservative with near-zero net debt, $841 million in cash, a 1.19x current ratio, and ROE of 37%, reflecting extremely efficient capital deployment.

At current levels, EMCOR trades around 34x trailing and 31x forward earnings versus a long-term historical average closer to 17–18x, reflecting a significant re-rating driven by growth expectations. While backlog stands at a record $10.1 billion and supports double-digit revenue growth near term, long-term returns are expected to normalize as growth moderates and margins stabilize.

Key risks include valuation compression, cyclicality in non-residential construction, labor shortages, tariff exposure, and potential slowdown in AI-driven data center demand, although secular tailwinds remain supportive. Overall, EMCOR remains a high-quality compounder best suited for long-term holders willing to accept a lower margin of safety at current prices levels.

Previously, we covered a bullish thesis on EMCOR Group, Inc. (EME) by CompanyCharts in April 2025, which highlighted undervaluation, strong U.S. infrastructure exposure, and consistent earnings and free cash flow growth. EME’s stock price has appreciated by approximately 116.46% since our coverage. The Wealth Dynasty Report’s Substack shares a similar view but emphasizes on peak valuation and reduced margin of safety despite continued AI-driven construction tailwinds and strong fundamentals.

The phrase “market manipulation” has historically conjured up a specific image – A dark, smoky room filled with traders huddled over phones, whispering insider secrets to skew the market in their favor.

Today, the smoky rooms have been replaced. The perpetrators are no longer humans; they are autonomous AI agents.

Introducing the Machine Perception Layer – A digital era where algorithms trade, reason, and react in microseconds, executing financial orders before a human trader even realizes that something is up.

This isn’t science fiction. It is the new reality of systemic risk, and we’ve already witnessed its devastating potential.

Was the ‘Oracle Loop‘ behind October’s flash crash?

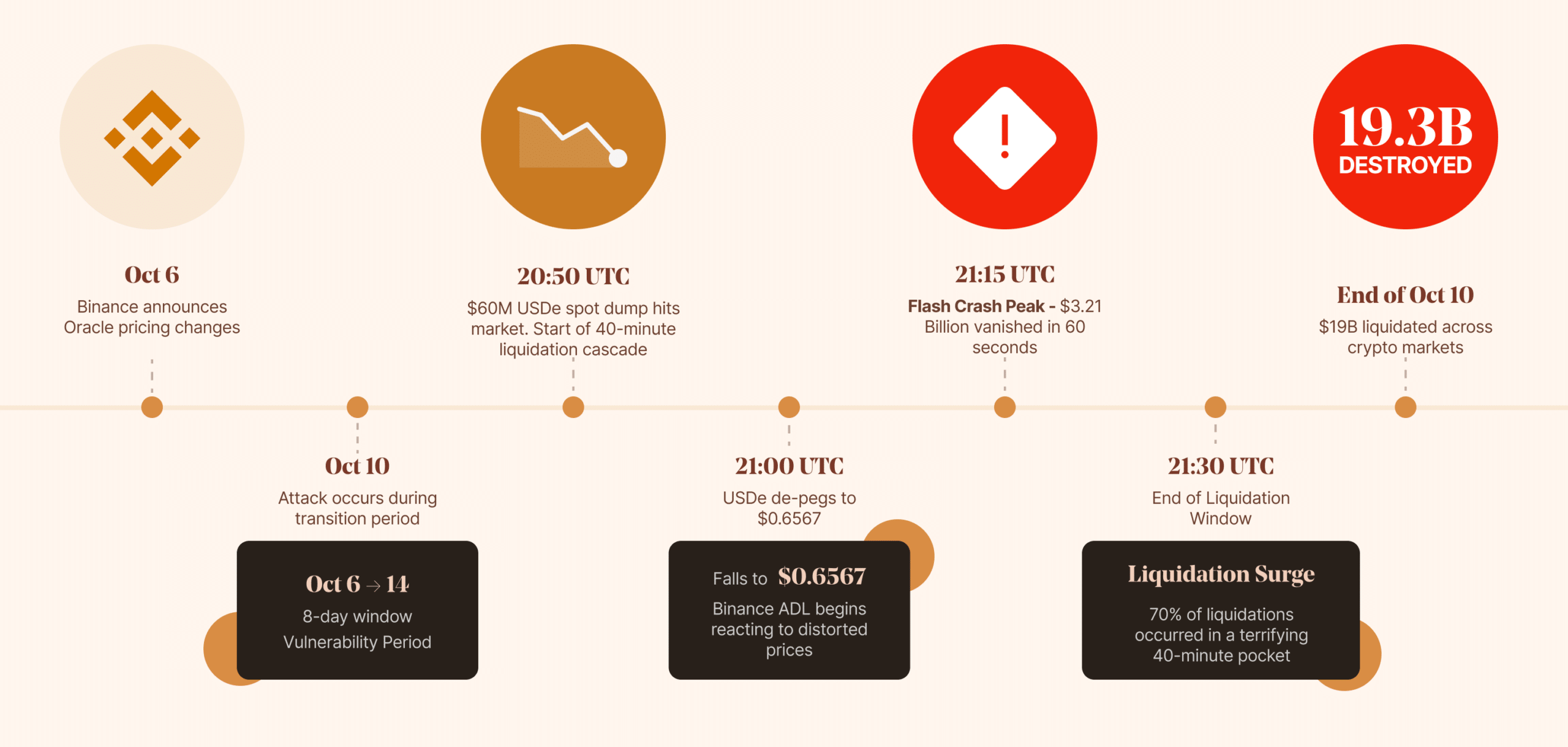

On an unassuming Tuesday, the 10th of October, at exactly 21:15 UTC, $3.21 billion vanished in 60 seconds. Over the course of that day, the crypto market saw a historic $19 billion in liquidations.

70% of the liquidations were violently compressed into a terrifying 40-minute pocket between 20:50 and 21:30 UTC. So, what caused the collapse?

At its heart was a structural vulnerability known as the “Oracle Loop.” On the 6th of October, Binance announced oracle pricing updates on the 14th. This created an 8-day “vulnerability window” while the system was in transition.

The attack happened on the 10th of October, bang in the middle of this period.

Surprisingly, the initial “hack” was just a spot dump of $60 million in the synthetic dollar USDe, causing it to de-peg and reach $0.6567.

However, Binance’s Automatic Deleveraging (ADL) judged the value of the sell-off by only looking at the exchange’s internal order books to price USDe, wBETH, and BNSOL, instead of the broader market.

Timeline of the October 2025 flash crash | Source: AMBCrypto

The ADL started clearing out bankrupt, over-leveraged accounts at any available price. Meanwhile, market makers couldn’t get their orders through, causing the buy side of the order book to simply cease.

The system liquidated $19.3 billion based on a phantom price that existed nowhere else in the world.

This caused a wipeout of funds across all platforms that relied on Binance’s ADL.

Panic selling emerged, marking prices down to near-zero levels. For example, the native token of Cosmos [ATOM] collapsed from $4 down to $0.001 on Binance.

Why crypto is ground zero

TradFi has always had market pauses. It has regulations, human oversight, and a “close” at the end of the day, with weekends off. Crypto, in comparison, is a 24/7 network of independent blockchains.

According to Nic Puckrin, macro analyst and founder of Coin Bureau,

If there’s a sharp price move on one venue, it tends to spread to all the others with the help of arbitrage bots, shared collateral, and price oracles. So you get the liquidation cascades that are common in crypto, with no tools in place to trigger a pause in selling.

The ground reality is extremely chaotic too. Thousands of independent, highly specialized bots run on blockchains like Solana or Binance with one simple goal – Make profits, decrease losses, and do not stop trading.

For Nikita Prokopenko, Executive Legal Associate at SBSB FinTech Lawyers, the “real issue” is data. Speaking to AMBCrypto, she said,

Market makers used bots even before the AI age. The real issue is the data AI takes on. If the data is analyzed poorly, it can trigger a sequence of non-grounded trades, leading to pump-and-dump schemes. This is the real risk.

Let’s take Solana’s Hive Mind, for example. In early 2026, autonomous AI agents accounted for over 70% of all transaction volume on Solana DEXs, especially during peak token launches.

These are not unified corporate entities though. They are thousands of fragmented bots built on open-source frameworks like ElizaOS and Valory’s Olas. They scrape social media sentiment, analyze on-chain liquidity, and execute trades in fractions of a second.

However, there may be a workaround here. According to Puckrin,

The key is not trusting any single price source. It’s also important to have automatic safeguards that kick in when conditions deteriorate: Leverage limits that tighten as liquidity thins, and kill switches that halt activity when prices move abnormally fast.

Of late, AI agents have been making their way into prediction markets as well. Most famously, the Polystrat agent, deployed on the decentralized prediction protocol Polymarket via the Olas network, executed over 4,200 independent trades.

In fact, it captured astonishing returns of over 370% in its first month alone!

You CANNOT regulate math!

After the dust settled post the October 2025 liquidation event, critics scrambled to find an explanation. However, the uncomfortable truth is that AI agents simply did what they were asked to do.

They flawlessly processed orders, checked for risk, and sold because they were meant to protect profits.

Who is to blame then? Well, Puckrin believes that,

Fines and bans can’t be aimed at the code itself. They have to be aimed at whoever is actually allowing the bot. The fact that crypto is code-based doesn’t automatically make accountability disappear.

The $19 billion wipeout wasn’t a crime. It was a flawless, systemic realization of “game theory.” When autonomous agents are programmed with the same rules of self-preservation, they create a collective monster.

Ultimately, AI operates strictly on prompts and mathematics—and as Wall Street and Silicon Valley are quickly learning, you cannot contain, penalize, or regulate math.

Final Summary

October 2025’s flash crash was a result of AI bots misreading crypto signals, causing $19 billion in liquidations.

AI agents taking over crypto trading in 2026 leaves the industry open to vulnerabilities.

Banks are focusing on pulling stablecoins and tokenized forms of more traditional financial instruments into one integrated package to meet growing institutional demand for multi-asset flexibility.

Rather than waiting for a single winner to emerge, large asset managers and corporate treasuries are demanding a multi-instrument setup in which stablecoins, tokenized bank deposits and tokenized money market funds all run on the same infrastructure.

“The demand from institutional clients is consistent: they are not waiting for any single instrument to prevail,” Thomas Eichenberger, chief strategy officer and deputy group CEO at Swiss-based digital asset bank Sygnum, told CoinDesk on Thursday in an email.

“They are asking how tokenized deposits, regulated stablecoins, and tokenized money market funds can be combined and made interoperable, so a treasury function can move between them — permissioned settlement, 24/7 cross-border flows, yield with on-demand liquidity — under one regulatory framework they already trust,” he added.

Sygnum, which describes itself as the world’s first digital assets bank, partnered late last year with Swiss banking powerhouse UBS and PostFinance, a subsidiary company of the state-owned Swiss Post, to test blockchain payments between institutions on Ethereum.

OpenAI, the company behind ChatGPT, is jumping into the mega-IPO stock-trading race, filing a confidential S-1 with the Securities and Exchange Commission. With SpaceX at bat for a Friday opening and Anthropic on deck, OpenAI is in the queue but has not set a date for its debut.

“We have not decided on timing yet; it may be a while because there are things we want to do that are likely easier as a private company,” OpenAI said in a statement posted on its website. “But it’s a complicated set of trade-offs, and this gives us the option to go public sooner if that ends up being best.”

It may feel as if OpenAI burst onto the tech scene overnight, but the company’s roots as a nonprofit date back to 2015, when it introduced itself as an artificial intelligence research company. It aimed to “advance digital intelligence in the way that is most likely to benefit humanity as a whole, unconstrained by a need to generate financial return.”

Recently valued at roughly $852 billion and potentially seeking a public valuation of $1 trillion or more, a publicly traded OpenAI would likely face pressure from investors to deliver strong financial returns.

Here are six things to know before you buy OpenAI once it goes public.

1. Is the IPO market getting crowded?

With OpenAI, SpaceX, and Anthropic all expected to premiere within a relatively short period, investors may wonder whether the market is becoming oversaturated with big-name equity bets. Deutsche Bank chief global strategist Bankim Chadha told Yahoo Finance that the S&P 500 has absorbed large IPOs in the past without difficulty.

“It sounds like very compelling logic that these huge IPOs would suck out all the liquidity, and then crowd out all the other stocks,” Chadha said. “Take a look at how the S&P 500 behaved during waves of issuance around big IPOs, as we’re talking about now. When the market is very strong, issuance then picks up, and the market basically remains strong.”

2. Can OpenAI monetize ChatGPT?

Consumers’ growing subscription overload may be a barrier to monetizing ChatGPT. Currently, subscription prices range from free with limited access to $100 per month for power users. Out of an estimated 800 million users, only 5% pay, according to the Financial Times.

OpenAI has experimented with pay-per-click ads within ChatGPT query results. Forrester Research found that AI users are “generally sensitive to ads blurring the line between helpful information and paid promotion.” Users are also wary of personal information being tapped without their permission. However, a majority of those polled (83%) said they would be willing to tolerate the ads in exchange for a free service.

3. The AI boom comes with a massive price tag

Data centers may not be popular with the “not in my backyard” crowd, but perhaps more importantly, they aren’t cheap either. OpenAI has said it plans to spend $115 billion by 2029, mostly on data centers, to support its AI infrastructure.

And then you have to train the AI models, at an estimated cost of nearly $125 billion by 2028, and again in 2029. By 2030, those training costs will dip below $100 billion (but not by much), according to the Wall Street Journal.

4. OpenAI hasn’t made a profit so far

Despite explosive growth, OpenAI hasn’t made a profit to date.

Reports indicate that the company could generate roughly $30 billion in revenue during 2026, while still posting an estimated $14 billion loss that year. Total losses could reach $44 billion before OpenAI turns a profit in 2029.

Under its current “capped-profit” business structure, OpenAI will have to transition from its opaque, quasi-nonprofit heritage to a fully transparent, publicly traded, for-profit company. Anthropic, with its ChatGPT nemesis Claude — which has also filed for a future IPO — will be a primary and formidable competitor.

5. You can buy the stock before the IPO

As with other pre-IPO offerings, private-market stock previously held by investors, employees, and other insiders is available in the secondary market. For example, ARK funds hold OpenAI in exchange-traded funds, including the ARK Innovation ETF (ARKK) and the Next Generation Internet ETF (ARKW).

Shares may also be available on secondary marketplaces such as Forge. However, you must be an accredited investor to purchase these shares, with a net worth of $1 million or more (excluding your home) and an income of at least $200,000 individually or $300,000 jointly.

6. OpenAI will likely be a part of index funds

If your broker doesn’t offer the OpenAI IPO (and we don’t yet know which brokers those are), you can eventually gain exposure to the stock by purchasing it once it trades publicly — or through an index fund, though which index (S&P 500, Nasdaq) is also not yet known.

When the Buffalo Bills open their $2.2 billion Highmark Stadium this September, they’ll be opening the NFL’s smallest venue: 60,108 seats, down from the 71,608 the old stadium held. And to make that happen, New York State and Erie County paid $850 million in public funds, resulting in 11,500 fewer seats, with personal seat licenses (the mechanism allowing holders the right to buy season tickets) running as high as $50,000 per seat. Get-in prices on opening night have already listed at $663 on the resale market.

The stadium was built, in significant part, with the money of the fans being priced out of it. New York State contributed $600 million; Erie County contributed $250 million, which collectively is the largest public subsidy ever committed to an NFL facility. But the Bills Mafia’s new stadium isn’t unique in this funding: In deal after deal across American sports, it’s the same playbook in which the public funds a venue, and the owner uses it to serve a wealthier, smaller crowd.

‘Market rates’ to blame

On the first day the FIFA World Cup opened, FIFA President Gianni Infantino held a press conference in Mexico City and offered this defense of his tournament’s sky-high ticket prices: “If we are doing something wrong, everyone in North America is doing something wrong.” It was his more forward argument following his comments at the Milken conference in April, in which he blamed the U.S. market’s design for encouraging these exorbitant prices. “We have to look at the market—we are in the market in which entertainment is the most developed in the world, so we have to apply market rates.”

Between 1970 and 2020, state and local governments spent $33 billion in public funds on major-league sports arenas across the U.S. and Canada—with the median public contribution covering 73% of construction costs. That number has only accelerated: In 2024 alone, more than $13 billion in taxpayer subsidies were proposed by teams across professional sports for new construction and renovations.

“No one has ever built a new stadium and provided more affordable tickets after that new stadium has opened,” said Victor Matheson, a professor of economics at the College of the Holy Cross who has studied sports subsidies for nearly 30 years. “It’s, in fact, exactly the opposite.”

The shrinking stadium

Individual teams in most leagues don’t have to share revenue from premium seats and luxury boxes with the rest of their league—while TV and merchandise revenue is pooled. That incentive pushes every owner in the same direction: Rip out the cheap seats, build suites, constrain supply, and extract maximum value from the fans with the deepest pockets.

Average NFL ticket prices nearly tripled from 2015 to 2025, up 173% after adjusting for inflation. The new Chiefs stadium is expected to have roughly 15% fewer seats than Arrowhead. New stadiums across the NFL, NBA, and MLB consistently follow the same pattern: fewer general seats, more luxury suites, higher prices throughout.

“The money is in super premium experiences, not in actually putting people in the seats,” Matheson told Fortune. “The old model was: Build an 85,000-seat stadium and sell cheap bleacher tickets and hopefully they buy some peanuts and Cracker Jack. That’s not the way anyone sells things anymore.”

“We make stadiums and arenas smaller, but we make them nicer,” Matheson continued. “You tear out a bunch of bleacher seats, and you put in a box with a handful of seats but a super-premium experience, because you can make a lot more money on a few seats to the right people than a lot of seats to the working class.”

The incentive structure reinforces itself: Teams don’t have to share premium revenue with the league, making it the one revenue stream they can maximize entirely on their own terms.

FIFA raised prices on more than 90 of the 104 World Cup matches between October 2025 and April 2026, with the three main ticket categories rising an average of 34%. FIFA claims it received 500 million requests for the 7 million World Cup tickets on offer. Infantino offered 130,000 tickets at $60—out of a total of six to seven million—and called it the “right thing to do.” The Football Supporters Europe coalition filed a formal complaint accusing FIFA of abusing its monopoly position. The New York and New Jersey attorneys general subpoenaed FIFA over alleged seat-location misrepresentation and artificial price inflation.

Taxpayer dollars at auction

The stadium subsidy race has a direct parallel in the broader economy in terms of cities competing with each other using public money to offer companies better tax incentives and bring their businesses there.

In 2018, Amazon solicited bids from 238 cities for its second headquarters. New Jersey offered $7 billion if Amazon located in Newark. Maryland pledged $8.5 billion. New York ultimately offered $3.5 billion in tax incentives—less than half of Newark’s package, yet Amazon still chose New York. Amazon executives said the decision was based primarily on where employees wanted to live, not on incentives, meaning Newark’s $7 billion was never really in the running, and eventually, New York pulled out of the deal due to community opposition.

Economists say these cities, already with the structural advantages to win regardless, are essentially throwing money into the void because these companies and stadium owners were always going to pick them. Buffalo was never realistically going to lose the Bills. The $850 million was, in effect, a ransom paid to prevent a departure that was never truly on the table.

We’re seeing an auction play out with data centers. States have been offering hundreds of millions in tax breaks to attract the AI infrastructure boom, and the costs are exploding beyond any projection. Ohio’s data center tax exemption, initially projected to cost $136 million in fiscal 2025, came in at nearly $1.6 billion—more than 11 times the estimate. The state has since suspended the program. Illinois followed, with Gov. JB Pritzker pausing data center tax incentives after the legislature failed to make facilities pay for their own electricity costs, arguing as one of many voices in the debate that the buildings bring few jobs relative to their footprint, consume enormous power and water, and face growing community opposition.

A hidden market problem

Judd Kessler, a professor of business economics at the Wharton School and author of Lucky by Design, said the stadium subsidy dynamic is a hidden market failure at the structural level. When public money builds a venue that an owner then deliberately constrains and ups the amenities and premiums, the taxpayer is funding the creation of a scarcity they will personally be priced out of. When venues price below what the full market would bear, the surplus moves sideways into bots, queues, and resale platforms. And when there, between 25 and 35% gets extracted in fees on every transaction.

“We as customers and fans should look at those fees and be annoyed by them,” Kessler told Fortune, “the same way—potentially even more so—than we are annoyed by very high initial ticket prices.” That fee structure was central to the Ticketmaster-Live Nation antitrust case, in which a jury ruled in April that Live Nation held an illegal monopoly over the live events industry. It’s one reason, Kessler argues, innovation in ticket market design has stalled: too many players in the system profit from the opacity.

The pattern surfaced in sharp relief at Madison Square Garden this week. Mayor Zohran Mamdani paid close to $1,000 for a standing-room-only ticket to Game 3 of the NBA Finals while simultaneously announcing a free watch party for 5,000 fans at Bryant Park who couldn’t afford to attend. The same dynamic played out in Central Park on Monday, where the state of New York spent $6 million to host a free watch party for 50,000 residents who cannot afford a World Cup ticket at MetLife Stadium less than 10 miles away across the river.

The return that never comes

Every new stadium deal is sold with some version of the same promise: jobs, tourism, civic pride, economic revitalization. The economic literature is nearly unanimous that those promises don’t materialize. A 2017 survey found 80% of economists believe the costs of stadium subsidies outweigh the benefits.

“This profit-maximizing concept, when you’re simultaneously asking for handouts from regular taxpayers, is appalling,” Matheson said. “Asking blue-collar workers to pay higher taxes so the wealthy and upper-middle class can go see games in shiny new stadiums is absolutely one of the worst pieces of public policy out there.”