The dollar index (DXY00) is moving lower today and is down by -0.28%. Today’s -3% plunge in WTI crude oil prices has lowered inflation expectations and could prompt the Fed to pursue easier monetary policy, a bearish factor for the dollar. Also, lower T-note yields today weaken the dollar’s interest rate differential and are negative for the dollar.

The dollar recovered from its worst level today on better-than-expected US economic news. The Apr trade deficit eased to -$55.9 billion from -$56.6 billion in Mar, narrower than the -$56.1 billion expected. Also, May existing home sales rose +3.2% m/m to a 5-month high of 4.17 million, stronger than expectations of 4.07 million.

More News from Barchart

President Trump today predicted a swift end to the war with Iran and a subsequent fall in oil prices, and said, “We’re in the final throes of what will be a very, very good deal, and that they could have at least an idea one or two days from now” about the deal.

The swaps markets are discounting the odds at +3% for a +25 bp rate cut hike at the next FOMC meeting on June 16-17.

EUR/USD (^EURUSD) today is up by +0.29%. The euro is moving higher today amid a weaker dollar. Also, an as-expected increase in German Apr industrial production and better-than-expected German Apr trade news are supportive for the euro. In addition, today’s -3% fall in crude oil prices is positive for the Eurozone economy and the euro as Europe imports most of its energy.

German Apr industrial production rose +0.4% m/m, right on expectations and the biggest increase in five months.

German trade news was better than expected as Apr exports unexpectedly rose +0.9% m/m, stronger than expectations of a-0.5% m/m decline. Also, Apr imports unexpectedly rose +1.2% m/m versus expectations of a -2.0% m/m decline.

The markets are discounting a +100% chance for a +25 bp rate hike by the ECB at Thursday’s policy meeting.

USD/JPY (^USDJPY) today is up by +0.02%. The yen is slightly lower today after a +2% rally in the Nikkei Stock Index curbed safe-haven demand for the yen. Losses in the yen are limited amid today’s -3% decline in crude oil prices, which is positive for Japan’s economy and the yen as Japan imports more than 90% of its energy. Also, today’s hawkish report from Nikkei is bullish for the yen as it stated the BOJ is set to raise its policy rate by 25 bp to 1.00% at next week’s policy meeting.

Japan May machine tool orders rose +37.4% y/y, the eleventh consecutive monthly increase.

The markets are discounting a +95% chance of a +25 bp BOJ rate hike at the next policy meeting on June 16.

August COMEX gold (GCQ26) today is down -19.20 (-0.44%), and July COMEX silver (SIN26) is down -0.940 (-1.37%).

Gold and silver prices gave up an early advance today and moved lower on the stronger-than-expected US May existing home sales report, which is hawkish for Fed policy. Today’s strength in equity markets has also reduced safe-haven demand for precious metals. In addition, today’s hawkish report from the Nikkei is bearish for precious metals as it stated the BOJ is set to raise its policy rate by 25 bp to 1.00% at next week’s policy meeting.

Precious metals found support today from a weaker dollar. Also, today’s -3% decline in crude oil prices eased inflation expectations and could prompt the world’s central banks to pursue easier monetary policies, a bullish factor for precious metals. In addition, precious metals still have safe-haven support amid the ongoing US-Iran war.

Silver prices garnered some support from today’s better-than-expected China May trade news, a sign of economic strength that supports industrial metals demand. China May exports rose +19.4% y/y, stronger than expectations of +15.0% y/y. Also, May imports rose +27.4% y/y, stronger than expectations of +26.0% y/y.

Recent fund liquidation of precious metals is bearish for prices, as long holdings in gold ETFs fell to a 5.5-month low on March 31 after climbing to a 3.5-year high on February 27. Also, long holdings in silver ETFs fell to a 10-month low on Monday after rising to a 3.5-year high on December 23.

Strong central bank demand for gold is supportive of gold prices, following news that bullion held in China’s PBOC reserves rose by +320,000 ounces to 74.96 million troy ounces in May, the largest monthly increase in 17 months, and the nineteenth consecutive month the PBOC has boosted its gold reserves.

On the date of publication, Rich Asplund did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

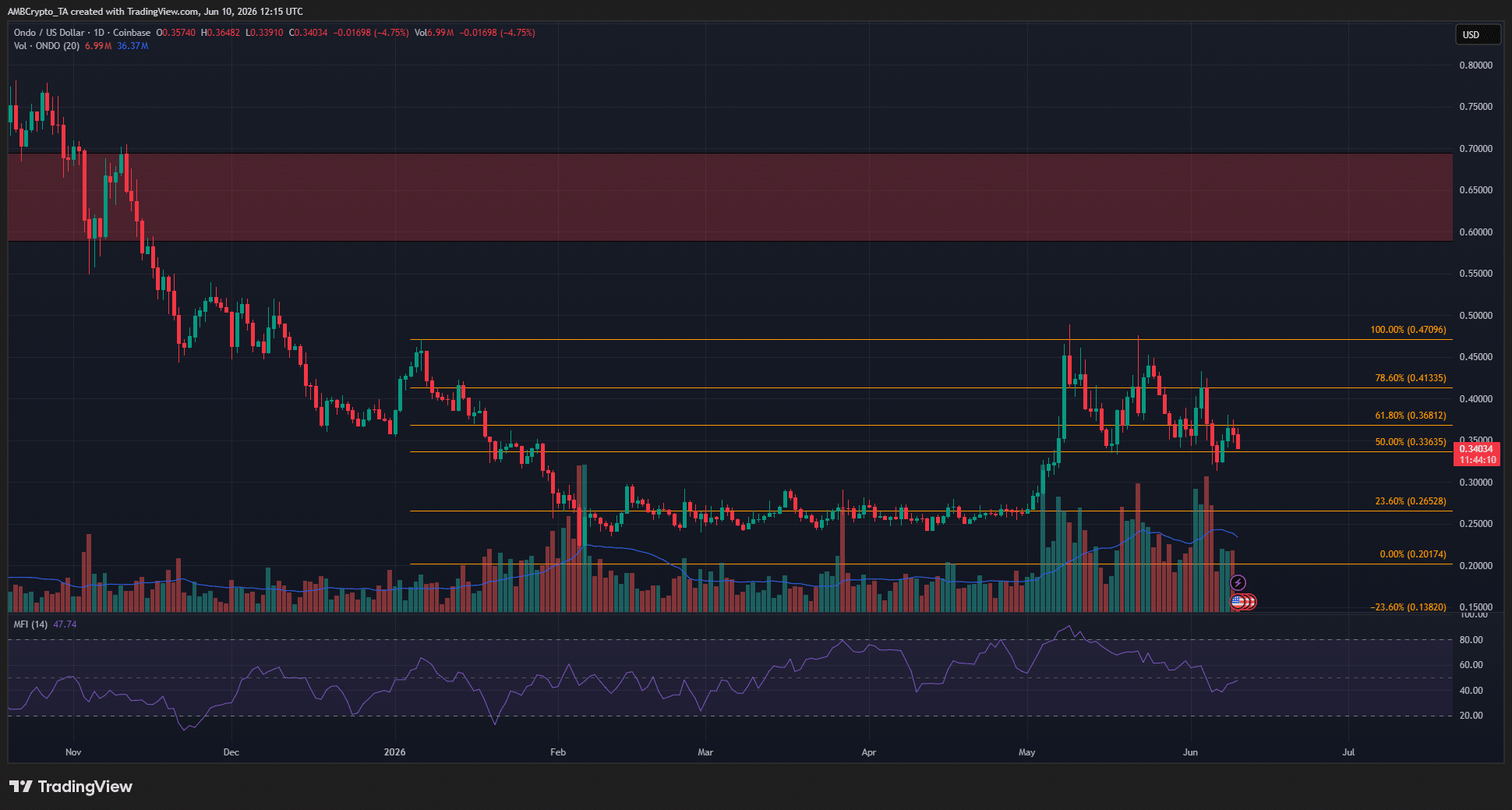

Ondo [ONDO] rallied strongly in early May to challenge the swing high at $0.47 but has since retraced back to $0.34. It was down 5.5% in the past 24 hours and just over 16.9% in the previous week of trading.

The Ondo token losses came alongside a rapid Bitcoin [BTC] sell-off. The extreme selling and fearful market conditions could see both ONDO and BTC fall lower.

The bearish ONDO case

Source: ONDO/USDT on TradingView

Throughout 2026, the higher timeframe swing structure of ONDO has been bearish. The Bitcoin rally beyond $80k in May helped the altcoin sentiment.

The news and the growing RWA narrative around that time helped boost ONDO prices to a local high of $0.451, but the altcoin didn’t manage a daily session close above the $0.47 swing high from January.

The subsequent rejection and the losses over the past month highlighted how the bearish trend was intact. It also signaled that further losses can be expected, especially as the lower timeframe demand zone from $0.335 to $0.350 has been broken.

Traders’ call to action – Sell

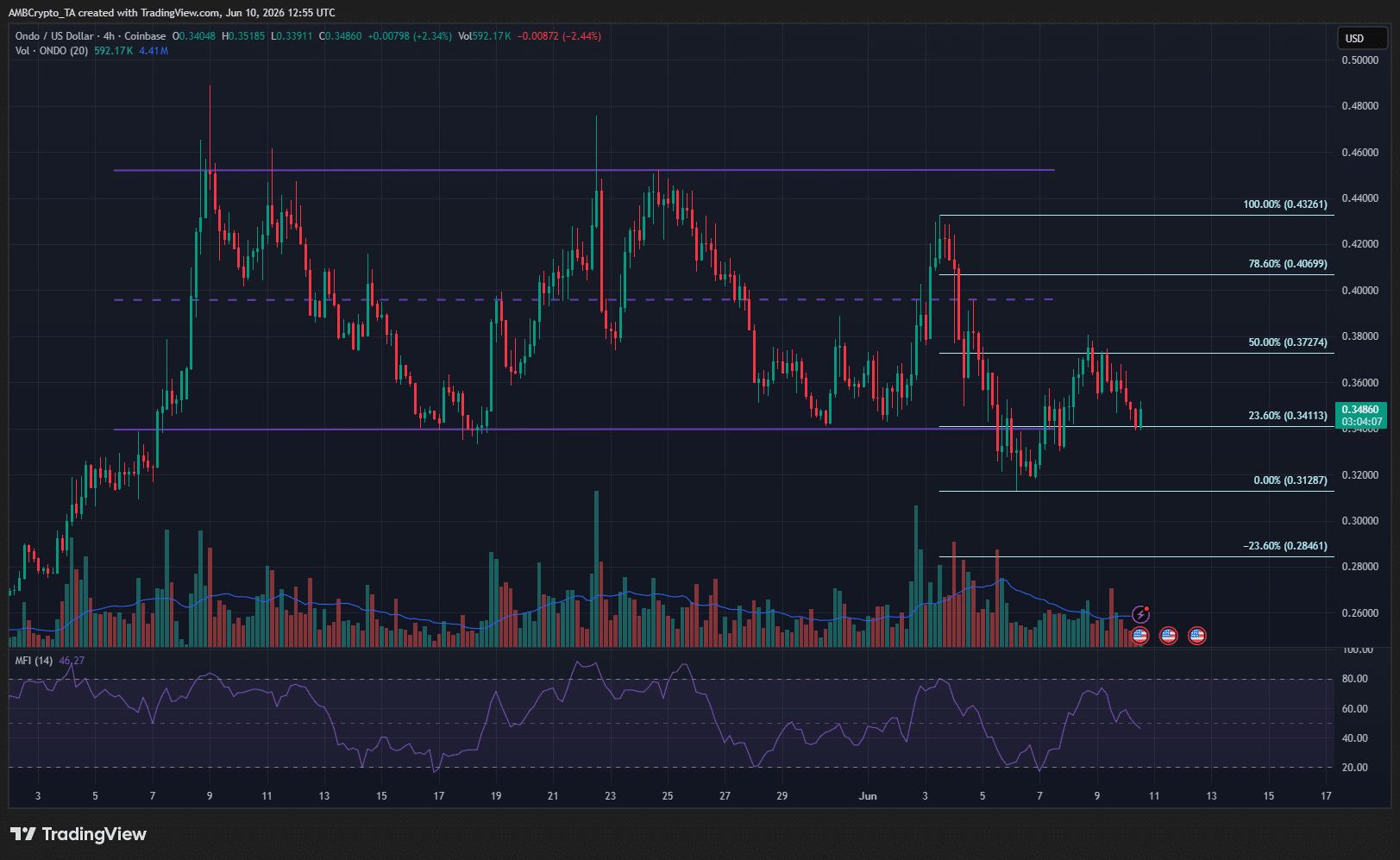

Source: ONDO/USDT on TradingView

The short-term range over the past month between $0.34 and $0.45 was breached to the downside. The H4 structure had turned bearish, and the bounce to $0.372 has reversed.

The MFI on this timeframe was in the process of falling below 50 to signal increased capital outflows and downward momentum.

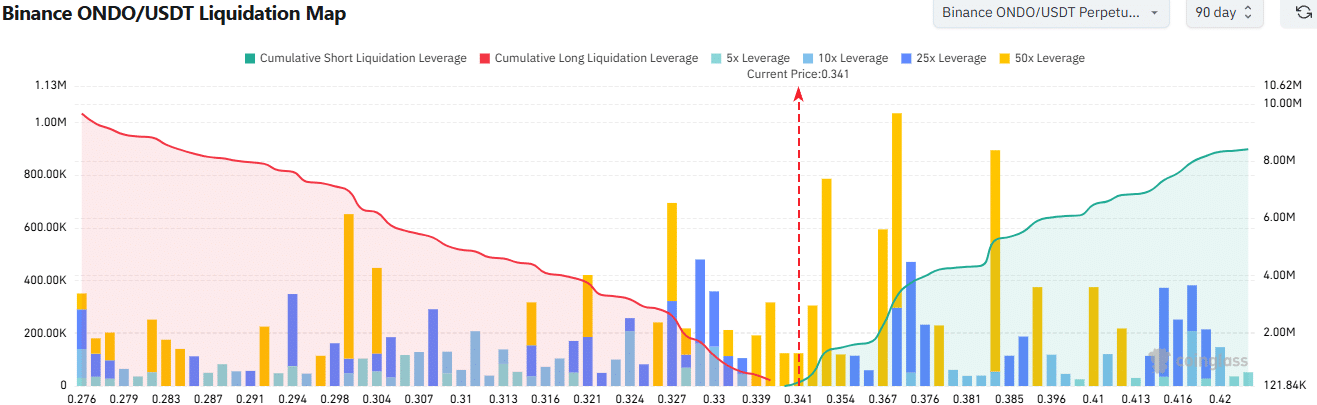

Source: CoinGlass

The liquidation map of the past three months showed that the $0.31-$0.34 area had relatively high cumulative long leverage. A bounce to $0.376-$0.385 was possible, but a dive toward $0.31 was likely to occur soon afterward.

Therefore, traders can position themselves bearishly but leave space for a short-term liquidation hunt to the upside.

A sustained move beyond $0.432 would break the 4-hour structure bullishly, invalidating the bearish short-term bias.

Final Summary

The Ondo rally in May challenged local highs, but demand was not enough to flip the long-term downtrend.

A bounce from the short-term range low at $0.34 is possible, but the momentum favored the sellers.

Texas is shifting from courting data centers toward regulating them.

Gov. Greg Abbott has proposed new rules for data centers as concerns about their energy and water consumption and their impact on utility prices spur complaints in communities across the US.

“The rapid scale of data center development requires oversight to ensure everyday Texans are not burdened with the costs of infrastructure driven by data center expansion,” Abbott, a Republican, wrote in a letter to state regulators on Wednesday.

Abbott said he would work with the state legislature to pass a number of measures, including requiring data centers to pay for their own electric infrastructure, requiring new data centers to use water-efficient technology, and repealing sales tax exemptions for data centers.

The letter also directs state regulators to start working to ensure data centers pay for their own electric infrastructure, ensure data center interconnections result in lower residential electricity bills, and use their power to protect Texas residents.

The proposed regulations are notable in a pro-business state that hosts data centers owned by Big Tech companies from Tesla to Meta to Amazon. Texas has the second-most data centers of any state, behind only Virginia.

BYOE — Bring Your Own Electricity

Backlash to data center development has grown across the US, with protests in local communities and proposed statewide bans in at least 12 states.

Gabriel Collins, an energy and environmental regulatory affairs fellow at Rice University’s Baker Institute, said the proposed regulations in Texas are unlike efforts to pause data center development in other states.

Williams said the message he thinks Abbott is trying to send is “Texas is open for business, but be ready to bring your own electricity and be prepared to invest in local water systems.”

“They want to make sure that the companies with the big balance sheets bear the significant share of whatever the impacts may be,” he said.

Collins also said the issue of addressing data centers is largely bipartisan, a relative rarity in Texas, which could partly explain why Abbott is signaling state lawmakers to focus on it, adding there’s a pretty good shot they can get “reasonable guardrails” passed.

Texas approved a statewide sales tax break for data centers back in 2013. The Texas Tribune reported that the state gives data centers over $1 billion in tax breaks every year.

In November, Abbott called Texas “the epicenter of AI development” during a joint announcement with Google of a $40 billion investment in the state, which included new data centers.

Last week, I shared something with CoinDesk that I want to sit with a little longer. A few minutes in an interview didn’t do it justice. My suggestion is that anyone building in DeFi should think of themselves as a financial asset manager who happens to write code, rather than as a software team that handles money.

A few people pushed back, so let me take one step further: the thing institutions really want from us has almost nothing to do with the code. They want to answer an age-old question: “When something goes wrong, who picks up the phone?”

So far, the answer has been nobody. The code is law: no company, no jurisdiction and no name on the door. For a while, we pushed that as the unique selling proposition (USP), and I understand the appeal. “Trust the contract, not the human” can feel like the safer bet, but if you spend time with a risk committee, you’ll see how strange it sounds to them.

They don’t underwrite code; they assess people and processes. They want to know who signed off, who can move funds, what happens at 3am when a key is compromised and whose responsibility it is to have considered those risks. If you hand them a brilliant protocol written by an anonymous team, with a multi-signature wallet (multisig) controlled by a group of people who have never met each other, the committee will not view it as an innovation. Instead, they will see it as an operational risk they can’t yet price.

And here’s where I’ve landed: the accountability they’re asking for is what lets decentralisation grow up. You get to keep the openness, the composability and the permissionless rails — all of it — while still answering the basic questions any serious financial steward should be able to address.

What does that look like in practice? It means having reserves you can verify in real time, allowing anyone to check solvency rather than relying on assertions in a blog post or press release. It includes controls to ensure that no single person can move significant amounts of money alone, because that’s standard practice in well-run institutions (and it should embarrass us that most protocols don’t adhere to this). None of this is a big ask; it’s the bare minimum.

I get the skepticism. People might say this is how you compromise on the speed that makes crypto alluring. I see it differently, though. Moving fast on what you build is a gift, whereas moving fast with other people’s money (with no one willing to be accountable for it) isn’t speed, it’s just risk waiting for a deadline. April showed us some of those deadlines, and there will be more.

The audience for getting this right has already changed. The institutions everyone keeps waiting for aren’t on their way. They’re already here, managing real money on these rails right now while half the industry debates whether they belong. The platforms that win in the next few years will be the ones that can include a Galaxy or Susquehanna alongside someone opening their first wallet in Lagos. Both should have the same access and the same protections, and both should know who is accountable when it counts.

That’s the bar I want us to be measured against, and I want it set higher than the banks — not on the same level. Not because regulators are coming, although they are. The harder question is whether we’ll build it ourselves or wait for someone else to force our hand.

Principled Perspectives

The centuries-old structure solving bitcoin’s yield problem

Bitcoin holders face a dilemma: how do you preserve ownership through market stress without being forced into actions that destroy long-term value? The answer is not another “crypto yield wrapper”. As bitcoin BTC$61,608.96 adoption matures, a centuries-old financial structure is emerging as a compelling alternative: reinsurance.

BTC is currently trading well below its 2025 highs, and the drawdown is testing conviction across the investor spectrum. The investors who build lasting wealth are not those who predict bottoms or avoid drawdowns; they are the ones who can hold through corrections without being forced to sell. That requires a way to generate income from a long-term bitcoin position without relying on bitcoin’s price direction.

Why the traditional bitcoin yield playbook fails when you need it most

Most yield offerings fall into two buckets: options strategies that monetize volatility, and lending platforms that rehypothecate assets. Both tend to break precisely when stress arrives. Options strategies expose holders to path dependency, volatility regime shifts and counterparty risk, with yield that vanishes when margin calls hit. Lending platforms can be worse: bitcoin disappears into opaque collateral chains, and when liquidity dries up, so does the capital behind it.

Reinsurance is a different source of yield entirely

Reinsurance is insurance for insurance companies, allowing primary insurers to transfer portions of their risk portfolio to limit exposure to large-scale events. These contracts operate independently of financial markets, creating a structurally different return profile that combines underwriting profits with conservative leverage, a time-tested approach that predates cryptocurrency by centuries.

The key insight is that reinsurance returns are driven by real-world risk selection and pricing rather than bitcoin’s price direction. Hurricane risk in Florida does not care if bitcoin is trading at $40,000 or $100,000. This creates historically low correlation to both crypto markets and public equity beta with genuine diversification, rather than repackaging the same underlying exposures.

The mechanics

The structure is simple: post bitcoin as capital in a regulated (re)insurance vehicle, write USD-denominated policies and collect premiums in dollars. Reserves are held in cash and cash equivalents, using standard trust and custody mechanics, keeping the bitcoin ring-fenced as capital, not rehypothecated. Reinsurance is structurally advantaged here. BTC remains in institutional-grade custody within a corporate structure with legal segregation intended to isolate different investors’ assets, with investors able to have 24/7 on-chain proof of their bitcoin capital. This preserves the core objective: maintaining BTC exposure for long-term appreciation, while generating dollar cash flows from uncorrelated reinsurance premiums.

Why institutions should consider reinsurance

Recent 13F filings suggest that long-duration institutional investors are not all running for the exit. Select endowments, public pension plans and sovereign wealth-backed investors have added or maintained bitcoin ETF exposure through the drawdown, underscoring that sophisticated allocators are increasingly treating regulated bitcoin exposure as a long-term portfolio position rather than a purely tactical trade.

But staying the course is easier to justify when a bitcoin position can produce cash flow without depending on price appreciation alone. Reinsurance operates within established regulatory perimeters, supported by actuarial discipline, underwriting controls and capital adequacy standards. For institutions thinking in decades, that distinction matters. The objective is not to chase incremental yield by taking on more crypto-native risk. It is to keep bitcoin exposure intact, earn dollar-denominated income from an independent risk pool and reduce the likelihood that market stress forces a sale at precisely the wrong time.

Headlines of the week

By Helene Braun

A dormant Satoshi-era bitcoin wallet moved after 14 years as the owner became the target of a $285 billion lawsuit, with notice served through Bitcoin’s blockchain; institutional investors continued pulling money from bitcoin ETFs even as BTC revisited the $60,000 level that attracted buyers earlier this year; and DFG CEO James Wo, who built a billion-dollar crypto investment firm from a $20 million family-backed start, said he remains bullish on bitcoin while questioning some of the market’s most aggressive ether price forecasts.

Chart of the Week

Hyperliquid’s 70% rally: what drove HYPE from $40 to $75 in six weeks

HYPE ran from ~$44 to an ATH of $75.52 in six weeks (early May to June 3), as spot ETF launches from Bitwise and 21Shares drove over $130 million; the ATH broke on June 2–3 as TD Securities published the first major bank report documenting Hyperliquid beating CME to oil price discovery, with Grayscale’s HYPG ETF launching the same day.

Listen. Read. Watch. Engage.

Listen:$3 billion leaves Bitcoin ETFs. Why Wall Street isn’t panicking. Jennifer Sanasie is joined by David LaValle to unpack a $2.97 billion outflow streak from Bitcoin ETFs, Bloomberg’s Eric Balchunas explains why the recent outflows may be more noise than signal and Stellar Development Foundation CEO Denelle Dixon discusses DTCC’s decision to select Stellar.

Read: In “Crypto for Advisors”, Beth Haddock reviews the three due diligence questions advisors should be asking in 2026. Then, Aaron Brogan reviews the GENIUS Act implementation timeline and how things will change once it’s here.

Watch: “I will not vote for CLARITY until we address ethics.” Senator Angela Alsobrooks joins CoinDesk Policy Protocol hosts Rebecca Rettig and Renato Mariotti to discuss the three outstanding issues she needs resolved before voting the CLARITY Act off the Senate floor.

Engage: The CoinDesk: Policy & Regulation event is heading back to Washington, D.C. on September 24. This one-day event connects law makers with chief legal officers, compliance officers and policy experts to discuss the future of digital asset industry standards.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

And for a limited time, you can get even more with an elevated welcome bonus on a new Capital One cash-back card:

These welcome offers can help pad your summer budget or give you a headstart on saving for back-to-school season.

Capital One Savor Cash Rewards Credit Card

Annual fee

$0

Welcome offer

For a limited time, earn a one-time $250 cash bonus once you spend $500 on purchases within the first 3 months from account opening

Introductory APR

0% intro APR on purchases and balance transfers for 12 months, then variable 18.49% – 28.49% APR

Purchase APR

18.49% – 28.49% variable

Rewards rate

8% cash back on Capital One Entertainment purchases

5% cash back on hotels, vacation rentals and rental cars booked through Capital One Travel

3% cash back on dining, entertainment, popular streaming services, and at grocery stores (excluding superstores like Walmart and Target)

1% cash back on all other purchases

Benefits

Generous intro APR on purchases and balance transfers for the first 12 months

No foreign transaction fees

The Capital One Savor is one of our favorite cash-back credit cards, thanks to its excellent everyday rewards for no annual fee. In addition to those bonus rewards, you can use the introductory 0% APR to pay down existing debt with a balance transfer or delay interest charges on new purchases.

This is also a solid travel card. Not only can you earn rewards on eligible travel bookings through Capital One Travel, but you’ll pay no foreign transaction fees for international purchases. Plus, you can still earn rewards on dining and entertainment spending while traveling, just like you would at home.

Capital One Savor Student Cash Rewards Credit Card

Rewards rate

8% cash back on Capital One Entertainment purchases

5% cash back on hotels, vacation rentals, and rental cars booked through Capital One Travel

3% cash back on dining, entertainment, popular streaming services, and at grocery stores (excluding superstores like Walmart and Target)

1% cash back on all other purchases

Like the regular Savor card, the Capital One Savor Student card is a great option for earning cash rewards on your regular spending. You’ll earn the same 3% cash back on everyday purchases like dining out, streaming services, and groceries — and even pay no foreign transaction fees on your purchases abroad.

But while you’ll need good credit to qualify for a Savor card, this version is more accessible for students who don’t yet have a solid credit history. You can use your Savor Student card to make purchases and build your credit in school, and even keep it after graduation to continue earning cash-back rewards.

Capital One Quicksilver Student Cash Rewards Credit Card

The Capital One Quicksilver Student is another option for college students. This card makes it even easier to earn cash back on your spending with a standard 1.5% cash back on every purchase, no matter what you buy. That means you’ll get the same 1.5% back on everything from dining at restaurants and buying school supplies at the campus bookstore to filling up at the gas station.

Like the Savor Student, this card can help you build your credit history while you’re in school, since you don’t need a strong credit history to qualify. Once you graduate, you can continue using the Quicksilver for 1.5% back on everything you buy.

We already rank the regular Capital One Savor among our top cash-back cards, but the Savor Student and Quicksilver Student also have a lot to offer for students. And they’re only more valuable with the current elevated welcome offer.

Incoming students can benefit from opening a student credit card early, too. According to Capital One, you can qualify for the Savor Student or Quicksilver Student if you’re admitted and planning to enroll in an accredited university, community college, or other higher education institution within the next three months. So if you’re starting in the fall, you can still qualify over the summer.

If you’re deciding between the Savor or Quicksilver cards, take a look at your regular spending habits. If you make a lot of purchases outside of the Savor’s 3% bonus categories, you may get more value from the Quicksilver’s flat 1.5% cash back. Otherwise, the Savor may help you save more on the purchases you make most often.

However, make sure you’re prepared to take on the responsibility of using a credit card before you apply. Student cards are a great way to build credit, but you’ll need to pay your bill on time and in full every month to maintain a good credit score and avoid high-interest debt. Even student cards carry very high APRs that can add up quickly if you spend more than you can afford.

Editorial Disclosure: The information in this article has not been reviewed or approved by any advertiser. All opinions belong solely to Yahoo Finance and are not those of any other entity. The details on financial products, including card rates and fees, are accurate as of the publish date. All products or services are presented without warranty. Check the bank’s website for the most current information. This site doesn’t include all currently available offers. Credit score alone does not guarantee or imply approval for any financial product.

Talks on ethics provisions in the crypto market structure bill, the CLARITY Act, are reportedly “rocky.”

According to a former FOX Business reporter, Eleanor Terrett, Democrats have disagreed with Republicans on a previous ethics deal.

A Dem source familiar with a bipartisan meeting between Senate lawmakers today described ethics negotiations as ‘rocky,’ citing what they characterized as an ‘about-face’ by GOP members and the White House on an agreement they say had previously been reached.

According to the source, the State Attorneys General (AGs) were to be allowed to sue the federal Department of Justice (DoJ) if it fails to implement the ethics provisions. Additionally, the deal would allow actions to be taken even against members of Congress.

According to Republicans, the deal was flagged by their members who were initially not part of the earlier ethics discussions.

Will ethics stall CLARITY Act?

The ethics issue is primarily aimed at blocking President Donald Trump’s massive conflict of interest in the crypto sector. But it also seeks to prevent other members of the administration from having business interests in the sector.

Trump’s family’s massive interest in DeFi project World Liberty Financials (WLFI), stablecoin (USD1), Bitcoin mining, and other verticals has been widely flagged by Democrats in the past.

In fact, Trump’s crypto profit topped $3B in the past year, while retail investors holding his tokens lost $4B.

For the bill to pass the Senate floor vote, Republicans must secure some Democratic votes. But some of the pro-crypto Democrats have previously warned of not supporting the bill if ethics provisions aren’t addressed.

In short, this could be a key deal breaker. But it remains whether a compromise will be reached before the floor vote.

Industry pushes for developer protections in CLARITY Act

Earlier in the week, over 200 crypto firms urged the Senate to pass the CLARITY Act.

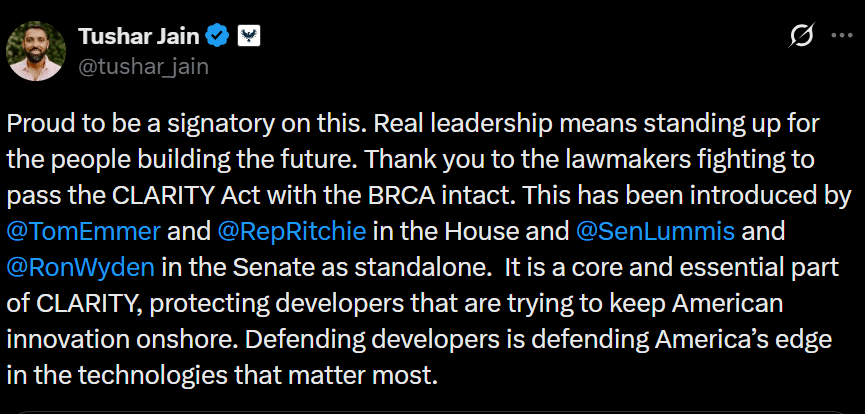

On Tuesday, the 9th of June, another group of over 60 firms, including Hyperliquid, Solana, venture firm MultiCoin Capital, and lobby group DeFi Education Fund (DFF), pressed the Senate to safeguard developers’ rights.

Tushar Jain, co-founder of MultiCoin Capital, said,

Defending developers is defending America’s edge in the technologies that matter most.

Source: X

Commenting on the broader industry push for regulatory clarity, Marcos Viriato, CEO and co-founder of Parfin, told AMBCrypto that regulatory uncertainty is more costly than regulation itself.

As digital finance matures, the conversation is increasingly moving beyond whether digital assets should be regulated and towards how they can be adopted at scale. Regulatory clarity gives institutions the confidence to move from experimentation to implementation.

That said, the White House still sees a path forward for the bill, but warned that time may be running out.

Final Summary

Ethics talks have reportedly hit a ‘rocky’ start, further raising uncertainty on the CLARITY Act’s outlook

Parfin co-founder said the industry’s push for clarity was because uncertainty is more costly amid growing adoption.

When U.S. spot bitcoin exchange-traded funds (ETFs) launched in January 2024, investors had more than a dozen funds to choose from. BlackRock, Fidelity, Ark Invest, Bitwise, VanEck, Franklin Templeton and several others entered what many expected would become a fiercely competitive market.

Eighteen months later, the battle increasingly looks like a two-player race.

Data shows that BlackRock’s iShares Bitcoin Trust (IBIT) and Fidelity’s Wise Origin Bitcoin Fund (FBTC) are doing most of the heavy lifting when it comes to attracting new institutional capital, while smaller funds have become largely irrelevant in determining the direction of the overall market.

The trend was evident throughout the first half of 2026.

On January 14, bitcoin ETFs recorded net inflows of $840.6 million, according to data from Farside Investors. IBIT alone accounted for $648.4 million of that total, while FBTC added another $125.4 million. Together, the two funds represented more than 90% of all inflows that day.

A similar pattern appeared on April 17, when total inflows reached $663.9 million. IBIT brought in $284 million and FBTC added $163.4 million, accounting for roughly two-thirds of all new money entering the sector.

Even during periods of weaker sentiment, the dominance of the two largest funds remained apparent. On May 1, total inflows reached $629.8 million, with IBIT contributing $284.4 million and FBTC adding $213.4 million. Combined, the pair attracted nearly $500 million of the day’s total. The pattern repeated throughout much of 2026, with the two funds frequently accounting for the majority of net inflows on the largest allocation days and often offsetting weakness elsewhere in the ETF market.

The concentration has emerged during a difficult year for bitcoin and the broader crypto ETF market. Bitcoin is down roughly 29% year-to-date, a decline that has tested institutional conviction and triggered several waves of ETF redemptions. Between mid-May and early June alone, spot bitcoin ETFs recorded multiple days of heavy outflows. The selling marks a sharp contrast to earlier periods when investors often viewed bitcoin pullbacks as buying opportunities.

But the data highlights a broader shift taking place in the bitcoin ETF market in which investors increasingly appear to be concentrating their allocations in the largest and most liquid vehicles.

That trend has particularly benefited BlackRock.

IBIT has emerged as the flagship product of the entire spot bitcoin ETF sector, regularly posting the largest inflows and often acting as a stabilizing force during periods of market stress. On several days when the broader ETF complex experienced heavy outflows, IBIT either remained positive or saw far smaller redemptions than its competitors.

The dominance is not entirely surprising. Many of the largest buyers of bitcoin ETFs are financial advisers, registered investment advisers, hedge funds, family offices, pension consultants and institutional asset allocators. For those investors, liquidity, trading volume and issuer reputation often matter as much as the underlying bitcoin exposure itself.

BlackRock manages more than $10 trillion in assets globally and maintains relationships with thousands of wealth-management platforms. Fidelity, one of the largest retirement and brokerage providers in the U.S., brings similar advantages through its distribution network and long-standing presence among retail and institutional investors.

As a result, many allocators increasingly view IBIT and FBTC as the default options for gaining bitcoin exposure.

The flip side is that smaller issuers are struggling to remain relevant.

Funds such as Franklin Templeton’s EZBC, VanEck’s HODL, Valkyrie’s BRRR and WisdomTree’s BTCW frequently record daily flows measured in single-digit millions of dollars.

On many trading days, their contributions are so small that they have little impact on the overall direction of the market.

Even funds that were once viewed as major competitors, including Bitwise’s BITB and Ark’s ARKB, now play a secondary role compared with the industry’s two largest products. Earlier this year, Trump Media & Technology Group withdrew plans for a proposed spot bitcoin ETF, abandoning an effort to enter the increasingly crowded market that is now dominated by products from BlackRock and Fidelity.

The concentration has become particularly noticeable during periods of volatility. When investors buy bitcoin ETFs aggressively, most of the money flows into BlackRock and Fidelity.

When investors sell, the behavior of those two funds often determines whether the sector posts net inflows or outflows.

That dynamic suggests the bitcoin ETF market is entering a new phase. Rather than a broad competition among a dozen issuers, the industry increasingly resembles a winner-take-most business where scale, liquidity and distribution drive investor decisions.