Kalshi is seeking to raise fresh capital at a valuation of about $40 billion, nearly doubling the $22 billion valuation it targeted in its previous funding round, according to a Financial Times report citing people familiar with the matter.

The prediction markets platform could close the fundraising as soon as the third quarter of this year, FT said.

If completed, the deal would widen Kalshi’s valuation lead over rival Polymarket, which was last reported to be seeking funding at $15 billion. The two platforms have emerged as the dominant names in the prediction markets sector, while many other entrants have increased the industry’s competitive landscape.

Kalshi’s previous funding round, which valued the company at $22 billion, attracted a roster of high-profile investors including Philippe Laffont’s Coatue Management, Sequoia Capital, Andreessen Horowitz and Morgan Stanley.

Competition in the sector has intensified as firms race to capture users and expand product offerings.

Kalshi operates as a federally regulated exchange in the United States, a distinction that has helped it attract mainstream investors and institutional backing. Meanwhile, Polymarket, which uses blockchain infrastructure and cryptocurrency-based settlement, has gained popularity among crypto traders and has become widely followed during recent election cycles.

PEP trades at $142, implying ~20% upside to the $170.18 price target, supported by strong Q1 revenue growth and 90% model confidence.

Piper Sandler rates PEP Overweight at $178, and a $10 billion buyback plus 54 consecutive dividend hikes bolster the 2027 bull case.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and PepsiCo didn’t make the cut. Grab the names FREE today.

The headline number for this article is $180, and I want to address it head on before anyone scrolls further.

jetcityimage / iStock Editorial via Getty Images

Our proprietary 24/7 Wall St. price target for PepsiCo (NASDAQ:PEP) is $170.18 over the next 12 months, with a clear path to $180 in the bull case as the World Cup activation, productivity savings, and convenient foods recovery compound through 2027. With shares at $142.02, that base case implies 19.83% upside.

A Defensive Name That Just Went on Sale

PEP has fallen 4.42% over the past 30 days and 1.19% in the last week, partly reflecting hawkish Fed commentary that dimmed appetite for dividend stocks. Zooming out, shares are up 14.55% over the past year and Pepsi remains a Consumer Defensive anchor with a beta of 0.359.

Q1 FY2026 delivered core EPS of $1.61 on revenue of $19.44 billion, a 8.5% year-over-year gain. Operating margin expanded 210 basis points to 16.5%, and management reaffirmed full-year organic revenue growth of 2% to 4%. The next earnings catalyst lands on July 9, 2026.

PEP Earnings Explorer — 24/7 Wall St.

Why Bulls See $180 by Mid-2027

Piper Sandler maintains an Overweight rating with a $178 price target, while TIKR’s longer-term model points to $208 by December 2030. Our bull case scenario lands at $177.28 by June 2027, with the $180 mark within reach if Q2 and Q3 earnings extend the Q1 beat streak.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and PepsiCo didn’t make the cut. Grab the names FREE today.

Growth drivers are tangible. CEO Ramon Laguarta noted that PBNA grew 9% in Q1, and international markets are accelerating around the 2026 World Cup activation. PFNA added 300 million new consumption occasions versus the prior year.

Laguarta stated: “We’ve seen momentum in PBNA, both organic and reported…And sequential growth in PFNA.” Add a $10 billion buyback authorization, the 54th consecutive dividend hike, and active institutional buying, and the bull math works.

PEP Analyst Ratings — 24/7 Wall St.

The Risks Worth Watching

Tariff-driven commodity costs hit PBNA with an 11 percentage point impact in Q4 25, and FY25 operating income fell 19.57% on Rockstar and Be & Cheery impairments totaling $1.993 billion. Volume softness in convenient foods and slower snack consumption tied to GLP-1 adoption could pressure organic growth toward the bottom of the 2% to 4% range. Our bear case scenario stops at $152.27.

The FY25 impairments were one-time charges. Operating cash flow still came in at $12.087 billion, with FCF conversion guided above 80%. Bulls argue the impairments reflect aggressive portfolio cleanup rather than core business deterioration.

PEP Price Target — 24/7 Wall St.

PepsiCo Price Prediction 2026-2030

The 24/7 Wall St. price target stands at $170.18 with 90% model confidence. Q1 delivered +8.5% revenue growth and a 210 bp margin expansion, yet shares trade closer to the 52-week low than the high.

The setup looks constructive for a low-beta compounder with a 4% yield and a clear path to $180 by 2027. The thesis weakens if Fed hawkishness continues penalizing dividend payers through the back half of 2026.

Here is where our model projects PEP could trade, assuming current growth trajectories and margin recovery hold.

These projections assume PEP continues executing the productivity and innovation strategy Laguarta outlined, with the World Cup activation and poppi integration supporting beverage growth.

Significant upside or downside could result from sustained commodity inflation, faster-than-expected GLP-1 impacts on snack volumes, or larger buyback execution against the new $10 billion authorization.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and PepsiCo didn’t make the cut. Grab the names FREE today.

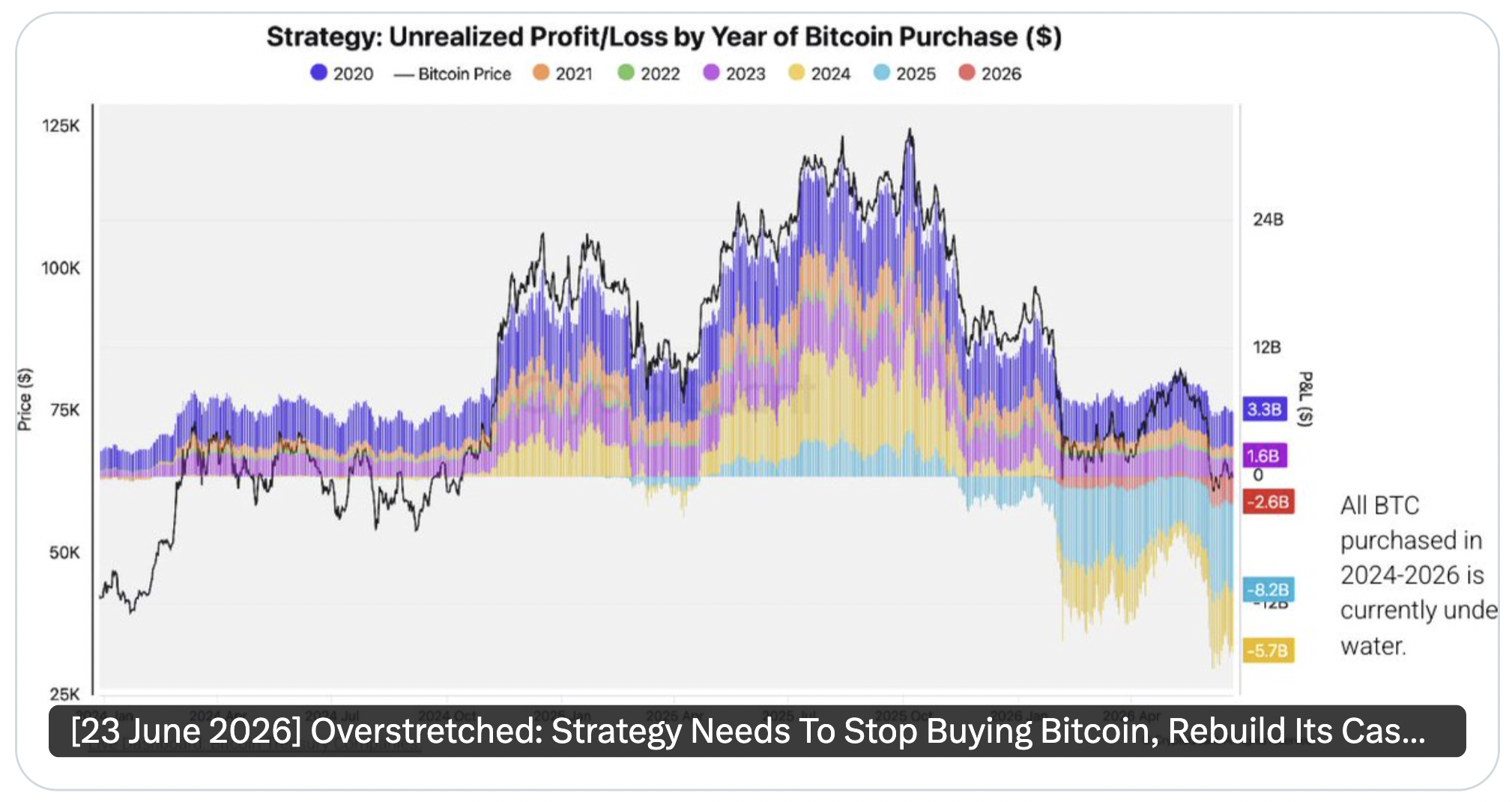

Michael Saylor’s Strategy has amassed 847,363 Bitcoin [BTC], which is equivalent to $53 billion. According to BitcoinTreasuries.NET Strategy purchased all these Bitcoins at an average cost of $75,646, totalling 113 purchases and 1 sale since the 11th of August 2020.

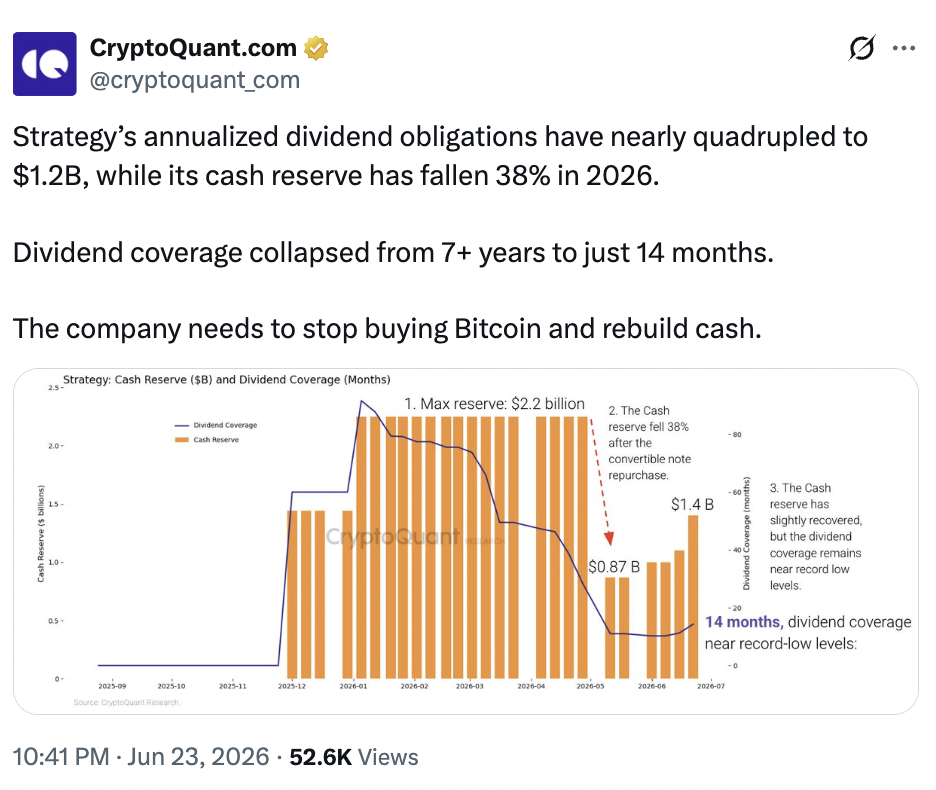

However, instead of receiving praise, Strategy has recently been drawing criticism. A recent report from CryptoQuant suggests that, despite still owning a significant amount of Bitcoin, the company may be under increasing financial strain from its new income-focused security, STRC.

Source: CryptoQuant

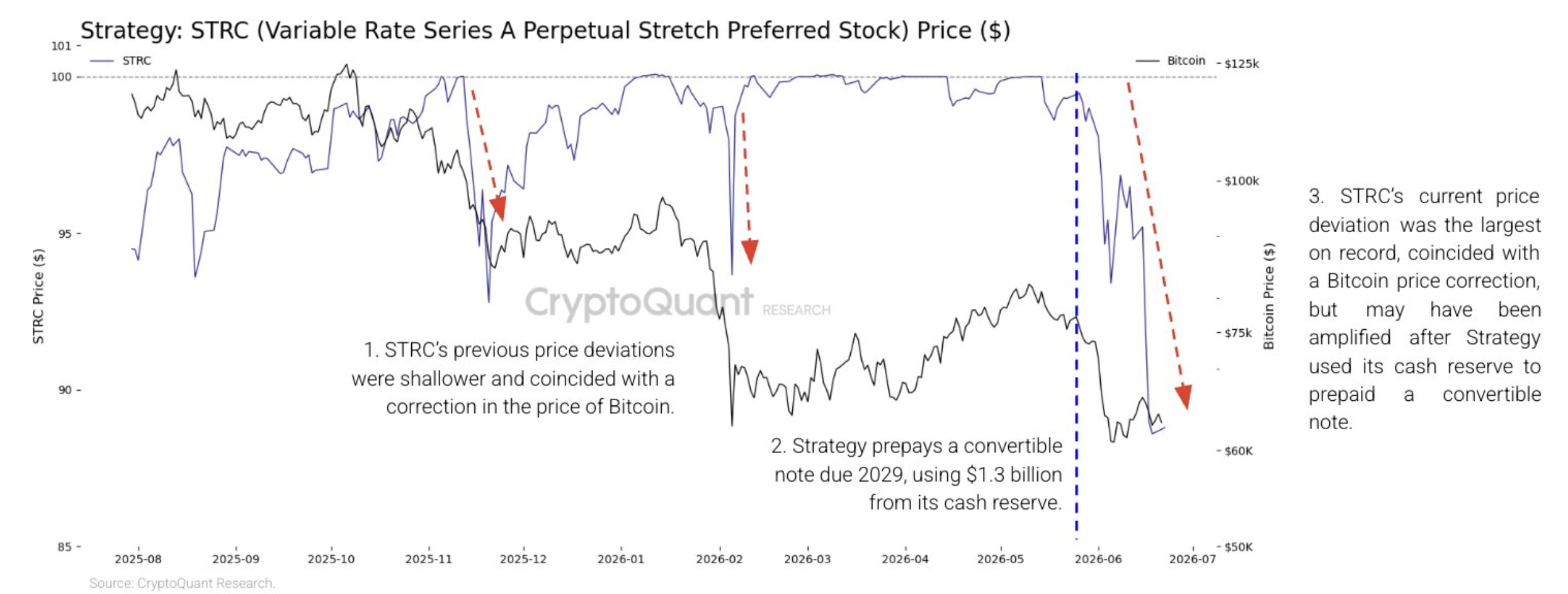

STRC drops below $100 par value

For background, Strategy’s STRC has fallen to $87.65 at the time of writing, significantly below its $100 par value. This happened along with the company’s cash reserves sharply declining in tandem with a correction in the Bitcoin market.

Although Strategy’s yearly dividend commitments have nearly quadrupled to $1.2 billion, the company’s cash reserves have decreased by 38% since the start of 2026.

This means that, as opposed to more than seven years ago, the company now has enough cash on hand to pay dividends for only roughly 14 months. Hence, to comfort investors, Strategy might increase dividend yields or issue more MSTR stock, even though it is unlikely to sell Bitcoin to support STRC.

Source: CryptoQuant

Recent activity around Strategy

However, through its at-the-market program, Strategy sold 2.71 million MSTR shares between the 15th and the 21st of June. As a result, they were able to raise $335.5 million in net proceeds, of which they used to purchase 520 BTC for $34.9 million.

Following this, some community members pointed out that issuing additional MSTR shares would no longer produce the premium value that Saylor’s own capital allocation framework relies on.

Critics slam Strategy’s BTC accumulation

In agreement, Julio Moreno, head of research at CryptoQuant, stated,

The company’s strategic priority should be to pause Bitcoin purchases and rebuild its cash reserve.

Moenor thinks that even though Strategy still has a sizable Bitcoin treasury, it would be difficult to sell Bitcoin to raise money. This is because the company is sitting on an estimated $10.6 billion in unrealized loss, which could reduce shareholder value.

Source: CryptoQuant

Supporters backing Saylor’s plan for Strategy

However, not everyone shared a similar sentiment. Samson Mow, the CEO of JAN3, said,

$STRC has a self-repairing mechanism that most people don’t really understand.

Mow argues that Strategy avoids taking on additional dividend obligations because it stops issuing new shares below par. Meanwhile, a higher effective yield—12.78% if bought at $90—and the possibility of an 11.11% capital gain if the stock rises to $100 draw in buyers.

When combined, these incentives generate a potential return of almost 24%, boosting demand and assisting STRC in its recovery without Strategy’s direct involvement.

Mow, however, also came to the best conclusion when he added,

I’d be surprised if it took more than a few weeks for $STRC to get to par again.

Final Summary

Michael Saylor’s Strategy is adding more and more Bitcoin but STRC tarding below the $100 mark raises concerns.

Community divided between whether Strategy should add or subtract from its Bitcoin stash.

Yakovenko’s comments stood out because they came from one of Ethereum’s most prominent competitors. While debates between Ethereum and Solana supporters have often been contentious, Yakovenko’s reaction reflected a view shared by many currently at the top of the industry: that leaner organizations can sometimes make better decisions than larger, more bureaucratic ones.

The emergence of EthLabs is particularly significant because it arrived the day before the foundation’s layoffs and budget cuts, underscoring what supporters see as a broader trend: Ethereum’s research and development ecosystem increasingly extending beyond the foundation itself.

“I feel that the job cuts at the EF were necessary for their budget, longevity, and CROPs alignment,” said Hudson Jameson, head of ecosystems at CertiK and a former employee at the Ethereum Foundation. “As sad as the layoffs are, it was an inevitability to keep the EF lean long term.”

Jameson described EthLabs’ launch as exciting, noting that its founding team includes respected veterans of Ethereum’s research and development community. “The founding team at EthLabs are long-time, well-respected members of the Eth R&D community,” he said. “I can’t wait to see what they will accomplish.”

For years, critics and supporters alike have debated whether Ethereum relies too heavily on the Ethereum Foundation. As the ecosystem has grown into a global network of developers, infrastructure providers, layer-2 networks, institutions and companies, some leaders have argued that the foundation should become less central rather than more influential.

Silver (SI=F) July futures opened at $65.21 per ounce on Tuesday, 0.6% lower than Monday’s closing price. The price of silver fell this morning to $62.05 per ounce as of 9:08 a.m. ET.

Silver prices are falling this morning as concerns over future rate hikes have eclipsed the progress in peace talks between the U.S. and Iran. Two major investment banks lowered their gold price expectations this year, underscoring how rising borrowing costs curb demand for precious metals. Furthermore, silver prices are struggling even more than gold prices:

While gold’s rebound was short-lived, primarily due to investors reassessing the outlook for U.S. interest rates following last week’s hawkish Federal Reserve meeting, silver has struggled even more than the bullion, said veteran commodities analyst and Head of Commodity Strategy for Saxo Bank, Ole Hansen.

“The combination of higher bond yields, a firmer dollar, and expectations that policy rates may remain elevated for longer continues to challenge investor appetite for non-yielding assets,” Hansen wrote in a post on Substack.

Silver (SI=F) July futures opened 0.6% lower than Monday’s closing price. Here’s a look at how the opening silver price has changed versus last week, month, and year:

One week ago: -6.7%

One month ago: -14.2%

One year ago: +80.3%

For context, silver’s year-over-year growth was 173.3% on May 14.

Want to learn more about the current top-performing companies in the silver industry? Explore a list of the top-performing companies in the silver industry using the Yahoo Finance Screener. You can create your own screeners with over 150 different screening criteria.

Silver price predictions for the next decade

Silver price forecasts vary wildly by expert. Some say silver’s price will hold steady or experience modest growth, while others predict huge price spikes. Here are some of the biggest predictions for silver’s price:

1. Silver reaches $100 per ounce

Experts with BlackRock and J.P. Morgan agree that the outlook for silver remains strong, and its price will increase. By the end of 2026, experts predict silver’s price will surpass $80 per ounce, and it could reach $100 per ounce by 2030.

Does that mean you should buy lots of silver? Be aware that predictions can change, and they may revise their forecasts at any time.

2. Silver coins become more popular

With the conflict in the Middle East, investors are increasingly concerned about economic turmoil and manufacturing supply chain disruptions. Historically, that means investors will increasingly buy precious metals, such as silver.

Because buying an ounce of gold is prohibitively expensive for new investors, silver coins or bars are a more accessible entry point, so there may be increased demand.

3. Pricing may be more volatile

Compared to gold, silver’s price tends to be more volatile, with more rises and falls. Its price fluctuates due to changes in industrial demand and investor confidence.

For example, at the beginning of January 2026, silver’s price topped $113 per ounce. But by February, its price dropped to $77 per ounce, a decrease of about 32% in just a few weeks.

Whether you’re tracking the price of silver since last month or last year, the price-of-silver chart below shows the precious metal’s value journey so far this year.

Elon Musk, the world’s richest man, briefly held onto the title of being the world’s first and only trillionaire before his net worth was deflated back down to a more modest nine-figure amount. On June 12, the day SpaceX began trading on the Nasdaq, Musk became the first person ever to have a $1 trillion net worth. But by June 24, his fortune had flattened down to $957 billion, according to Bloomberg’s Billionaires Index.

During that period, the SpaceX and Tesla CEO was worth—depending on who was counting, using what measures, and what time during the day—somewhere between $1.32 trillion and $1.45 trillion at the top.

Forbes also downgraded Musk’s status, but gave him a few extra million than Bloomberg did: $962 billion, after removing $116 billion of restricted Tesla stock from its math. The two trackers still agree on the durable fact: he is still, by a wide margin, the richest person on the planet. (Larry Page trails far behind as the world’s second richest person, with a net worth hovering around $300 billion).

The round-trip excursion into trillionaire status was sponsored by SpaceX. The company priced its IPO at $135 a share and on June 12, raised a record $85.7 billion at a valuation near $1.77 trillion. Retail buyers chasing Musk’s dream of data centers in space and an eventual Mars settlement pushed the stock to about $225 on June 16, briefly valuing the company close to $2 trillion. However, by Tuesday’s close, it sat near $156, roughly 30% off the peak, and slipped further Wednesday, briefly dipping below the first-day pop price of $150.

Musk’s stake, about 40% of the company, still accounts for the bulk of his fortune; Bloomberg pegs it around $744 billion, or about four-fifths of everything he owns. Scholars have raised concerns about the highly-concentrated nature of the SpaceX governance structure, in that shareholders have unusually little amount of control over the company’s future. The MSCI rated SpaceX a CCC, its worst rating, for its governance structure.

But the other side of Musk’s control is that when the stock goes down, his net worth fluctuates also.

Two forces pulled the stock since the exuberant IPO-week. One was macro: investors priced in the possibility of one or more interest rate hikes after the Fed’s hawkish June meeting, which established the same higher-for-longer backdrop now lifting the dollar to a 13-month high and dragging oil and gold lower.

The other was specific to SpaceX: confirmation of a planned bond sale, reported at roughly $20 billion to $25 billion, which raised the obvious question about why a capital-intensive company issuing debt at a valuation that had just outrun its IPO price. Debt-buyers showed high demand for the bonds, but for the shorter-dated ones, about five years; a less risky purchase than some of the longer term debt that Musk wants to auction off.

The Fortune 500 Innovation Forum will convene Fortune 500 executives, U.S. policy officials, top founders, and thought leaders to help define what’s next for the American economy, Nov. 16-17 in Detroit. Apply here.

Binance has withdrawn its application for a Markets in Crypto-Assets (MiCA) license in Greece and will seek authorization in another European Union country, the crypto exchange said Wednesday via several X posts.

While Binance did not immediately respond to CoinDesk’s request for comment, Gillian Lynch, head of Europe and the United Kingdom, told Reuters that “Binance is not leaving Europe.” Her comment follows her firm’s bid to secure a licence in Greece to offer crypto services in the EU went sour.

Last week, Binance said its European regulatory MiCA application was compliant despite reports of Greek rejection. “Our understanding is that the HCMC (Hellenic Capital Market Commission) completed its review of the application and considered it compliant with MiCA requirements, and that the application was also reviewed at ESMA level,” a Binance spokesman told CoinDesk via email on June 16.

The decision comes days before a June 30 deadline. Under MiCA rules, crypto firms must obtain a license from at least one EU member state by July 1 to serve clients across the 27-nation trading bloc. Unlicensed firms must wind down their EU activities.