Uniswap [UNI] staged an aggressive recovery after buyers returned across the market and pushed the token out of a prolonged period of weakness.

Over the last 24 hours, UNI gained 22.41%, while its market capitalization climbed 22.36% to $2.19 billion. Trading activity strengthened even further, with volume surging 110.49% to more than $560 million.

Such a sharp increase suggested that traders had re-entered the market with conviction rather than reacting to a short-lived price fluctuation. The rally also arrived as several major altcoins posted gains, which helped improve sentiment across the broader market.

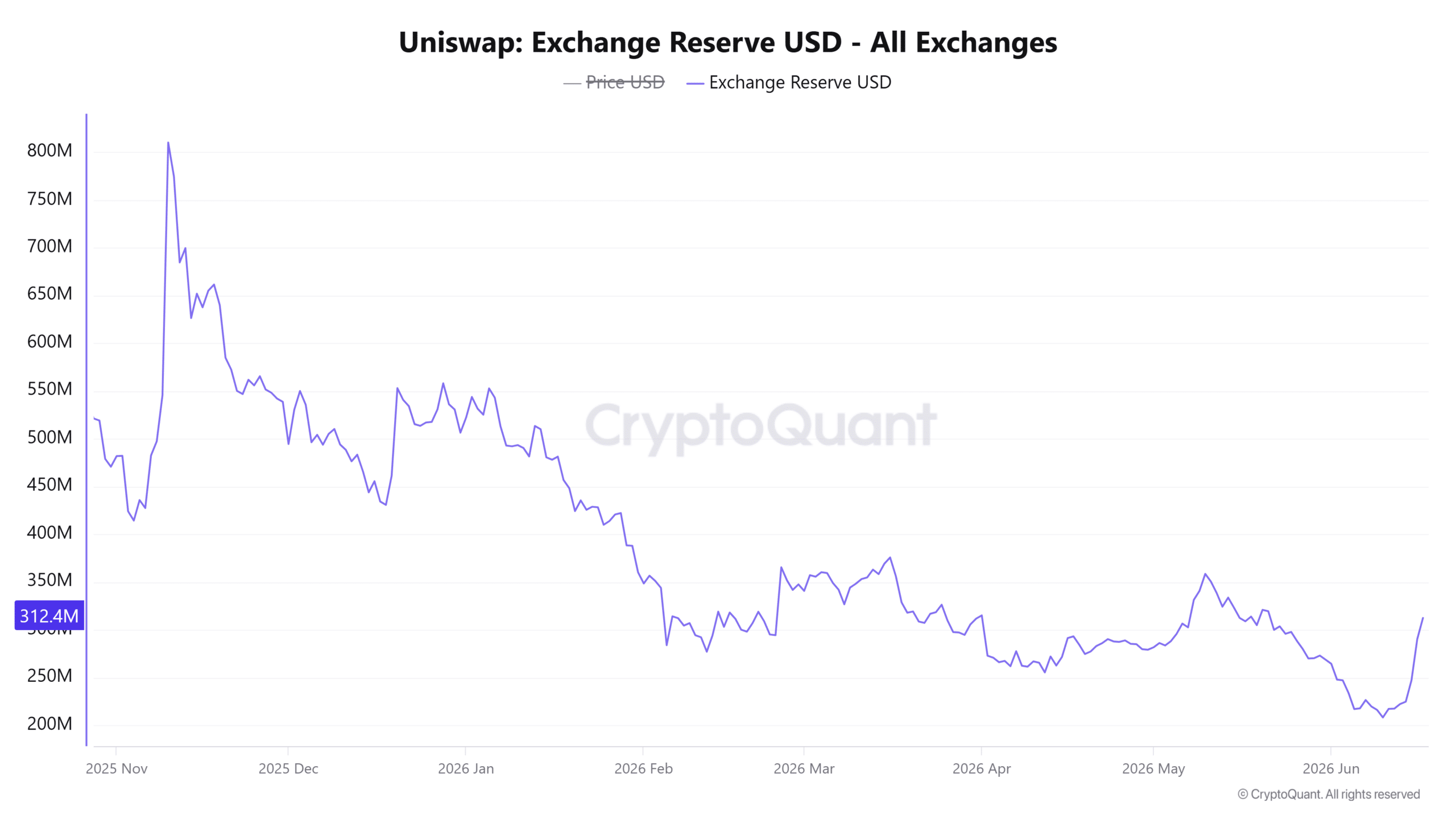

Rising reserves hint at shifting supply dynamics

While price and trading activity expanded rapidly, exchange reserve data painted a more nuanced picture. The total value of UNI held across exchanges increased by 29.36%, reaching approximately $313.24 million.

This represented a notable increase in the amount of capital positioned on trading platforms. An increase in exchange reserves often indicates that more tokens have become available for immediate trading.

In some cases, traders move assets onto exchanges to secure profits after a strong rally. However, rising reserves do not automatically signal incoming selling pressure, especially when demand remains strong.

Source: CryptoQuant

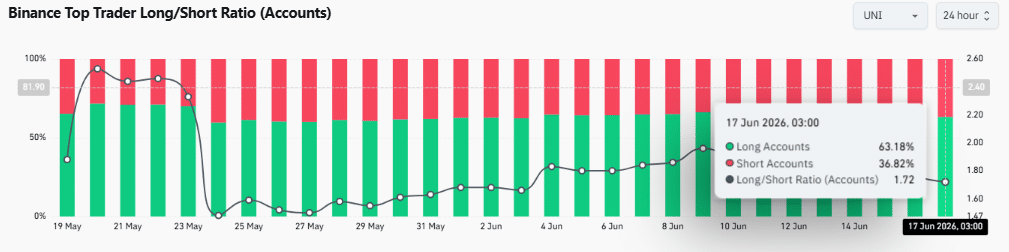

Bulls continue dominating Binance positioning

Derivatives traders maintained a bullish stance despite recent market volatility. Binance’s Top Trader Long/Short Ratio showed that 63.18% of accounts held long positions, while only 36.82% remained short.

This produced a Long/Short Ratio of 1.72, reflecting a clear preference for upside exposure.

The data suggested that experienced traders continued positioning for additional gains following UNI’s breakout. Unlike highly crowded bullish setups, the ratio remained elevated without reaching extreme levels.

This condition often leaves room for further positioning before sentiment becomes overheated.

Source: CoinGlass

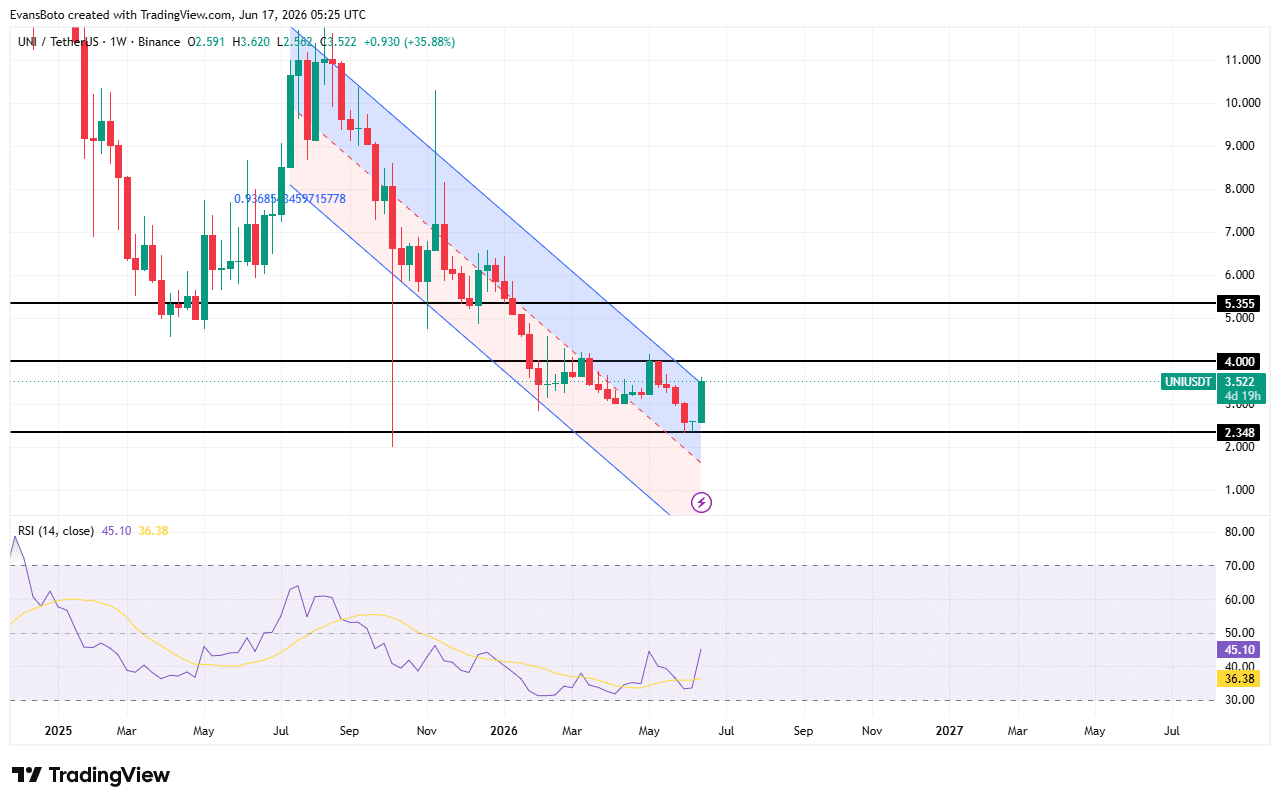

Has UNI finally escaped its downtrend?

UNI delivered one of its strongest weekly recoveries after rebounding from the lower boundary of a long-term descending channel that had contained price action for several months.

Buyers pushed the token toward $3.52 and challenged the channel’s upper resistance, which marked a significant improvement in market structure. The weekly chart showed UNI recovering from support near $2.35, a level that previously attracted renewed demand.

Meanwhile, the Relative Strength Index climbed to 45.10 from deeply oversold conditions and moved above its signal line near 36.38.

Although the RSI remained below the neutral 50 level, the indicator reflected strengthening buying interest and improving market conditions. A weekly close above the descending channel could confirm a broader trend shift.

Under that scenario, UNI could challenge the $4.00 resistance level before targeting the next major barrier around $5.35.

Source: TradingView

Current market conditions favored buyers as volume expanded, trader positioning remained bullish, and technical indicators continued improving.

The increase in exchange reserves introduced a degree of caution, yet demand had remained strong enough to absorb additional supply.

If UNI secures a decisive move above $4.00, the recovery could continue toward $5.35. However, failure to overcome that resistance would likely keep price consolidation in focus before the next directional move emerges.

Final Summary

UNI’s breakout gained support from rising volume and bullish trader positioning.

Exchange reserves increased sharply, making incoming supply trends worth monitoring.

Chipotle’s (CMG) biggest stock-market problem may not be burritos, menu prices or slowing comparable sales.

It might be investor skepticism.

Bank of America thinks the restaurant business is demonstrating a demand pattern that might be significant for the beaten-down growth brands, including Chipotle Mexican Grill. Consumers still prefer to cut restaurant wallet share when gas takes up a bigger slice of the household budget, according to the firm’s June 12 restaurant-industry survey.

But BofA’s more noteworthy finding is that consumers seem to be holding the line on the amount of restaurant meals they buy, even while price and spending patterns are changing.

That distinction is important to Chipotle since the stock has been caught up in a broader reset for high-growth restaurant names. BofA says the biggest valuation compression has been for companies where comparable sales have slowed, including Chipotle, Domino’s Pizza (DPZ) and Wingstop (WING).

The firm still has a Buy rating on Chipotle, with a $50 price target, compared to the price of $31.25 in the report.

BofA said its analysis indicates that consumers “try to preserve the quantity of restaurant meals” even as pricing and spending fluctuate.

Chipotle sits at the center of BofA’s restaurant-stock argument

BofA’s restaurant-stock thesis is most attractive based on Chipotle being a growth story as well as a consumer-demand story.

The company has long been considered a luxury restaurant operator. Investors have been rewarding Chipotle for its pricing power, restaurant-level profitability, digital ordering, brand strength and extended runway for new locations. That works when traffic is healthy and consumers are still willing to pay for fast-casual.

But things grow more complicated when investors start to worry about the strain on household budgets.

Gas prices are important because gasoline is not a trivial item for many customers to cut back on. When drivers have to pay more at the pump, they could have less freedom to go out to eat. That’s why investors often smack down restaurant equities when they see fuel costs going up.

BofA’s work backs that fear up, but only to a point.

Between 2009 and 2019, the firm found that changes in restaurant wallet share closely and inversely correlated with changes in gas wallet share. Put simply, when gas shaved a larger slice off consumer spending, eateries tended to lose share.

The connection was negative in the post-Covid period, from March 2023 through April 2026, BofA said. But the link also got noisier, meaning gas doesn’t explain restaurant demand as clearly as it used to.

BofA’s analysis suggests that viewing restaurant growth stocks as just the victims of increasing household expenditures may be too harsh. Consumers might be altering their buying habits, but they aren’t necessarily forsaking restaurant visits.

BofA finds a demand clue in restaurant spending

The essential takeaway from the BofA analysis isn’t that more gas spending can be bad for eateries.

That is already known to investors.

The bigger finding emerged when BofA adjusted spending categories for inflation. The business deflated restaurant and gas spending by their respective consumer-price measures and found the relationship between real gas wallet share and real restaurant wallet share to be substantially weaker.

This is important because restaurant stocks can seem worse when investors are only looking at dollars spent. Even if consumers remain eating out, sales growth can decelerate if menu-price inflation eases. The BofA note shows the true demand picture may be stronger than the headline spending numbers suggest.

Industry same store transaction growth averaged negative 1.5% to negative 3% since 2023, with average check growth ranging from 2.8% to 9.2%, said BofA.

That’s a suboptimal backdrop.

Traffic remains bad; customers remain choosy. The takeaway, BofA says, is that restaurant demand doesn’t appear broken. Consumers seem to be keeping up the habit of eating out, even as their spending shifts with gas prices, menu pricing and inflation.

That’s a major difference for Chipotle.

More Restaurants

The corporation doesn’t want investors to think consumers are suddenly rich with cash. It demands investors buy into the idea that dining out is robust enough to support long-term unit growth, earnings expectations and a premium brand valuation.

BofA thinks the market has become overly skeptical. The business said the biggest valuation compression has been for food firms that were growing at a high rate but have seen their comps decline, such as Chipotle, Domino’s, and Wingstop. BofA feels growth is more sustained than the market presently prices in.

Chipotle’s valuation may be missing a key demand signalSimon McGill / Getty Images

Chipotle investors should watch traffic, not just prices

The next test for Chipotle investors is whether traffic can hold up with pricing becoming less and less of a tailwind.

Two years later, BofA said in March 2023 that restaurant menu price rises had dropped from what was at a decades-high pace to more of a long-term average pace. That matters because plenty of restaurant companies saw their average checks go up when menu prices were rising faster.

When that pricing advantage disappears, the traffic value goes up.

Traffic that is consistent or better would confirm BofA’s perspective of consumers “protecting” restaurant meals for Chipotle. This would also assist investors in distinguishing between a normal deceleration in pricing and a more serious demand problem.

Light traffic would cause the opposite problem. If customers visit less frequently and pricing continues to lag, the market may become even more cautious about Chipotle’s growth prospects.

So the BofA note reverses the framing.

It’s not just about whether Chipotle can charge more or people are just spending less at restaurants in nominal dollars. The larger question is whether customers still consider fast-casual meals a regular part of their lives.

Key takeaways for Chipotle investors

BofA says gas and restaurant wallet shares still tend to move in opposite directions.

The post-Covid relationship has become noisier, meaning gas does not explain restaurant demand by itself.

BofA’s inflation-adjusted work suggests consumers are trying to preserve restaurant visits.

Chipotle, Domino’s and Wingstop have seen valuation compression as comps slowed.

BofA rates Chipotle Buy with a $50 price objective.

Investors should watch traffic trends as menu-price inflation cools.

Domino’s and Wingstop matter because they support the larger argument. BofA noted that all three are former high-growth restaurant stocks whose valuations have shrunk. But Chipotle is the most obvious test, as it’s one of the most recognizable fast-casual brands and is related to investor discussions around traffic, price and long-term unit growth.

BofA’s gas-price clue changes the Chipotle debate

The simple story around restaurant stocks is increasing gas costs reduce demand.

BofA’s report is more helpful since it poses a more pointed question: Are customers abandoning restaurant meals, or are they just spending differently when gas prices and menu prices fluctuate?

That question is important for Chipotle, since the company has been considered a growth name facing more skepticism about demand. If consumers are still guarding restaurant visits, Chipotle’s valuation decrease could be pricing in too much weakness.

That does not eliminate the risks.

But Chipotle still requires steady traffic, solid restaurant execution, disciplined pricing and continuous unit growth to justify a premium multiple. Gas prices can still hurt lower-income shoppers, and slower average-check growth might make same-store sales look less exciting.

But the work by BofA implies investors may be looking at the incorrect demand signal.

The most crucial question for Chipotle investors may not be whether people spend less when gas costs rise. It may be whether they keep turning up.

If they do, BofA’s judgment on restaurant stocks may be right: Chipotle’s slowdown might not be the end of the growth story but the moment investors became too cautious of it.

If you’re only looking at the dollar price of your portfolio, you may be missing part of the picture, which is significantly shaped by money supply growth.

To the casual observer, the markets look like business as usual. While bitcoin has nearly halved to $66,000 since its $126,000 peak in October of last year, the decline could be dismissed as just another brutal, quadrennial crypto bear market. Meanwhile, the S&P 500 continues to hover near record highs.

But beneath the surface, a more interesting signal emerges when both prices are adjusted for the U.S. M2 money supply. M2 is the Federal Reserve’s estimate of liquid assets, including cash on hand, money deposited in checking and savings accounts, and other short-term saving vehicles such as money market funds and certificates of deposit.

Monetary exhaustion?

Some observers see bitcoin as a high-beta barometer for dollar liquidity, and the BTC/M2 ratio, bitcoin’s price adjusted for money supply growth, is now flashing a warning. The ratio, after a sharp climb from 2023 through 2025, appears to have formed what technical analysts call a head-and-shoulders pattern, typically read as a bearish signal.

If the pattern holds, it would suggest bitcoin’s exponential edge over money supply growth — the dynamic that let it outrun debasement so convincingly in prior cycles — is fading. Bitcoin’s ability to outpace the flood of new dollars may be approaching diminishing returns, at least for now.

Standard Chartered Says UNI Could Hit $100 as Wall Street Moves Onchain

Standard Chartered has opened coverage of Uniswap with one of the most aggressive Wall Street forecasts yet for a major DeFi token, setting a $100 price target for UNI by the end of 2030.

The call would put UNI nearly 40 times above its current level near $2.70, with the bank arguing that Uniswap could become a larger market infrastructure layer as tokenized assets move deeper into decentralized finance. Standard Chartered’s price path calls for UNI to reach $6.50 by the end of 2026, followed by $20 in 2027, $40 in 2028 and $65 in 2029 before hitting $100 in 2030.

Geoffrey Kendrick, Standard Chartered’s global head of digital assets research, framed the thesis around Uniswap’s role as a neutral trading infrastructure rather than just a retail decentralized exchange. He wrote that the token could “outperform both ETH (CRYPTO: $ETH) and BTC (CRYPTO: $BTC) through end-2030,” helped by institutional adoption of tokenized securities, stablecoins and other onchain financial assets.

More From Cryptoprowl:

The bank expects the value of tokenized assets active in DeFi to grow 37-fold by 2030, pushing total value locked across DeFi protocols to about $2.7 trillion. That would expand the pool of assets available for decentralized trading venues, with Uniswap positioned as one of the clearest beneficiaries because of its scale, brand and automated market maker model.

Uniswap has already become part of the institutional tokenization stack. BlackRock’s BUIDL fund became accessible through UniswapX in February, while Uniswap has also highlighted tokenized versions of major equities such as Apple (NASDAQ: $AAPL), Tesla (NASDAQ: $TSLA), Nvidia (NASDAQ: $NVDA) and SpaceX (NASDAQ: $SPCX) moving through its ecosystem.

The forecast still depends on execution. Uniswap faces competition from specialized DeFi venues, possible compliance rules around tokenized assets and the need to keep activity flowing through UNI-linked economics. But the bank’s report adds another signal that large financial institutions are starting to treat DeFi infrastructure as part of the tokenization trade.

Uniswap (CRYPTO: $UNI) is currently trading at $2.79 U.S. per digital token.

XRP has had a relatively quiet 24 hours of trading. It was above the $1.18-local resistance level, but has only moved by 0.21% since. This, despite its daily trading volume shrinking by 44%.

Spot XRP ETF flows have been positive for the most part this month. The bounce from $1.14 to $1.29 last weekend has begun to wane though, and the price is once again struggling to stay afloat above the $1.21 local support.

AMBCrypto reported concentrated demand in the South Korean exchange Upbit during the recent price move higher. Since the demand wasn’t reflected evenly across other exchanges, it did not allude to a sustained recovery being underway for XRP.

XRP achieves bullish breakout target

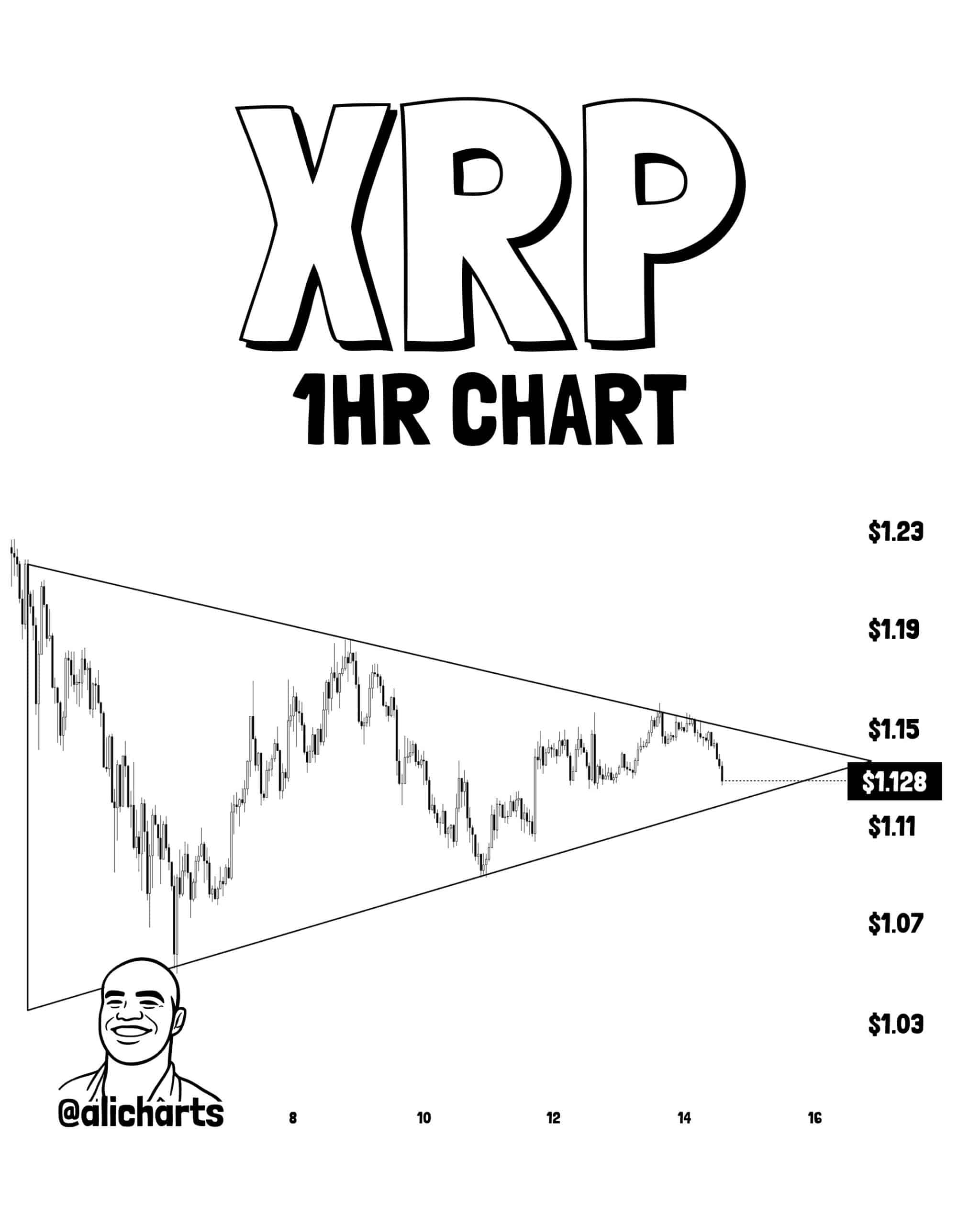

However, in a post on X, crypto analyst Ali Martinez pointed out that a symmetrical triangle formation was underway.

Source: Ali Charts on X

This pattern was projected to have a 14% breakout target, and it did nearly reach the $1.30 target before retracing.

At the time of writing, the lower timeframe had shifted from bullish to neutral too.

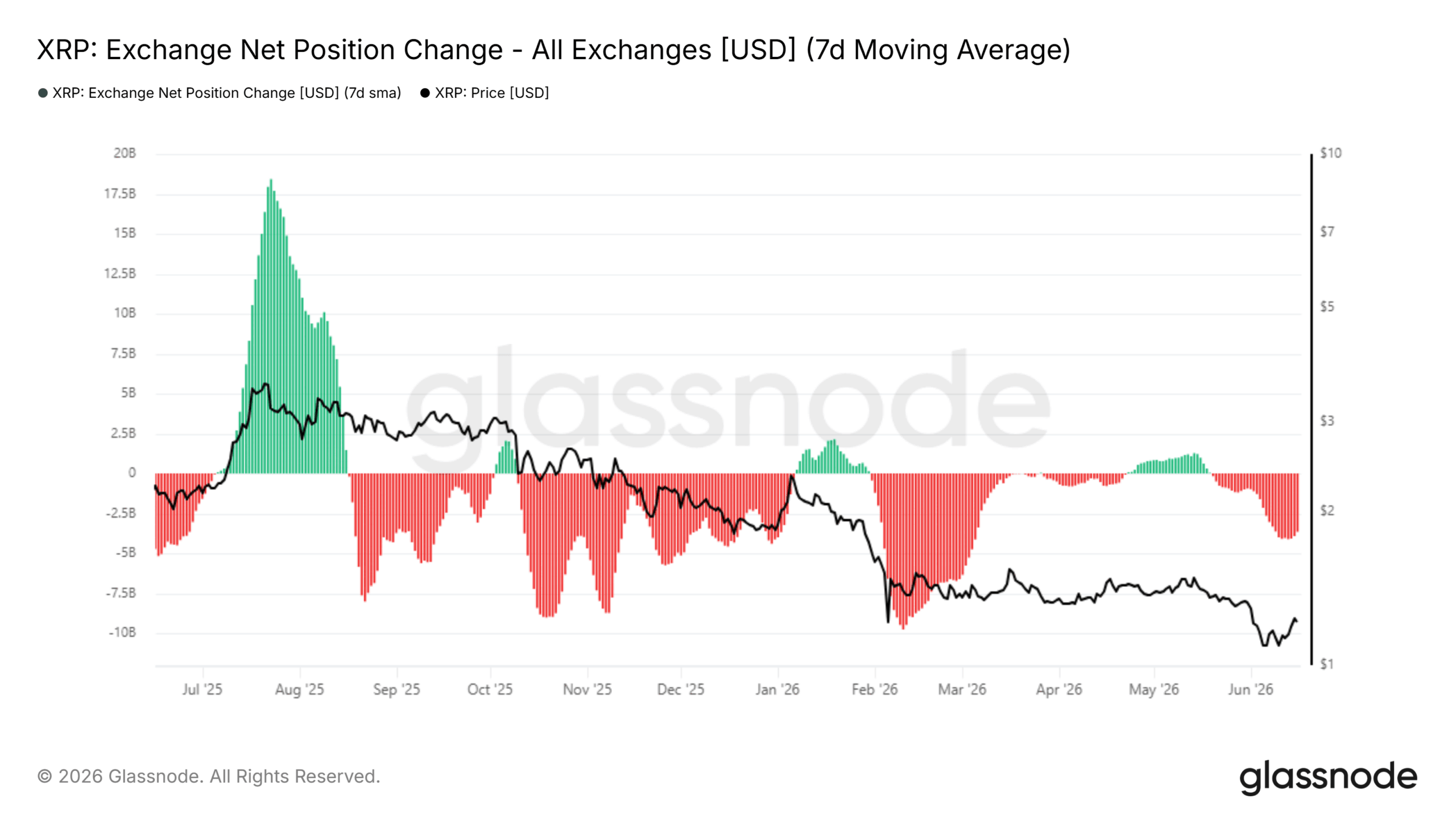

Source: Glassnode

That’s not all either as the 7-day moving average of the exchange net position change became increasingly negative over the past three weeks. This meant XRP was flowing out of exchange wallets, reflecting accumulation.

By itself, it does not guarantee a price trend. In February, the massive sell-off was followed by rapid accumulation, but the price of XRP did not enter another uptrend.

Instead, it formed a range before continuing its descent.

XRP’s price action continues to favor a bearish bias

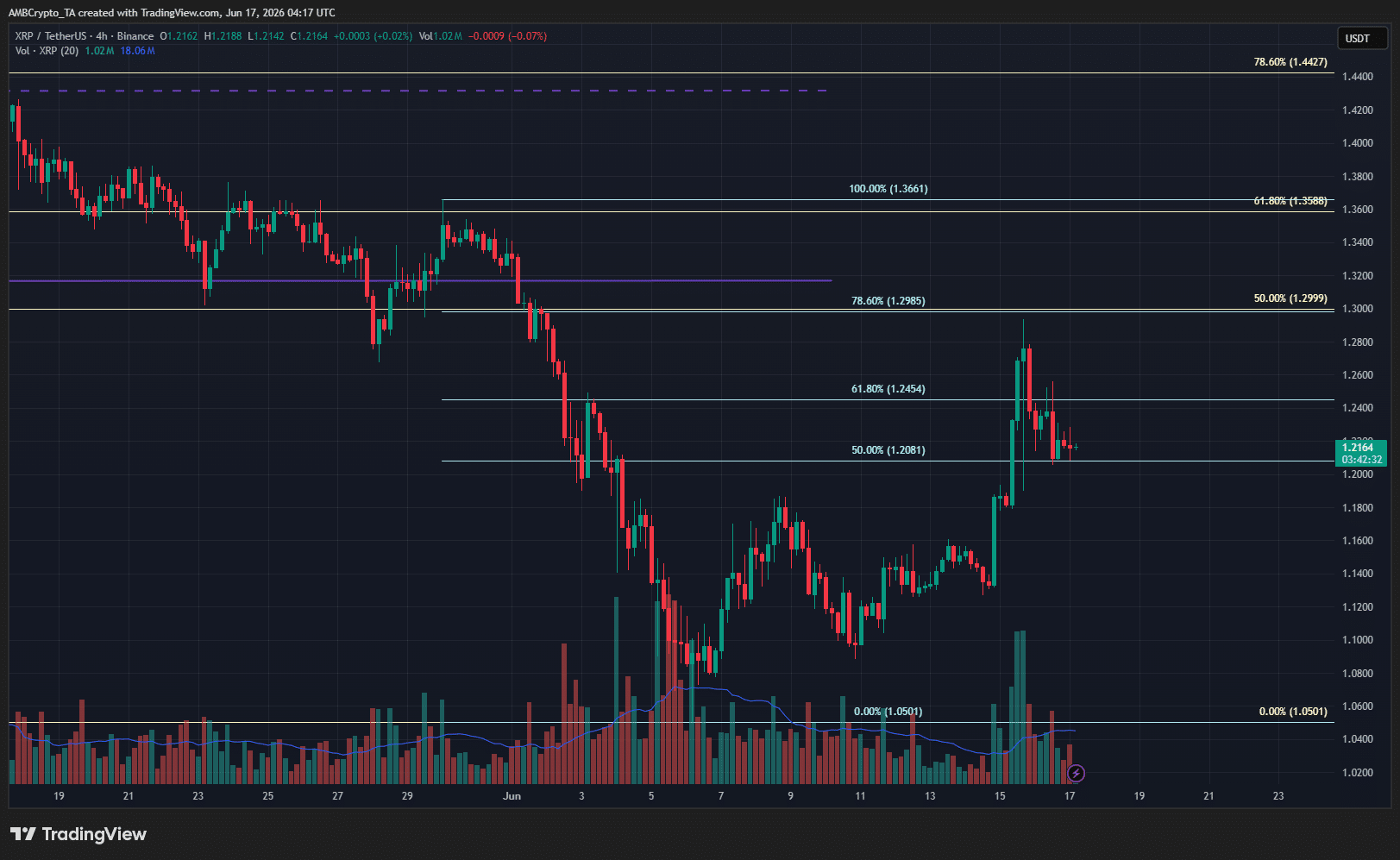

Source: XRP/USDT on TradingView

The breakdown from the range made a bearish structural break. The bounce over the past two weeks was barely able to reach the 50% retracement level before declining to $1.21, at the time of writing.

The risk-to-reward was not favorable for swing buyers. Traders can use a bounce to $1.35-$1.44 to sell, targeting a breakdown below $1.05.

Source: XRP/USDT on TradingView

The 4-hour chart revealed that the bearish move might already be underway. The altcoin has faced rejection from the H4 78.6% retracement level at $1.298. A drop below $1.208 would reinforce short-term bearish momentum.

Final Summary

XRP Spot ETF flows and accumulation trends on-chain might not be enough to orchestrate a recovery.

Longer-term price trend has been bearish and the recent rejection from just below $1.30 can spark another sell-off.

A Russian frigate opened fire in the English Channel on Tuesday, firing warning shots with small arms near a UK-registered civilian yacht, London and Moscow said.

The warship Admiral Grigorovich fired several shots — single rounds, not automatic fire — near the Bright Future, a sailing yacht, roughly 20 nautical miles south of the Isle of Wight outside UK territorial waters.

The UK assesses that the Grigorovich was signaling to other vessels that it was drifting instead of maneuvering under power, possibly leaving the warship feeling vulnerable. It sounded warnings before opening fire.

“Following attempts to contact a British vessel in the channel, the Grigorovich fired warning shots,” a UK defense ministry spokesperson told Business Insider. “These were not aimed at the vessel and were an attempt to prevent a possible collision.”

Russia’s defense ministry said the frigate had attempted to contact the Bright Future with radio, signal flares, and sound signals, but opened fire after receiving no response and seeing the yacht “following a dangerous course.”

“After closing the distance to 150 meters, the frigate’s commander decided to carry out the preemptive fire at the vessel’s course with small arms,” Moscow said.

A retired British couple on board the Bright Future told the BBC that the two vessels were not on a collision course and that the yacht had adjusted its path after the Admiral Grigorovich issued five horn blasts.

The incident follows the UK’s Royal Marines’ separate seizure of the MV Smyrtos, a tanker believed to be part of Russia’s shadow fleet, off the southern coast of England on Sunday.

Military helicopters boarded the MV Smyrtos off the coast of Portland.

While both events occurred in the English Channel, the UK defense ministry said that the seizure and Tuesday’s warning shots from the Admiral Grigorovich were isolated incidents.

“HMS Mersey has been monitoring the Russian vessel, and support has been provided to the crew of the yacht,” the defense ministry spokesperson said.

Still, the Russian navy has been repeatedly reported to be escorting shadow fleet tankers in convoys. The Admiral Grigorovich, part of the Black Sea Fleet, was spotted convoying two tankers in the English Channel in April, just after UK Prime Minister Keir Starmer had given British forces the authority to seize shadow fleet vessels.

Retired Royal Navy Commodore Steve Prest, now an associate fellow at the UK’s Royal United Services Institute, said it is possible that the Grigorovich’s commanding officer decided to open fire after they got too nervous about an unresponsive yacht near the warship.

However, Prest said in comments shared with Business Insider, given the context of the shadow fleet and the Royal Marines’ seizure of the Smyrtos, “I think this is the Russians baring their teeth,” adding that Moscow “very rarely will do something like this in an uncalculated, haphazard way.”

Prest said Russia may be trying to signal to other ships preparing to go through the English Channel: “Hey, look, we are here, we are serious, and we are prepared to stand our ground, so let’s not have any miscalculation.”

The 409-foot-long guided-missile frigate is the lead ship of its class and was commissioned in 2016. The ship’s main armament consists of eight vertical launch cells for land-attack cruise missiles and a 100mm naval gun.

June 16, 2026: This story was updated to reflect comment from the UK Defense Ministry.

Eligible businesses may also continue to evaluate or pursue their own MiCA-focused crypto asset service provider (CASP) licenses in parallel while integrating BitGo Europe’s infrastructure, BitGo said.

The final deadline for crypto firms to have transitioned to the MiCA regime is the end of this month, a regulatory reckoning that will force some firms to close down their businesses.

Industry estimates suggest that Europe had more than 3,000 registered crypto firms as of 2024, with Poland alone accounting for over 1,400 registrations. As of May 2026, there are 194 authorised CASPs (including credit institutions) and it is expected that around 75% of the pre-MiCA population will lose registration status as transitional periods expire, according to law firm Hogan Lovells.

Belshe said firms don’t need to go bust because of MiCA’s regulatory requirements, adding that regulators are aware of BitGo’s compliance-enhancing infrastructure offering. In terms of fees for the crypto compliance service, Belshe said it’s relatively cheap and varies product by product.

“There’s some amount of monthly minimum that you pay similar to what’s always been there. That’s a couple of $1,000 a month type of thing that can scale with volume,” he said. “Then clients can either go to variable-based plans, where they’re paying per transaction more, or they can use static-based plans, where they have kind of a fixed fee, and they pay less.”